{kind=link}

[ad_1]

What was our earlier view on Energetic Giant Cap Funds (in Dec-19)?

(Weblog Hyperlink)

Excessive odds of Energetic Giant Cap funds outperforming their Benchmark Nifty 100 TRI within the subsequent 2-3 years (i.e between 2020-23)!

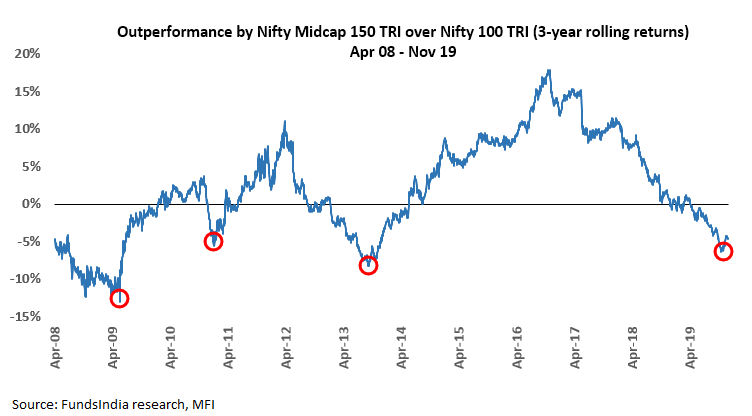

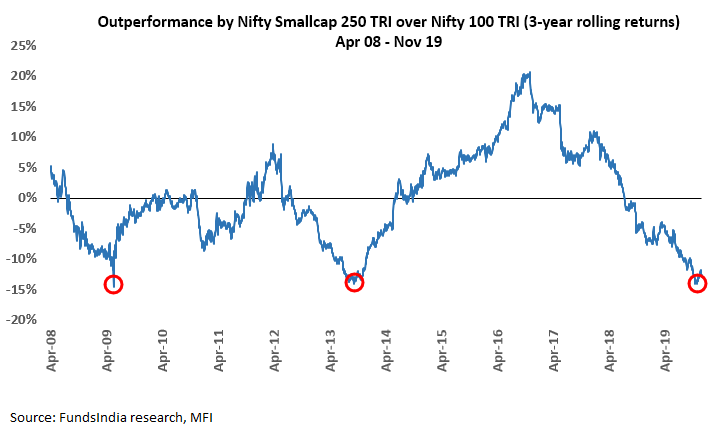

Cause 1: Mid & Small Caps had considerably underperformed Giant Caps over the earlier 3 years and we anticipated this to imply revert

- Energetic Giant Cap funds often have round 10-20% of Mid & Small Cap publicity. This had a destructive impression on the efficiency of Giant Cap funds in comparison with the pure-play Giant Cap indices for the reason that Mid & Small Cap segments underperformed Giant Caps within the earlier 3 years.

- Nonetheless, traditionally Mid/Small Cap vs Giant Cap efficiency tends to be cyclical. We had been anticipating a development reversal over the following 3-5 years the place mid/small caps outperform giant caps.

- We anticipated Energetic Giant Cap funds to have a constructive upside from their Mid & Small Cap publicity.

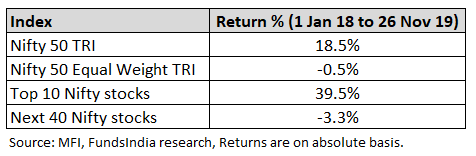

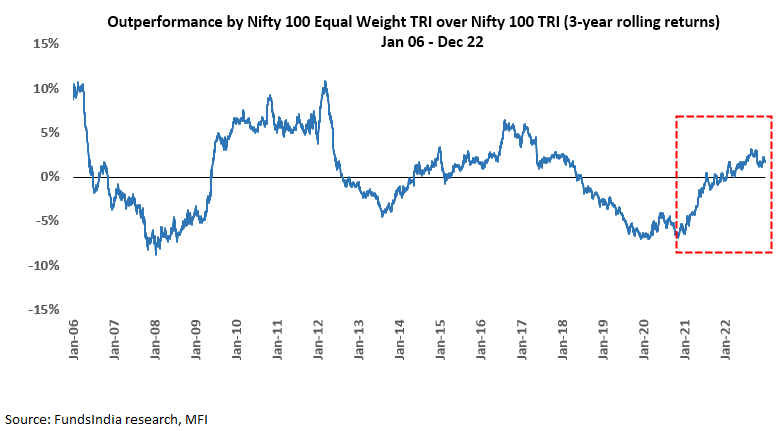

Cause 2: Part of utmost polarisation between 2017-2019 i.e few prime shares drove the index returns – led to the underperformance of diversified energetic large-cap funds. We anticipated this to imply revert.

