{kind=link}

[ad_1]

Common auto use is just 4% of every day, but a brand new automobile buy regularly prices 50% of somebody’s annual earnings.[i] While you add in taxes, gasoline, insurance coverage, and upkeep, many individuals can’t make a logical case for possession. That is very true in city areas, the place mobility choices are plentiful and on the rise. Regardless of these details, auto possession can also be on the rise. If we take a look at the entire mobility image, auto insurance coverage will stay related whereas on the similar time non-traditional transportation insurance coverage goes to start to develop, notably as individuals proceed to make use of their autos to earn extra cash through ride-sharing corporations. This creates a necessity for “hybrid” P&C mobility merchandise.

E-bikes, for instance, are a rapidly-growing mobility choice for individuals who want to buy a inexpensive solution to commute. They’re additionally out there by large bike-share networks, akin to Chicago’s Divvy system of bikes and e-bikes.

E-bikes aren’t the one mobility choice that’s on observe for progress, however they make an excellent working example. They test the bins for developments that might disrupt auto use and auto insurance coverage. They’re extremely economical. They’re sooner than conventional bikes (roughly 21% sooner per journey).[ii] Should you’re utilizing them for a commute, you’re much less prone to arrive at work exhausted and sweaty. They’re straightforward on the surroundings. They offer you some freedom to go the place you want to go with out sticking to a public transit route. Transport corporations, akin to UPS, are even contemplating e-bikes for last-mile supply.

E-bikes have even been proven to encourage individuals to trip extra, and since e-bikes use pedal-assist expertise, the online impact could possibly be that e-bike customers enhance their well being.

After all, there’s a flip aspect to e-bikes that includes insurance coverage. Attributable to their potential velocity (20 mph), they’re much less secure than a conventional bike. Their parts value extra to exchange in an accident declare. Their riders could have much less two-wheel expertise as a result of E-bikes are interesting to some riders that may not usually trip a conventional bike as a result of age, well being, or hilly terrain.

Despite the fact that e-bikes aren’t going to displace autos anytime quickly, P&C insurers want to understand their potential influence, together with the influence of car-sharing, ridesharing, transit enhancements, work-from-home existence, and using private autos for enterprise use. Mobility is altering and insurance coverage might want to shift to seize the alternatives it would create.

For a number of years now, Majesco has been monitoring and understanding how we transfer.

In our earlier Mobility analysis, we famous the numerous change in automotive exercise is leading to corporations exterior insurance coverage coalescing round a shift to the idea of “mobility.” From the decline in automotive possession for the primary time since 1960, to the rise of ride-hailing and car-sharing companies, a plethora of transportation choices continues to broaden – therefore the concentrate on mobility. On this yr’s Client Analysis report, Majesco regarded on the shopper developments with the best influence on P&C insurers. You may dig deeper into these shifts by studying, Your Insurance coverage Prospects: A Crystal Ball of Large Modifications in a Small Window of Time. At present, we’re making a case for mobility. Does your group grasp how the approaching mobility shift requires insurers to rethink services and products that match these new dangers?

Mobility in movement

Let’s take a look at the place mobility is in the present day. In line with the American Time Use Survey, the share of individuals touring in 2020 dropped by 17 share factors, to 67% from 84% in 2019[iii] – probably pushed by the distant work surroundings.

