{kind=link}

[ad_1]

Why PPF rate of interest not elevated from 1st April 2020 onwards? Although from 1st April 2023, all of the small financial savings schemes’ rates of interest have been elevated, why did PPF curiosity stay unchanged?

The PPF fee is similar at 7.1% from 1st April 2020 to 1st April 2023. It’s nearly 3 years!! What could be the causes?

When yesterday authorities introduced the rates of interest for all small financial savings rates of interest relevant from 1st April 2023 to thirtieth June 2023, nearly all of PPF traders are indignant. As a result of the PPF rate of interest was not modified for nearly 3 years.

Why it’s so? Why authorities not performing to vary the PPF rate of interest?

Why PPF rate of interest not elevated?

Chances are you’ll bear in mind that earlier than 2016, the PPF fee was once modified quarterly. Nevertheless, efficient from 1st April 2016, the change in rate of interest will probably be as soon as 1 / 4. I’ve written an in depth publish on this “Submit Workplace Financial savings Schemes -Adjustments efficient from 1st, April 2016“. Based on this, the timetable as beneath was set to announce the rates of interest.

You seen that it was talked about within the notification that the Govt agreed and determined to recalibrate the rates of interest of all small financial savings schemes “each quarter to align the small saving rates of interest with the market charges of the related Authorities securities.”

However what is that this FIMMDA month-end G-Sec fee?

FIMMDA (Fastened Revenue Cash Market and Derivatives Affiliation of India) is a voluntary market physique for the bond, cash, and derivatives markets. They publish the Authorities Safety fee. Based mostly on these charges, the subsequent quarter’s rate of interest on numerous Submit Workplace Financial savings Schemes is taken into account.

The ten-year G-Sec bond is taken into account the benchmark for PPF and the Sukanya Samriddhi Yojana (SSY). Sukanya Samriddhi Yojana (SSY) is to have a fee of 0.75% greater than over “prevailing 10Y bond market charges” and PPF a 0.25% increased return.

These are the principles set in 2016. Nevertheless, in relation to authorities schemes like PPF, SSY, SCSS, or EPF, there’s loads of strain from the general public to have the next fee at all times. We as traders really feel a breach of belief if the rate of interest begins to fall. Nevertheless, if any authorities begins to extend it (although due to inflation and the falling bond market), we really feel it’s the BEST technique.

All these socially associated schemes’ rates of interest are typically retained as standard or elevated contemplating the general public anger, political advantages, or another conditions that are past financial implications.

That is what occurred with PPF additionally. When the brand new course of was launched on 1st April 2016, the typical yield of 10 Years G-Sec was 7.7%. As per the above rule, it needs to be 7.95%. Nevertheless, the speed was set at 8.1%. Primarily as a result of the earlier PPF fee for FY2015-16 was 8.7%. If somebody lowered it to 7.95%, then the federal government has to face the anger as it’s nearly round 0.75% fee drop!!

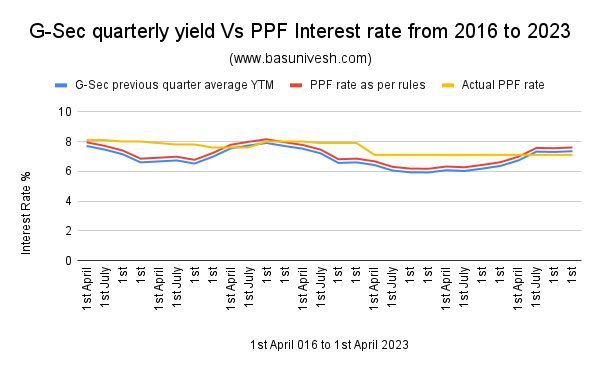

The development of getting the next fee than the precise earlier quarter’s G-Sec common YTM continued from that interval onwards. You may seek advice from the beneath chart for that goal.

Within the above chart, I’ve taken the earlier quarter’s common G-Sec yield and what needs to be the PPF fee Vs the precise fee.

You seen that from 1st April 2016 itself, the precise PPF fee was increased than the typical G-Sec yield, and in addition the PPF fee needs to be as per the principles the federal government set.

We loved the upper PPF fee throughout the decrease rate of interest regime. Now you seen {that a} 12 months on account of a rise in inflation and rate of interest, the bond markets have fallen drastically. Due to this, the yield of the bonds additionally elevated.

The yield on bonds is inversely proportional to their value. Increase in rates of interest will lead to a fall in bond costs. It will increase the yield. The reverse will occur when the rate of interest begins to fall.

Allow us to say you will have a bond with a face worth of Rs.1, 000 and the curiosity (coupon) on this bond will probably be 10%. Due to this fact, in case you purchased it at face worth and the return from this bond is 10%, then the yield on the such bond will probably be 10% (100/1000).

Now allow us to say RBI elevated the speed of curiosity to 11%, then whether or not anybody tries to purchase such bonds, which supply lower than the present market rate of interest? Clearly, no, in that case, the worth of such a bond, which bears a face worth of Rs.1,000, and coupon or yearly curiosity of 10% must fall. Allow us to say it fell to Rs.900. Then the yield will probably be 11.1% (100/900).

Why yield raised? As a result of the one that buys the bond which bears the face worth of Rs.1,000, however is presently priced at Rs.900, and the rate of interest (coupon) on such bond is mounted i.e. 10%. Due to this fact, by investing Rs.900 one can get a ten% return. Earlier you need to purchase this bond at Rs.1,000 (face worth) and the return is 10%. Now, on account of a rise within the rate of interest and a fall in bond value, the yield on such funding will enhance. Therefore, the autumn in value resulted in the next yield.

We’re presently dealing with the above scenario for round a 12 months. We as traders suppose that as financial institution FD charges and different debt devices are providing the upper fee then why is PPF curiosity not elevated?

In my opinion, the reason being that as PPF has an enormous AUM, I feel the federal government is compensating for what loss they made earlier on account of providing increased charges throughout the decrease rate of interest regime. How lengthy they’ll proceed we don’t know.

Right now morning once I tweeted about the identical as beneath.

Somebody replied saying “No, the true purpose will not be compensating however the finance secretary says for the reason that tax-free yield is increased (greater than 10% for the one falling within the highest tax bracket) subsequently there isn’t any want of accelerating the speed”.

I cannot settle for this purpose. If that’s the case, then the identical rule should additionally apply to SSY. Nevertheless, on this quarter (1st April 2023 onwards), they elevated the SSY fee however retained the PPF fee unchanged.

Contemplating all these eventualities, what I assume is that asking why the PPF rate of interest has not elevated will not be beneath our management. Although Authorities and politicians with bureaucrats float the principles, they hardly adopted them. Primarily as a result of such schemes contain loads of political repercussions quite than financial ones.

Therefore, quite than discussing or displaying anger on why the federal government not altering the rate of interest of PPF, allow us to think about what we will management (i.e investing).

Chances are you’ll add yet one more threat to your funding journey i.e POLITICAL POLICIES PARALYSIS RISK!!

[ad_2]