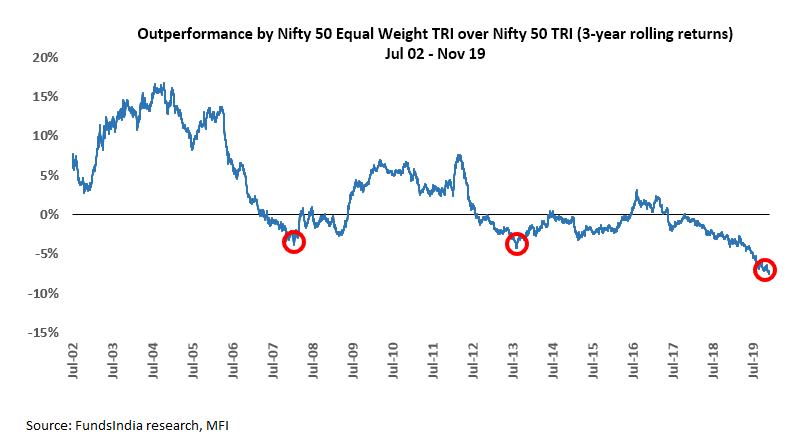

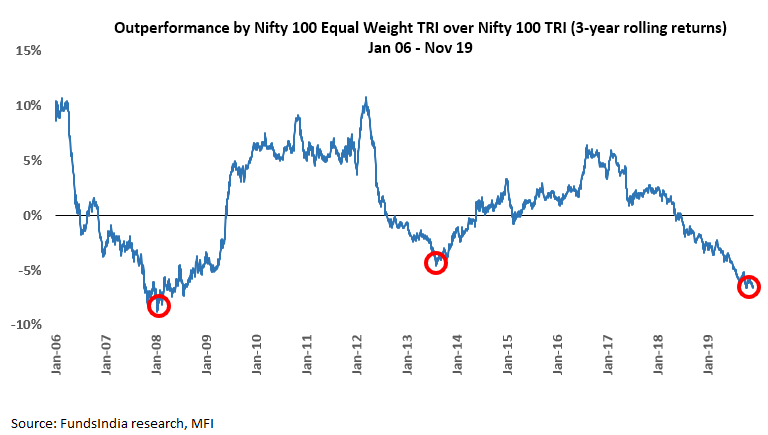

- Polarised markets seek advice from durations when few prime shares drive a big a part of returns. Between 2017-19, Nifty 50 TRI returns noticed vital polarisation – prime 10 shares drove a major a part of the returns. This led to the Nifty 50 TRI considerably outperforming the broad-based Nifty 50 Equal Weight TRI.

- As a result of impression of polarisation, diversified Giant Cap funds underperformed their benchmarks within the quick run.

- Nonetheless, over the long run, each Nifty 50 TRI and the broad-based Nifty 50 Equal Weight TRI indices had traditionally supplied related returns.

- We anticipated this Excessive Polarisation within the Giant Cap Index to imply revert and Energetic Giant Cap funds to have a constructive upside because the polarization reduces and returns get extra broad based mostly.

Did our rationale play out as per our expectations?Each views have performed out as anticipated.