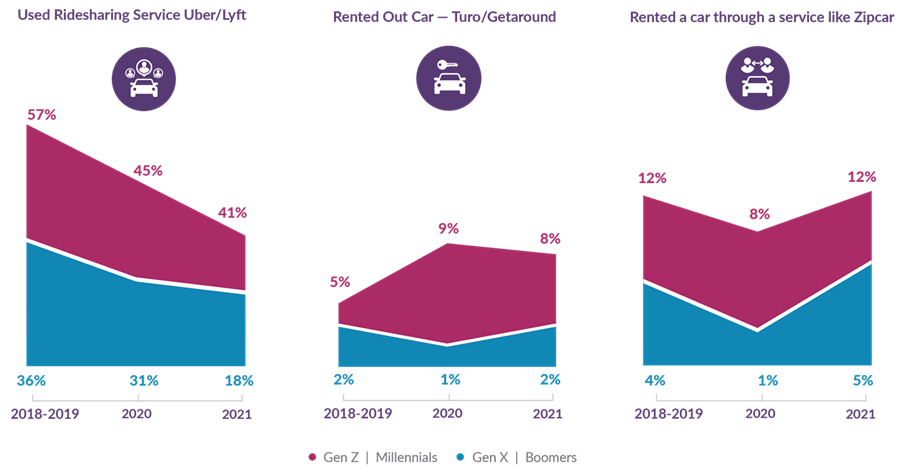

The usage of rideshare companies like Uber and Lyft dropped when COVID hit in 2020 and continued to say no, particularly amongst Gen X & Boomers. Gen Z & Millennials proceed to worth mobility as they use new mobility choices like e-bikes or scooters or short-term rental of automobiles from a service like Zipcar or one other particular person’s automotive by a platform like Turo or Getaround.

Determine 1: Mobility exercise developments

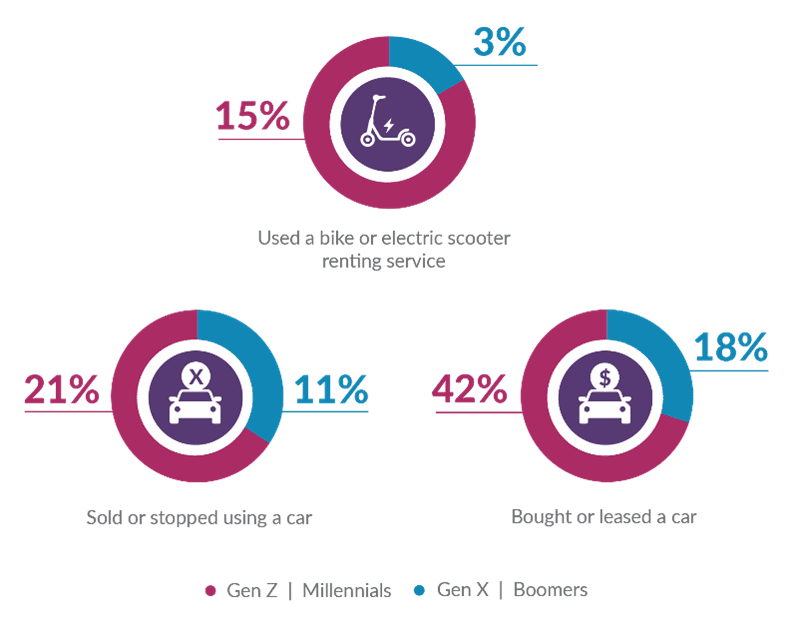

Nevertheless, the auto continues to be vital to Gen Z & Millennials. They purchased and/or offered a automobile at over twice the speed of Gen X & Boomers, with 42% indicating they purchased or leased a automotive, 21% offered a automotive, and 28% both added a automotive or purchased their first automotive.

Determine 2: Mobility actions previously yr

Within the subsequent three years, cars ought to see a resurgence. Gen Z & Millennials particularly will likely be shopping for/leasing new autos and count on to be driving greater than they at present do. This implies two key potential shifts in auto insurance coverage:

- First, the favored UBI-based insurance coverage, which has seen progress as a result of COVID and distant work, could should be tailored past simply miles pushed, to think about the place and methods to handle buyer worth and value expectations.

- Second, the surge in shopping for new autos which have embedded, refined applied sciences for telematics, sensors, and driverless capabilities, in addition to progressive companies, will probably create demand for embedded insurance coverage within the buy from the producer. More and more, auto producers both provide or are quickly to supply embedded insurance coverage. This shift requires insurers to supply comparable coverages and companies to retain prospects or to companion with vehicle producers.

Regardless, the expansion in new, technically refined autos would require insurers to maneuver past each conventional auto and UBI insurance coverage merchandise to new choices that mirror existence and behaviors, and are inclusive of value-added companies.

