{kind=link}

[ad_1]

A reader asks:

I do know it’s not possible to persistently time the inventory market. However what concerning the bond market? It’s anticipated that the Fed will elevate charges all through 2022 and possibly 2023 after which minimize them once more within the close to future (presumably earlier than the elections). Isn’t the next technique a straightforward win: purchase when charges get “excessive”, promote when again to 0%? I do know these cycles aren’t speculated to be as quick as they’re now, however I don’t see a lot consideration on this technique and section.

The bond market is actually simpler to handicap than the inventory market in some ways.

Bonds are ruled extra by math than the inventory market is.

You may attempt to predict inventory market returns utilizing some mixture of dividends, earnings, GDP progress or a complete host of different components nevertheless it’s unattainable to forecast investor feelings.

And investor feelings, for higher or worse, are what set valuations and the way a lot buyers are keen to pay for sure ranges of dividends, earnings or GDP progress.

For instance, earnings grew nearly 10% per 12 months within the Seventies however stick market returns weren’t nice. Earnings grew lower than 5% per 12 months within the Eighties however returns have been improbable.

Timing the inventory market is difficult as a result of it’s troublesome to foretell within the quick run and typically the long term.

Lengthy-term returns for high-quality bonds are pretty straightforward to foretell as a result of a very powerful issue is understood prematurely — the beginning yield.

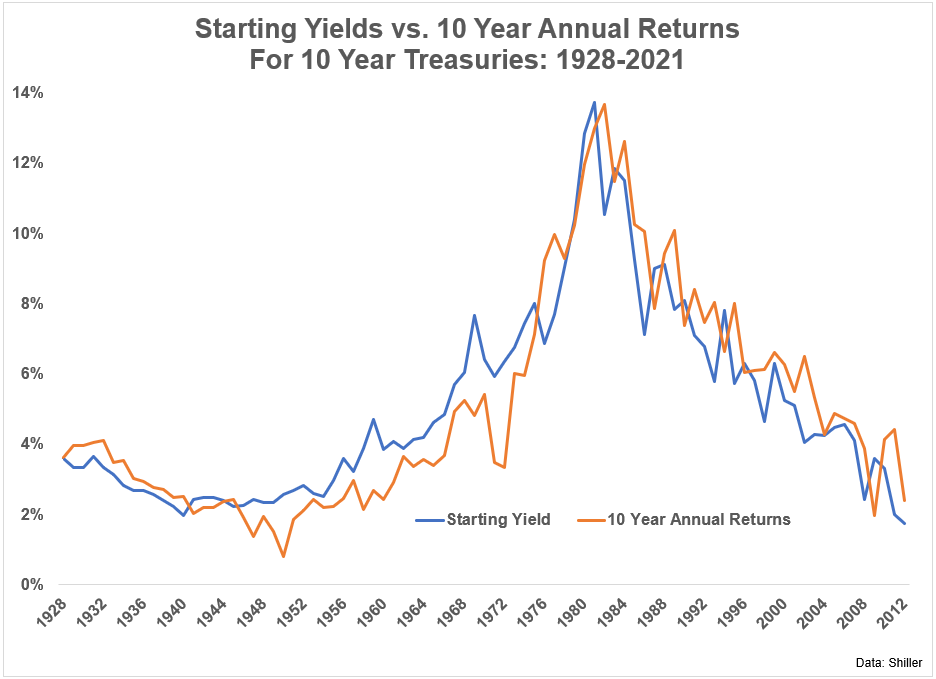

This chart reveals the beginning yield on 10 12 months treasury bonds together with the following 10 12 months annual returns:

That’s a reasonably clear chart. The correlation between beginning yields and 10 12 months returns is 0.92, that means there’s a very robust optimistic correlation right here.

If you wish to know what your future returns for bonds can be going out 5-10 years into the long run, the beginning yield will get you fairly darn shut.