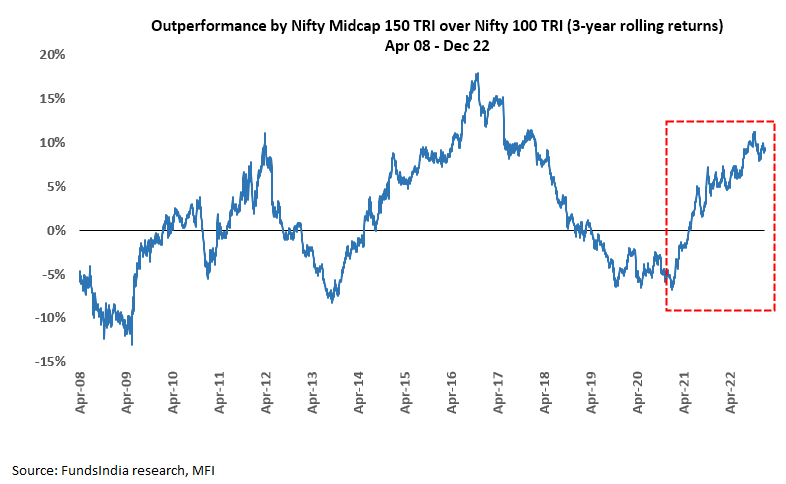

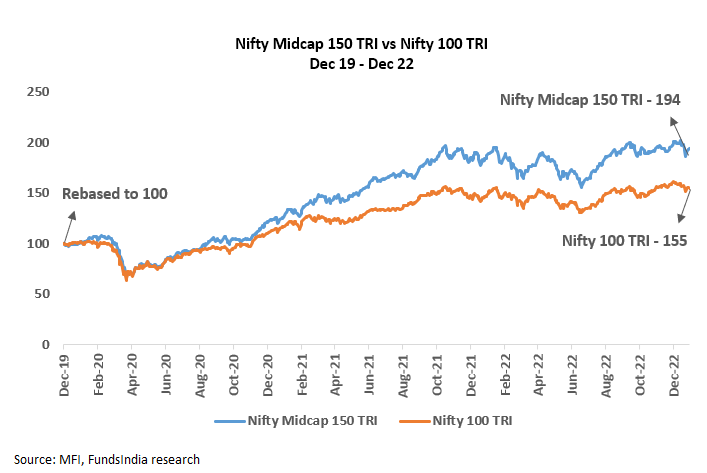

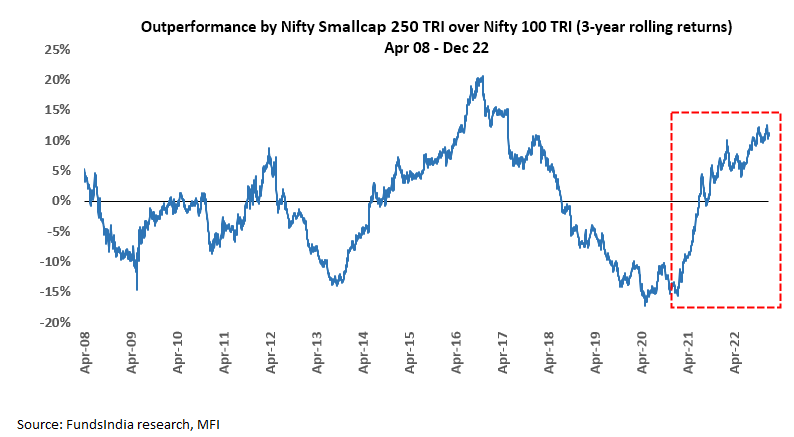

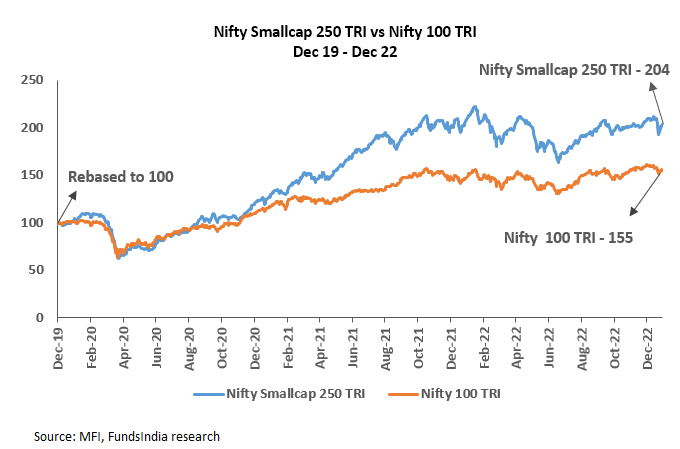

- Mid & Small Caps outperformed Largecaps

Mid Caps began to outperform Giant Caps as anticipated

Small Caps began to outperform Giant Caps as anticipated

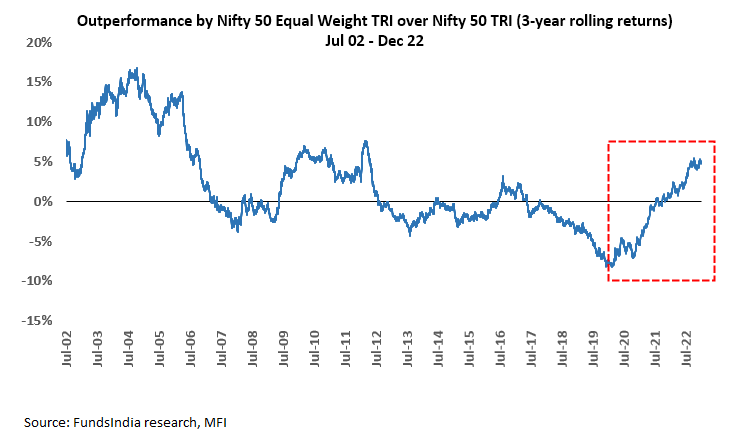

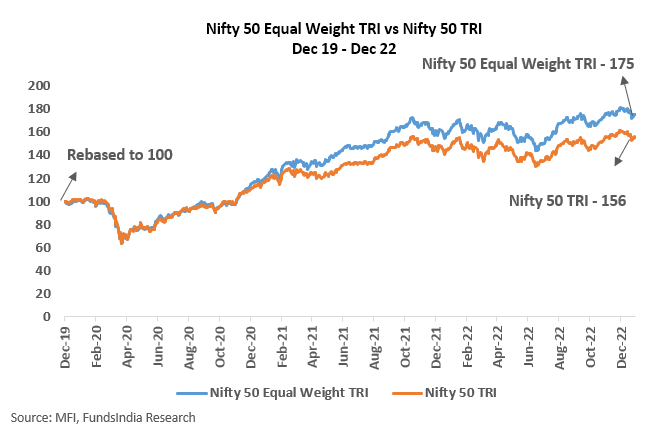

