{kind=link}

[ad_1]

The marketplace for U.S. Treasury securities skilled excessive stress in March 2020, when costs dropped precipitously (yields spiked) over a interval of about two weeks. This was extremely uncommon, as Treasury costs usually improve throughout instances of stress. Utilizing a theoretical mannequin, we present that markets for secure property will be fragile resulting from strategic interactions amongst buyers who maintain Treasury securities for his or her liquidity traits. Fearful about having to promote at probably worse costs sooner or later, such buyers could promote preemptively, resulting in self-fulfilling “market runs” which can be much like conventional financial institution runs in some respects.

Worth Crash with Constrained Vendor Stability Sheets and Unprecedented Gross sales

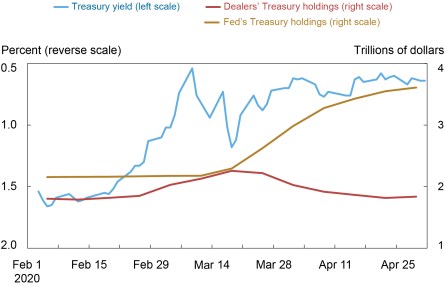

The weird occasions in Treasury markets in March 2020 have been mentioned extensively in earlier posts. We need to draw consideration to a confluence of two parts: First, the supplier banks that present Treasury market liquidity confronted mounting challenges to their intermediation capability. The chart under exhibits that supplier stability sheet area allotted to Treasury securities elevated each through the run-up in Treasury costs and their subsequent crash. The restoration in Treasury costs after March 18 coincided with supplier stability sheet stress receding because the Federal Reserve’s Treasury purchases ramped up.

Sellers Had been Constrained by the Run-up and Crash of Treasury Costs

Notes: The chart exhibits the market yield on U.S. Treasury securities at 10-year fixed maturity (reverse scale), Federal Reserve outright holdings of Treasury notes and bonds (nominal and TIPS), and Major Sellers’ web place and reverse repo in Treasury securities (nominal and TIPS).

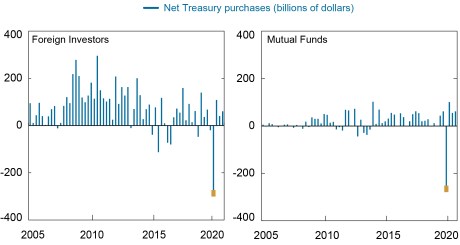

Second, the conduct of international buyers and mutual funds, the principle sellers of Treasury securities in March 2020, was very uncommon. The subsequent chart exhibits the web purchases of the 2 teams over time and highlights that their gross sales within the first quarter of 2020 had been unprecedented—a lot bigger than ever earlier than.

Unprecedented Gross sales that Seem Precautionary

Observe: The chart exhibits web purchases of Treasury securities (every type) for the 2 sectors with the biggest gross sales in 2020:Q1. “International buyers” refers back to the “remainder of the world” sector within the authentic desk.

Vissing-Jorgensen (2021) exhibits proof that each teams’ gross sales of Treasury securities exceeded their precise liquidity wants. The unprecedented magnitude of the gross sales, and the truth that a substantial fraction of them had been precautionary, makes this conduct seem similar to a run—harking back to depositors speeding to withdraw funds from a financial institution. In step with this proof, the Inter-Company Working Group for Treasury Market Surveillance (2021) reviews that “some Treasury holders appeared to react to the decline in market liquidity by promoting securities for precautionary causes lest circumstances worsen additional, and these gross sales solely added to the stress in the marketplace.”

Strategic Interplay amongst Treasury Traders Can Result in Fragility

In a latest Workers Report, we examine theoretically how strategic interplay amongst buyers could make markets fragile and result in “market runs.” We explicitly contemplate the likelihood that totally different buyers worth secure property corresponding to Treasury securities for totally different causes. Initially, secure property are secure, that means they’re anticipated to pay their full par worth at maturity with close to whole certainty. Because of this, we usually observe “flight to security” throughout instances of stress, during which demand for secure property will increase, pushing up their value. Second, secure property are liquid, and so some buyers maintain secure property to promote them when confronted with sudden liquidity wants. Throughout instances of stress, buyers’ liquidity wants can improve, competing with the same old “flight to security” and exerting downward stress on the worth of secure property after they make a “sprint for money.”