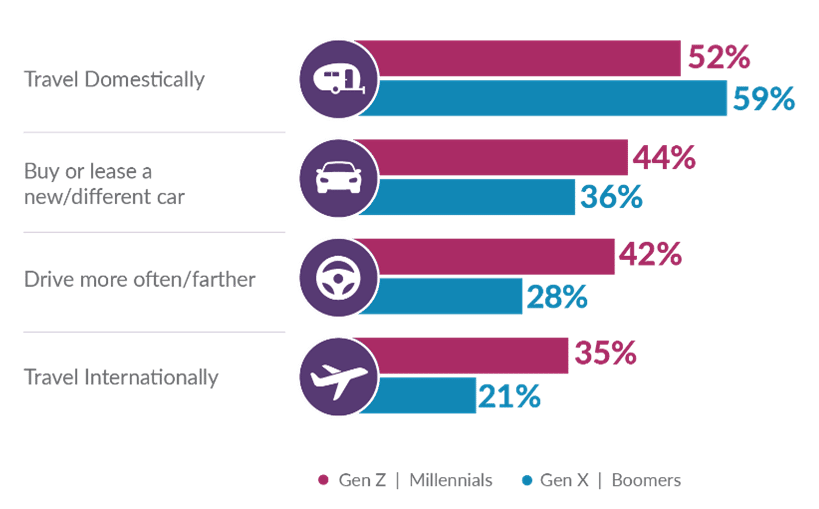

Moreover, with the easing of COVID restrictions, the pent-up demand for journey, particularly throughout the U.S., is predicted to develop. This presents a market alternative to supply on-demand protection for particular occasions, journeys, mobility choices, and bundled packages, akin to American Household’s Street Journey Accident Lodging Protection. Moreover, the rise of journey through planes and the challenges with airways has seen a rise in demand for journey insurance coverage.

Determine 3: Mobility expectations within the subsequent 3 years

How will prospects purchase the mobility insurance coverage they want?

From a product perspective, prospects count on an increasing array of merchandise to satisfy their altering behaviors, wants, and expectations. The Gen Z & Millennial technology is vastly totally different than the older technology, each when it comes to their life-style but in addition their digital savvy and life journey. Nevertheless, each nonetheless need digital and multi-channel choices in addition to a rising array of value-added companies.

This presents vital implications in addition to alternatives for insurers, all primarily based on how quickly they plan and execute towards them. Many InsurTech start-ups and incumbent insurer greenfields are particularly focusing on the Gen Z & Millennial technology with new, progressive merchandise, value-added companies, and experiences which are vastly totally different than most conventional insurers.

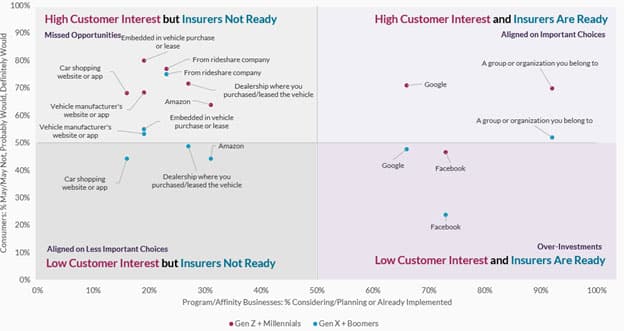

Majesco analyzed shopper information towards insurer information from a joint analysis venture with PIMA in 2020 for program enterprise and affinity plans for 3 insurance coverage segments (Life/Heath/Accident, Auto, and Dwelling/Renter). You may see extra on Life/Well being/Accident and Dwelling/Renter by downloading the Client Analysis report. Our evaluation was aimed toward determining if insurers are aligned to buyer sentiment relating to how they want to purchase auto/mobility insurance coverage.

Product and Channel Alignment

The prime alternatives lie in areas the place there may be excessive buyer curiosity in a selected insurance coverage channel, and insurers are prepared to maneuver into that channel. That’s represented within the prime proper quadrant in determine 4. Nevertheless, the best breadth of alternative lies in areas the place prospects are able to buy by a selected channel, however insurers aren’t ready to make the most of that channel. That’s represented by the highest left quadrant in determine 4.