- Polarisation within the prime 10 shares lowered and efficiency bought broad-based

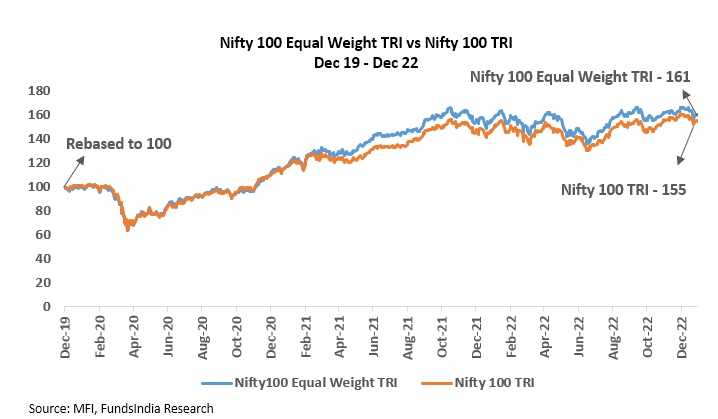

Nifty 50 Equal Weight TRI has outperformed Nifty 50 TRI as anticipated

Nifty 100 Equal Weight TRI has outperformed Nifty 100 TRI as anticipated

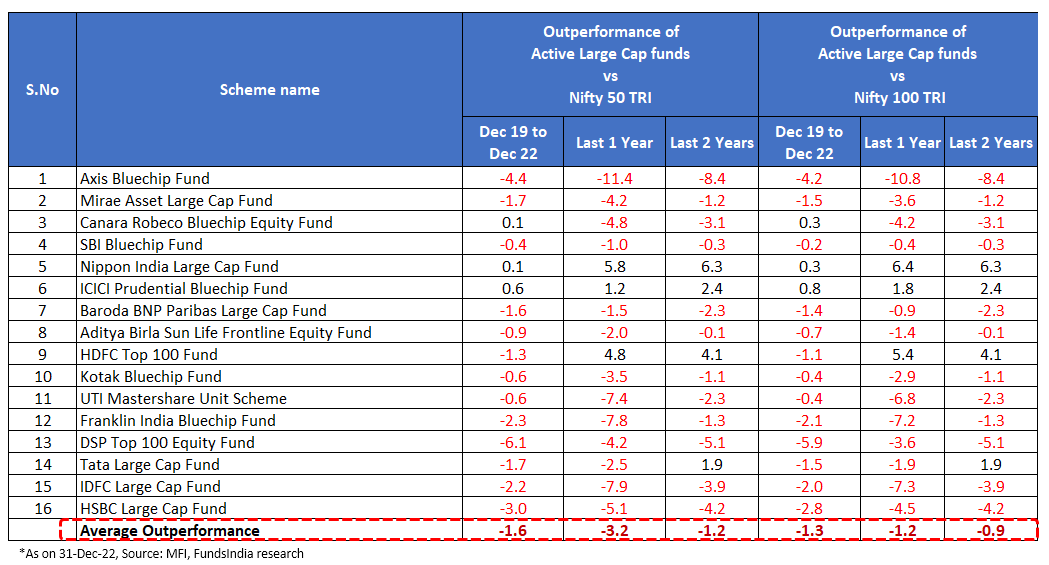

Did this translate into Giant Cap Energetic fund outperformance?