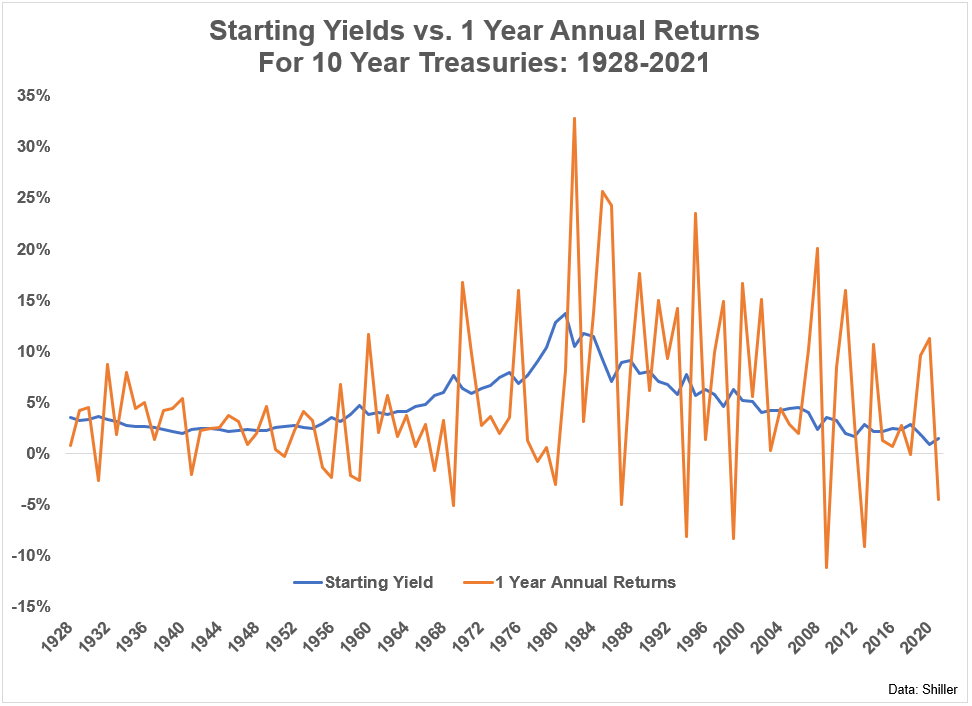

The issue is it’s not all that straightforward to foretell what’s going to occur to bonds within the meantime. Simply have a look at the beginning yields versus one 12 months returns over this identical timeframe:

It’s all around the map due to adjustments to rates of interest, inflation, financial progress and investor preferences.

Whereas long-term returns in bonds are ruled by math, the short-term remains to be ruled by feelings and financial uncertainty.

Timing the market is extraordinarily troublesome so for those who’re going to do it you want some guidelines in place. The issue is execution will seemingly be troublesome if the bond market doesn’t cooperate along with your parameters.

Let’s say you resolve to purchase bonds when charges hit 5% and promote them when charges go underneath 1%. This looks as if a reasonably affordable mannequin given what’s happening with the market.

That vary sounds fairly good proper now however what if it’s fully off going ahead?

What if the ceiling on yields is way greater than we predict proper now?

Or what if the ground is greater?

What if 0% is not the case for some time throughout a slowdown?

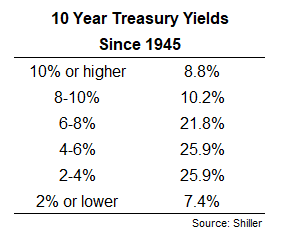

I appeared on the distribution of 10 12 months treasury yields going again to 1945:

Yields have solely ben 4% or decrease about one-third of the time. It’s attainable charges are set as much as keep a lot decrease for for much longer however that’s actually not assured.

What if charges are caught in a spread from 2% to six%? Or 3% to 7%?

In that case you find yourself shopping for too early and by no means attain your promote set off. It does appear attainable the Fed should convey charges proper again down through the subsequent recession however I don’t know what that new stage can be.

I do assume buyers are going to must be extra considerate about their mounted earnings publicity going ahead.

In an atmosphere of extra risky rates of interest you must be extra thoughtful relating to length, credit score high quality and form of the yield curve when determining what it’s you wish to get out of the bond aspect of your portfolio.

Each place in your portfolio ought to have a job and the identical is true for mounted earnings.

Are you wanting solely for yield?

Do you favor stability?

Are you available in the market for complete returns (earnings + value appreciation)?

It’s extra vital than ever to outline what it’s you’re in search of relating to bond publicity.

When you choose to maintain the volatility to the inventory aspect of your portfolio, short-term bonds appear to be a reasonably whole lot proper now.

If you wish to be extra tactical it may make sense to tackle extra length now that charges are greater and the Fed may push us right into a recession.

However it’s vital to keep in mind that attempting to time the bond market may add much more volatility to your portfolio and never in a great way.

Timing the bond market might be simpler than timing the inventory market however that doesn’t essentially imply it’s a slam dunk.

It’s a lot simpler to foretell the long-term returns on bonds than the short-term returns.

We spoke about this query on the newest version of Portfolio Rescue:

Michael Batnick joined me as properly to debate questions on municipal bond funds, information vs. uncertainty throughout bear markets, discovering a brand new job to be nearer to household and a few ideas about shopping for a house in a troublesome housing market.

When you have a query for the present, electronic mail us: AskTheCompoundShow@gmail.com

Additional Studying:

Anticipated Returns For Bonds Are Lastly Enticing

[ad_2]