Determine 4: Auto insurance coverage channel alignment/misalignment

Buyer Expertise

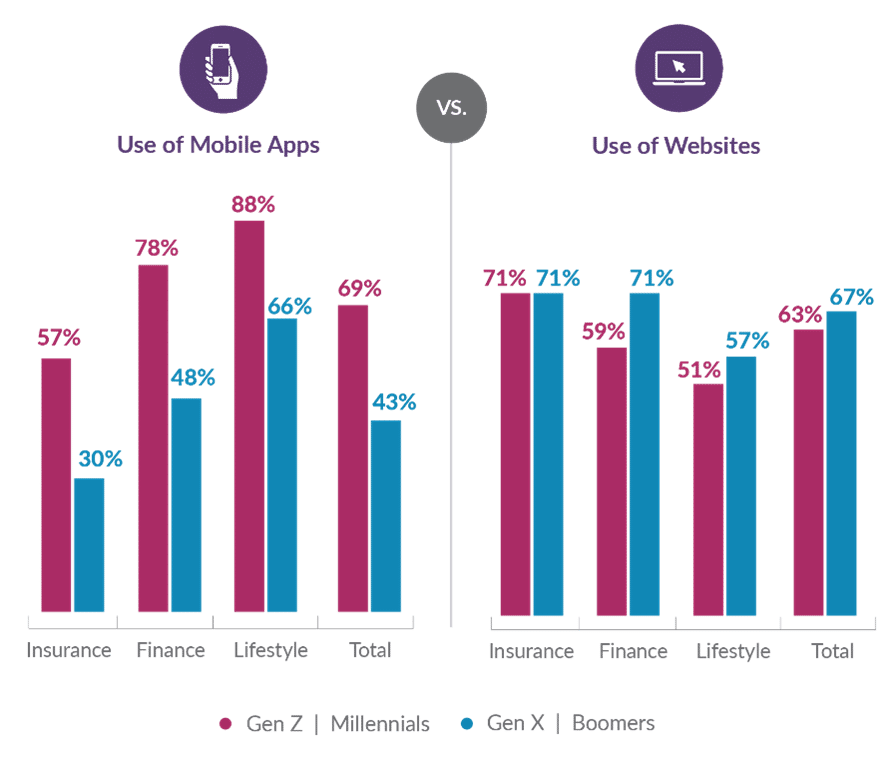

There may be additionally appreciable insurer-customer misalignment within the buyer expertise. Each technology segments use web sites at comparable ranges for managing insurance coverage, finance, and life-style services and products. Nevertheless, insurance coverage falls woefully behind in giving prospects the power to handle their services and products with cell apps. That is particularly regarding with Gen Z & Millennials, whose use of apps is 21 and 31 share factors greater for finance and life-style services and products, respectively. These are gaps that should be closed by insurers.

Determine 5: Use of digital instruments to handle accounts

A latest Service Administration article famous how even individuals who have been beforehand averse to utilizing expertise for on a regular basis duties have embraced it, citing an AARP examine that discovered the share of U.S. adults over 50 years outdated (Gen X & Boomer phase) utilizing a smartphone to make monetary transactions rose to 53% in 2020, up from 37% from 2019.[iv]

Looking for a holistic resolution

Insurance coverage is headed in a path the place new merchandise, akin to the type that can cowl all elements of mobility, should be offered by utterly new varieties of channels that match with buyer expertise preferences.