That is the place we had been stunned. Regardless of all of the above elements turning favorable and the atmosphere changing into conducive, Giant Cap Energetic funds nonetheless underperformed Nifty 50 TRI.

Whereas our rationale performed out as anticipated, Energetic Giant Cap funds are nonetheless struggling to outperform their Passive friends…

Confession time – we bought our name fallacious.

However what did we miss?

Whereas the atmosphere did flip favorable for Largecap Energetic funds, we underestimated the excessive outperformance threshold set by two main challenges.

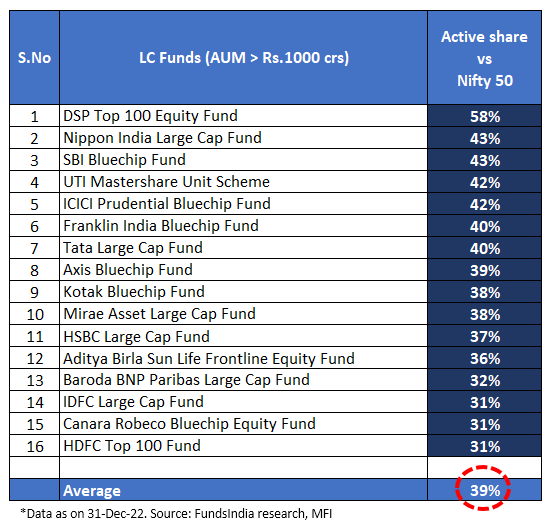

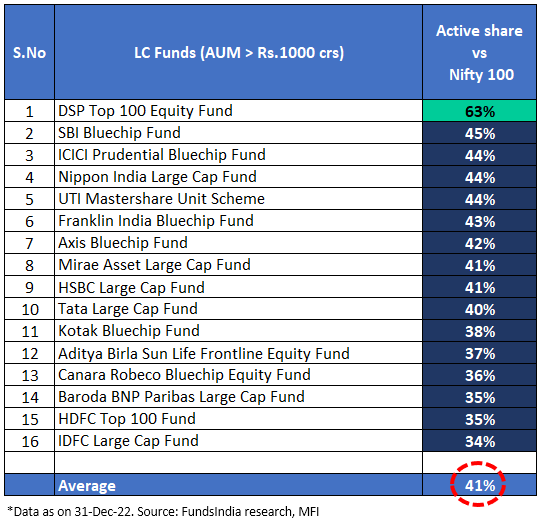

Problem 1: The Curse of Low Energetic Share (learn as excessive portfolio overlap with index)

- Energetic share measures how a lot a fund’s portfolio differs from its benchmark index. Greater the energetic share, larger the differentiated portfolio and therefore higher probabilities for outperformance

- As seen from the above desk, all of the funds (AUM > Rs.1000 crs) have a low energetic share round 40% (barring DSP High 100 Fairness Fund). In different phrases, ~60% of the portfolio for many Energetic Giant Cap funds are much like the index.

- This development of low energetic share has been exacerbated by the SEBI categorization norms introduced in 2018. This has narrowed the universe (at the very least 80% of the portfolio must be within the prime 100 shares based mostly on market capitalisation) and lowered the pliability to extend mid and small-cap publicity in giant caps as it’s capped at 20% of the portfolio.

- This makes the duty troublesome for a fund supervisor as they must outperform the index with only a small portion (~40%) of the differentiated portfolio.

