{kind=link}

[ad_1]

Editors’ be aware: When this publish was first revealed the x-axis labels on chart 2 and three have been incorrect, and the y-axis label was incorrect on chart 4. The charts have been corrected. 9:47 a.m. ET, July 12.

The financial disruptions related to the COVID-19 pandemic sparked a world dash-for-cash as traders bought securities quickly. This promoting strain occurred throughout superior sovereign bond markets and precipitated a deterioration in market functioning, resulting in quite a few central financial institution actions. On this publish, we spotlight outcomes from a latest paper wherein we present that these disruptions occurred disproportionately within the U.S. Treasury market and provide explanations for why traders’ promoting pressures have been extra pronounced and broad-based on this market than in different sovereign bond markets.

The COVID-19 Pandemic Brought on Market Disruptions throughout Sovereign Bond Markets

At first of the COVID-19 pandemic in late February 2020, and in response to the financial repercussions of impending lockdown measures, traders started to demand higher-quality, secure belongings. Particularly, they shifted their portfolios towards sovereign bonds, and the ensuing shopping for strain drove sovereign yields to say no broadly. Because the disaster intensified in March 2020, nevertheless, traders’ demand for money surged, resulting in promoting strain on sovereign bonds and subsequently will increase of their yields. This down-and-up sample in yields is illustrated for ten-year U.S., German, U.Okay., and Japanese bonds within the chart beneath.

Cumulative Yield Modifications throughout Sovereign Bond Markets

Notes: The chart shows the cumulative yield adjustments for ten-year sovereign bonds, beginning on January 1, 2020. U.S., Germany, U.Okay., and Japan denote Treasury, bund, gilt, and Japanese authorities bond (JGB) securities, respectively.

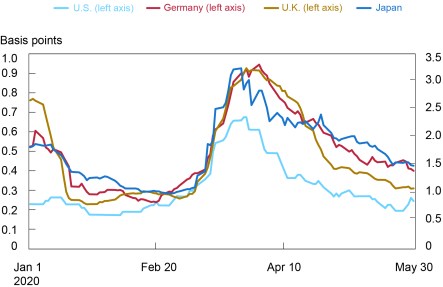

Alongside these adjustments in yields, sovereign bond liquidity deteriorated considerably in March 2020. For instance, bid-ask spreads elevated for U.S., German, U.Okay., and Japan ten-year sovereign bonds over late February and March 2020 (see the chart beneath).

The Unfold between Bid and Ask Yields throughout Sovereign Bond Markets

Notes: The chart exhibits the unfold between bid and ask yields for ten-year sovereign bonds on a ten-day, backward-looking transferring common. U.S., Germany, U.Okay., and Japan denote Treasury, bund, gilt, and Japanese authorities bond (JGB) securities, respectively.

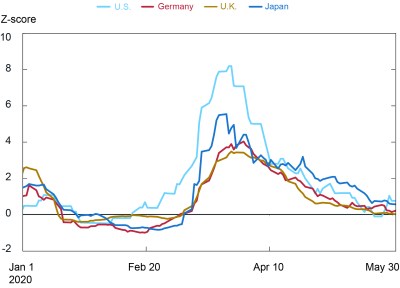

Though promoting pressures materialized for sovereign bonds broadly in March 2020, buying and selling situations within the U.S. Treasury markets noticed the biggest influence. For instance, the deterioration within the bid-ask unfold, normalized by its historic common, was extra pronounced for U.S. Treasuries than for German, U.Okay., and Japan sovereign bonds (see the chart beneath), whereas sometimes the normalized bid-ask unfold of U.S. Treasuries is decrease and extra steady than these of German, U.Okay., and Japan sovereign bonds.

The Normalized Unfold between Bid and Ask Yields throughout Sovereign Bond Markets

Notes: The chart exhibits the unfold between the ten-day, backward-looking transferring common of bid and ask yields for ten-year sovereign bonds, normalized by their respective Z-scores. Z-scores are computed from a ten-day transferring common of end-of-day bid-ask spreads utilizing knowledge from

January 2017 to January 2019. U.S., Germany, U.Okay., and Japan denote Treasury, bund, gilt, and Japanese authorities bond (JGB) securities, respectively.

Promoting Pressures Had been Disproportionately Larger within the U.S. Treasury Market

The breadth and depth of promoting pressures throughout investor varieties in the course of the COVID-19 shock was extra extreme in U.S. Treasuries than in different main sovereign bond markets, partly due to the U.S. greenback’s dominant standing as each an funding and funding forex.

Whereas central banks bought reserves denominated in all main currencies, gross sales of U.S. greenback belongings have been disproportionately higher. Certainly, gross sales of U.S. greenback reserves have been estimated to account for greater than 80 % of complete reserves gross sales, effectively in extra of the U.S. greenback’s roughly 60 % share of international change reserves.