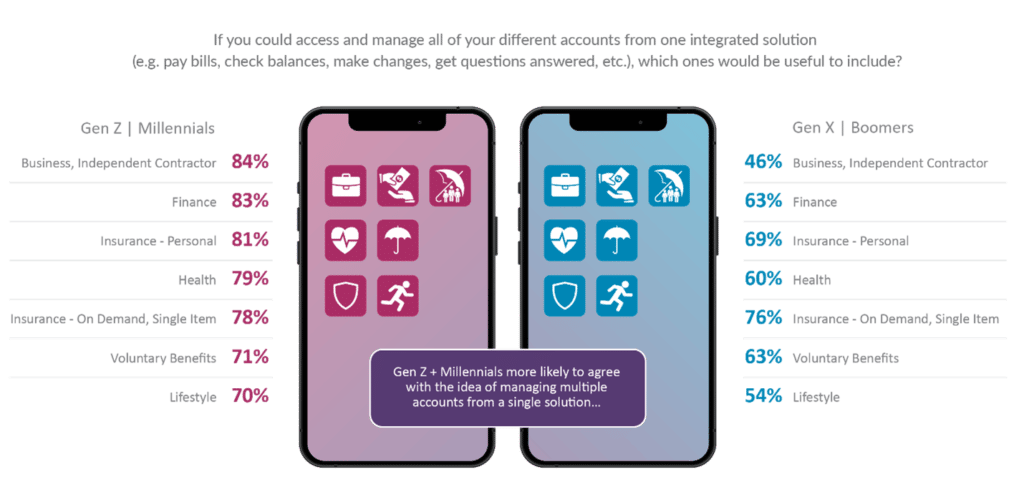

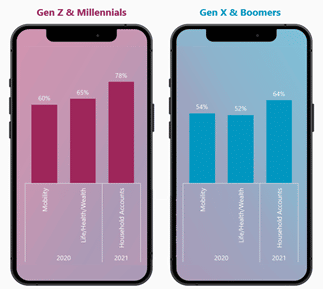

Zurich Group Chief Claims Officer, Ian Thompson, mentioned just lately that “the pre-pandemic period was overly-focused on constructing an ‘app’ by which prospects must interact.” At present the main focus is on making a holistic expertise throughout totally different merchandise, companies, and channels. As we famous in final yr’s shopper analysis report, the holistic expertise was strongly desired by the youthful technology, whereas of curiosity by the older technology in sure areas. The 2021 information signifies for each generational teams that is nonetheless sturdy (Determine 6) and rising even stronger in comparison with final yr (Determine 7. Word: The 2021 “Family Accounts” figures symbolize the common curiosity throughout all classes in Determine 6).

Determine 6: Buyer curiosity in a holistic resolution to handle all of their accounts

Determine 7: Elevated curiosity in a holistic resolution, 2021 vs 2020

If we take each of those wants under consideration (built-in account options and holistic insurance coverage options), we see that prospects are asking for the neatest and quickest methods to maintain them utterly coated. They need insurance coverage to be included in holistic account administration options.

What does this sort of resolution appear like?

Our greatest choice is to take a look at mobility insurance coverage by the eyes of a buyer. If a buyer might select the perfect insurance coverage expertise throughout all of their transportation choices, how would possibly it work?

Ideally, a holistic mobility insurance coverage expertise can be low-touch. In in the present day’s digital world, it’s doable for a cellular phone to know whether or not it’s transferring by rail, bike, automotive, or foot. With UBI on the rise, and superior, real-time information evaluation, maybe commuters might merely be coated and charged, primarily based on their precise motion. This could match their need to obtain pricing that’s aligned with expertise.

Insurance coverage buy might occur at one in every of many junctures in life; the acquisition of a automotive, the acquisition of a motorbike, or through a QR code on an advert at their favourite espresso store. Claims could possibly be app-based or auto-generated communications. Customer support might occur by textual content or by telephone. Worth-added companies like reminders or journey alerts might maintain prospects secure. (e.g. “There may be an 85% probability of heavy rain in the present day.”)

The hot button is flexibility. Wherever mobility strikes, insurers transfer with it. This requires insurers to maneuver now.

Buyer wants and expectations are dramatically totally different now. The accelerated tempo of digital expectations is considerably totally different. The entry to and use of knowledge are very totally different. Channel and companion choices are exponentially totally different. The enterprise working mannequin and expertise of the previous won’t help success for in the present day and the long run.

Alternative exists for individuals who shift their working mannequin and expertise to satisfy the client on their phrases.

Ask your self:

- Are you prepared for a better concentrate on customer-driven digital transformation?

- Does your expertise speed up your digital transformation?

- Are you able to make the most of digital in your bid to grow to be a aggressive and related insurance coverage chief and obtain the worthwhile progress that comes with it?

- What particular plans can you are taking to enhance your odds of success?

To organize your self for insurance coverage buyer developments, you’ll want to learn, Your Insurance coverage Prospects: A Crystal Ball of Large Modifications in a Small Window of Time. For Majesco’s associated SMB developments analysis, obtain, A Quickly-Altering SMB Panorama.

[i] 2018 Evolution of Mobility Research, 2019, Cox Automotive and Mobility

[ii] Bernsten, Sveinung, Lena Maines, Aleksander Langaker, Elling Bere, Bodily exercise when driving and electrical assisted bicycle, Worldwide Journal of Behavioral Vitamin and Bodily Exercise, April 26, 2017.

[iii] “American Time Use Survey Abstract,” op. cit.

[iv] French, David, “Digital Attraction Waning; Insurance coverage Claimants Heading Again to People,” Service Administration, November 21, 2021, https://www.carriermanagement.com/information/2021/11/21/229276.htm

[ad_2]