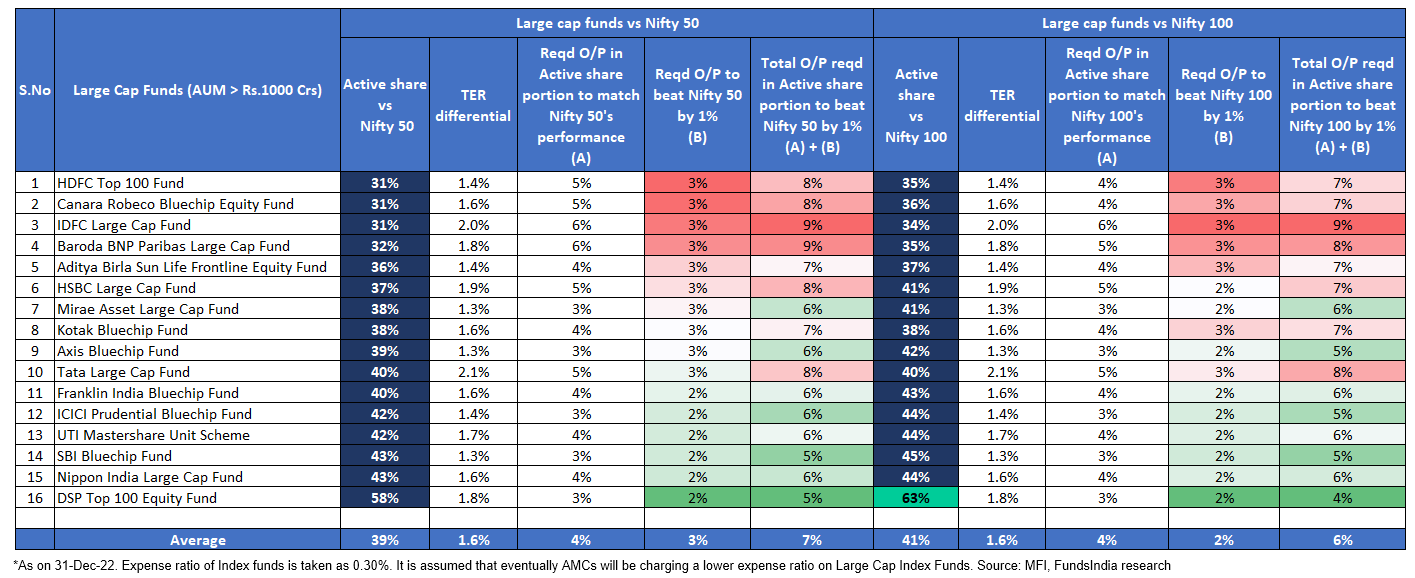

Problem 2: Excessive Expense Ratio

- Energetic giant caps are costlier than passive funds – Common expense ratio of Energetic Giant cap funds at 1.9% is considerably costlier in comparison with passive funds (eg: UTI Nifty 50 Index fund at 0.3%). Whereas some passive funds have larger expense ratios, our assumption is that with rising competitors you will see that a number of funds at 0.3% expense ratio or lesser.

…Resulting in the merciless math of outperformance

- As seen from the above desk, there’s a median distinction of 1.6% in expense ratio between actively managed Giant Cap funds and Passive Index funds.

- The differentiated portfolio (i.e energetic share) can also be low at ~40%.

- This will increase the burden of an energetic fund supervisor, because the fund supervisor should present an outperformance of round 3-4% yearly on the Energetic share portion simply to match the index returns.

- Additional, the fund supervisor should present an outperformance of round 5-7% yearly on the Energetic share portion to truly beat the index by simply 1%!!

Odds are stacked in opposition to Energetic Giant Cap Funds – Desire Passive Giant Cap Funds or Energetic Flexicap Funds

- Comparatively excessive expense ratios and low energetic share make it extraordinarily troublesome for Energetic Giant Cap funds to persistently outperform their passive friends. To place that into context, on the present energetic share ranges of ~40% and expense ratio differential of 1.6%, a big cap fund supervisor should present an outperformance of round 5-7% yearly on the Energetic share portion to truly beat the index by simply 1%!!

- Whereas there could also be a couple of energetic large-cap funds that will nonetheless outperform (through the use of levers of accelerating energetic share, concentrated portfolio, or contrarian method), it is going to be behaviorally difficult to stay to those funds because the efficiency is anticipated to be cyclical and huge outperformance could are available spurts following durations of underperformance.

- Given the above context, we choose to progressively transfer out of Energetic Giant Cap funds and as a substitute spend money on Passive Giant Cap Index funds or Energetic Giant Cap Biased Flexi Cap Funds (60-80% giant caps with the pliability to extend mid/small cap allocation) for taking part within the large-cap section.

What’s going to make us change our view?

- Enhance in Energetic share: If the Energetic share of Energetic Giant Cap Funds will increase above 60%, we’ll revisit our view

- Decreasing of Expense ratios: If the Expense ratio hole between Energetic & Passive Giant Cap fund reduces, we’ll revisit our view

Different articles chances are you’ll like

Publish Views:

42

[ad_2]