Our mannequin, which builds on Bernardo and Welch (2004), exhibits {that a} secure asset market is steady and well-functioning so long as the market is sufficiently deep. On this case, flight to security and sprint for money are complementary phenomena, with buyers who purchase the property for security absorbing gross sales from buyers who promote the property for liquidity. Nonetheless, in our mannequin, the market can break down if commerce includes sellers which can be topic to stability sheet constraints. The danger of market break-down will be self-fulfilling, because it leads buyers with out urgent liquidity must promote preemptively as a way to keep away from the potential for having to promote at decrease costs sooner or later.

Particular person buyers could choose promoting preemptively at this time in the event that they count on circumstances to deteriorate sufficiently tomorrow. Mixture gross sales at this time have a direct impact on the worth at this time, however additionally they have an oblique impact on the worth tomorrow, by their results on supplier stability sheets. If this stability sheet impact is sufficiently sturdy, a person investor’s incentive to promote preemptively will be increased if many different buyers additionally promote preemptively. When others are promoting at this time, an investor would slightly promote at this time than wait and threat having to promote tomorrow, by which era sellers could also be over-loaded with stock, leading to a lot decrease costs.

Flight to Security Can Set off a Sprint for Money

Surprisingly, we present that flight to security episodes can exacerbate the sprint for money when markets are fragile. Demand by flight-to-safety buyers early on in a stress episode will increase costs each contemporaneously and, by stress-free supplier stability sheets, sooner or later. If the strategic considerations of liquidity buyers are sufficiently sturdy, then extra demand from safety-first buyers at this time can induce liquidity buyers to promote at this time, exactly as a result of the market at this time has a comparatively increased capability to soak up gross sales. Then, a flight to security really triggers a touch for money, amplifying present market fragility.

How Was March 2020 Completely different from September 2008?

The occasions of March 2020 make a hanging distinction to the nadir of the good monetary disaster in September 2008, when Treasury markets didn’t endure from dysfunction and illiquidity. Our mannequin helps to grasp the variations between these two episodes. First, our mannequin highlights the central function of supplier stability sheet constraints which will partially be a results of post-crisis rules. Second, the liquidity wants through the COVID-19 disaster seem to have been a lot bigger—for instance, due to the disruptions from lockdowns globally. Our mannequin due to this fact means that in March 2020, the mix of unprecedented liquidity wants and significantly extra constrained sellers tilted the Treasury market right into a fragile area the place buyers promote strategically, and flight to security precipitates a touch for money.

Classes for the Future

Fragility in our mannequin hinges on the intertemporal concerns of strategic liquidity buyers who evaluate costs at this time to costs tomorrow. On the whole, there may be scope for coverage interventions that improve costs each within the current and sooner or later. Nonetheless, the timing of coverage interventions is necessary, and bulletins can have giant results nicely earlier than the interventions are executed. We present that an asset buy facility can have a big impact upon announcement by shifting strategic buyers from the “run” equilibrium to the “maintain” equilibrium, even when the power doesn’t turn out to be lively till a future date. Equally, coverage interventions that calm down supplier stability sheet constraints will be stabilizing as long as they calm down stability sheet constraints sooner or later as nicely.

Lastly, our mannequin exhibits that markets the place buying and selling happens in a decentralized, sequential approach and the place sellers play a big function in intermediating flows are inherently fragile. Adjustments to market construction whereby trades are pooled to scale back the function of sellers can due to this fact scale back the fragility of secure asset markets. Duffie (2020) argues that the expansion of the Treasury market since 2008 has drastically outpaced the capability of supplier stability sheets to soak up the extra provide and that this development is anticipated to proceed. The strategic mechanism in our mannequin is due to this fact more likely to turn out to be more and more related, suggesting that—absent coverage interventions—episodes corresponding to March 2020 could turn out to be extra frequent.

Thomas M. Eisenbach is a monetary analysis advisor in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Gregory Phelan is an affiliate professor of economics at Williams School, presently working as a senior researcher within the U.S. Treasury’s Workplace of Monetary Analysis.

Easy methods to cite this submit:

Thomas Eisenbach and Gregory Phelan, “How Can Protected Asset Markets Be Fragile?,” Federal Reserve Financial institution of New York Liberty Road Economics, September 8, 2022, https://libertystreeteconomics.newyorkfed.org/2022/09/how-can-safe-asset-markets-be-fragile/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).

[ad_2]