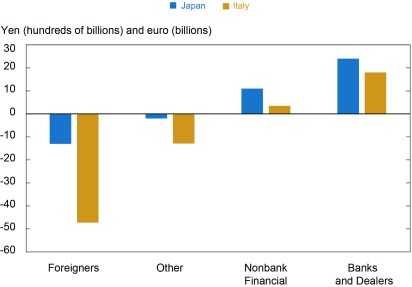

Non-public investor gross sales have been additionally extra pronounced in U.S. Treasuries than in different sovereign bonds. Information on investor transactions and holdings of sovereign bonds in Japan and Italy recommend that bond gross sales in March 2020 have been principally from international traders, as home nonbank traders—together with asset managers, insurers, and pension funds—appeared to both add to sovereign bond positions or stay roughly impartial (see chart beneath). In distinction, promoting pressures within the U.S. Treasury market have been broad-based, as each international traders and U.S. home mutual funds—which maintain a major share of marketable Treasury holdings—have been giant web sellers of U.S. Treasuries within the first quarter of 2020.

Purchases of Japanese and Italian Sovereign Bonds by Investor Sort in March 2020

Notes: The chart reviews the online purchases of Japanese sovereign bonds (JGBs) within the secondary market, excluding payments, and the combination change in holdings of Italian sovereign bonds (BTPs). Nonbank Monetary consists of funding trusts and insurers.

In the meantime, banks in international jurisdictions appeared to play a a lot bigger function in absorbing investor gross sales than banks in the US. Information from Japan and Italy present heavy web purchases from banks that helped offset international gross sales (see the chart above). In distinction, U.S. banks have been modest web sellers of U.S. Treasuries within the first quarter of 2020.

Larger Leverage Underpinned Bigger Promoting Pressures in Treasuries

Variations within the provide of securities and the buildup of Treasuries by levered entities comparable to relative worth hedge funds have been additionally components driving heavier web gross sales of U.S. Treasuries in early 2020. From the beginning of 2017 to proper earlier than the March 2020 shock, U.S. Treasury securities (excluding these held within the Federal Reserve’s System Open Market Account) elevated by greater than $3 trillion, whereas development in different jurisdictions was both modest (the U.Okay. and France) or damaging (Germany and Japan). Heavy Treasury issuance, amongst different components, contributed to a notable absorption of U.S. Treasuries by levered funds, rendering Treasuries significantly extra susceptible to fast deleveraging in the course of the March shock. Suggestions from international market members famous that leveraged funds’ participation in sovereign bond markets was not as giant within the run-up to the disaster.

Market Microstructure Variations Had been Much less Consequential

In our paper, we additionally discover the extent to which variations in bond market constructions could have amplified or mitigated strains. We discover that these components—together with market-maker obligations, the share of nonbank liquidity provision, the diploma of central versus bilateral clearing, and the prevalence of digital versus voice buying and selling—could have performed a modest function however weren’t main sources of differentiation within the functioning of sovereign bond markets in early 2020.

Takeaways

Though traders bought all kinds of belongings in the course of the COVID-19 pandemic, market functioning for U.S. Treasuries deteriorated disproportionately as in comparison with different sovereign bonds. We argue that the comparatively higher decline in Treasury market functioning was resulting from pronounced and broad-based promoting pressures, which have been pushed primarily by the greenback’s dominant standing as an funding and funding forex in addition to the massive presence of levered entities within the Treasury market in early 2020.

Questions stay about how effectively the Treasury market will soak up future promoting pressures from a broad base of traders. A big change within the Treasury market since March 2020 is the Federal Reserve’s introduction of the Standing Repo Facility and the FIMA Repo Facility. These liquidity services enable eligible counterparties to change Treasuries for money at an administered fee. As a steady supply of funding, these new applications might attenuate the necessity for gross sales throughout liquidity shocks, serving to to clean market functioning.

Moreover, the Treasury market could endure important adjustments. Instructed adjustments embody the enlargement of central clearing, the registration of energetic buying and selling corporations engaged in buying and promoting of securities as sellers with the SEC, enhanced oversight of buying and selling platforms, and enhancements within the high quality of information reporting.

Jordan Barone is a capital markets buying and selling principal within the Federal Reserve Financial institution of New York’s Markets Group.

Alain Chaboud is a senior financial venture supervisor within the Program Route Part on the Federal Reserve Board.

Adam Copeland is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Cullen Kavoussi is a coverage and market monitoring principal within the Financial institution’s Markets Group.

Frank Keane is a coverage advisor within the Financial institution’s Markets Group.

Seth Searls is an affiliate director within the Financial institution’s Markets Group.

How one can cite this publish:

Jordan Barone, Alain Chaboud, Adam Copeland, Cullen Kavoussi, Frank Keane, and Seth Searls, “The World Sprint for Money in March 2020,” Federal Reserve Financial institution of New York Liberty Road Economics, July 12, 2022, https://libertystreeteconomics.newyorkfed.org/2022/07/the-global-dash-for-cash-in-march-2020/.

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).

[ad_2]