{kind=link}

[ad_1]

This put up presents an replace of the financial forecasts generated by the Federal Reserve Financial institution of New York’s dynamic stochastic common equilibrium (DSGE) mannequin. We describe very briefly our forecast and its change since June 2022.

As traditional, we want to remind our readers that the DSGE mannequin forecast isn’t an official New York Fed forecast, however solely an enter to the Analysis employees’s general forecasting course of. For extra details about the mannequin and variables mentioned right here, see our DSGE mannequin Q & A.

The New York Fed mannequin forecasts use knowledge launched by means of 2022:Q2, augmented for 2022:Q3 with the median forecasts for actual GDP development and core PCE inflation from the August launch of the Philadelphia Fed Survey of Skilled Forecasters (SPF), in addition to the yields on 10-year Treasury securities and Baa-rated company bonds, primarily based on 2022:Q3 averages as much as August 26. As well as, for every quarter beginning in 2021:This autumn, the anticipated federal funds charge between one and 6 quarters into the long run is restricted to equal the corresponding median level forecast from the newest out there Survey of Main Sellers (SPD) in that quarter. For the present projection, that is the July SPD.

The outlook in comparison with June is barely extra pessimistic when it comes to inflation, and broadly unchanged when it comes to actual exercise. This evolution of the projections is the results of two forces. On the one hand, the mannequin sees the underlying state of the actual economic system as stronger than it did in June, as evidenced by the upper projections for the actual pure charge of curiosity (1.4 % versus 0.9 % for 2022, 1.2 % versus 0.9 % for 2023, and 1.0 % versus 0.9 % for 2024). Alternatively, financial coverage is predicted to be considerably tighter than in June, not solely in absolute phrases but in addition relative to the extra elevated actual pure charge.

These two forces roughly cancel each other out when it comes to output development. Output development is projected to be barely decrease for 2022 (-0.7 % versus -0.6 %), largely because of the truth that Q2 development was decrease than nowcasted by the SPF in Might. The mannequin tasks barely greater development for 2023 (-0.4 % versus -0.5 %) and as soon as once more lowers the expansion forecast for 2024 (0.1 % versus 0.4 %). For 2025, the mannequin expects development to nonetheless be under development, partly as a result of financial coverage stays fairly tight in its projections. The DSGE nonetheless sees a reasonably excessive chance of a recession within the subsequent couple of years. The likelihood of a not-so-soft touchdown–outlined as four-quarter GDP development dipping under -1 %, as occurred throughout the 1990 recession, a minimum of as soon as over the following ten quarters–stays about 80 %. The output hole is predicted to show detrimental within the medium time period, declining from 0.8 % on the finish of 2022 to -0.3 % in 2023, -1.2 % in 2024, and -1.7 % in 2025.

The modified evaluation of the underlying energy of the economic system has implications for the inflation projections as nicely. The mannequin attributes the present excessive inflation much less to transitory components, reminiscent of provide disruptions, and extra to persistent components. As a consequence, the mannequin tasks that inflation will stay elevated in 2022 at 4.1 %, up 0.3 proportion factors relative to June, and decline solely progressively thereafter (to three.1, 2.6, and a couple of.4 % in 2023, 2024, and 2025, respectively—versus projections of two.5, 2.1, and a couple of.0 % in June). As a result of the Phillips curve is estimated to be flat within the DSGE, tighter financial coverage has a restricted impact on the projected course of inflation.

Forecast Comparability

| 2022 | 2023 | 2024 | 2025 | |||||

|---|---|---|---|---|---|---|---|---|

| Sep | Jun | Sep | Jun | Sep | Jun | Sep | Jun | |

| GDP development (This autumn/This autumn) |

-0.7 (-2.3, 0.8) |

-0.6 (-3.6, 2.3) |

-0.4 (-5.2, 4.4) |

-0.5 (-5.0, 4.0) |

0.1 (-4.7, 4.9) |

0.4 (-4.4, 5.3) |

0.7 (-4.5, 5.9) |

1.4 (-3.9, 6.5) |

| Core PCE inflation (This autumn/This autumn) |

4.1 (3.8, 4.4) |

3.8 (3.3, 4.4) |

3.1 (2.3, 3.8) |

2.5 (1.7, 3.4) |

2.6 (1.7, 3.5) |

2.1 (1.2, 3.1) |

2.4 (1.4, 3.4) |

2.0 (1.0, 3.0) |

| Actual pure charge of curiosity (This autumn) |

1.4 (0.2, 2.6) |

0.9 (-0.4, 2.1) |

1.2 (-0.3, 2.6) |

0.9 (-0.5, 2.4) |

1.0 (-0.6, 2.6) |

0.9 (-0.7, 2.4) |

0.9 (-0.7, 2.6) |

0.8 (-0.9, 2.5) |

Notes: This desk lists the forecasts of output development, core PCE inflation, and the actual pure charge of curiosity from the September 2022 and June 2022 forecasts. The numbers outdoors parentheses are the imply forecasts, and the numbers in parentheses are the 68 % bands.

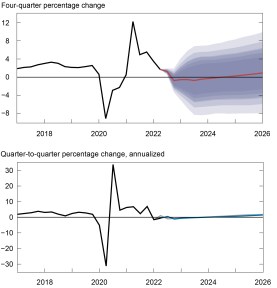

Forecasts of Output Progress

Notes: These two panels depict output development. Within the prime panel, the black line signifies precise knowledge and the pink line exhibits the mannequin forecasts. The shaded areas mark the uncertainty related to our forecasts at 50, 60, 70, 80, and 90 % likelihood intervals. Within the backside panel, the blue line exhibits the present forecast (quarter-to-quarter, annualized), and the grey line exhibits the June 2022 forecast.

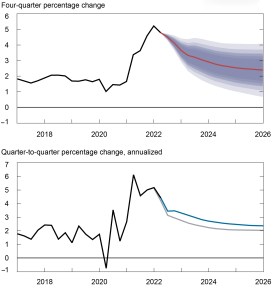

Forecasts of Inflation

Notes: These two panels depict core private consumption expenditures (PCE) inflation. Within the prime panel, the black line signifies precise knowledge and the pink line exhibits the mannequin forecasts. The shaded areas mark the uncertainty related to our forecasts at 50, 60, 70, 80, and 90 % likelihood intervals. Within the backside panel, the blue line exhibits the present forecast (quarter-to-quarter, annualized), and the grey line exhibits the June 2022 forecast.

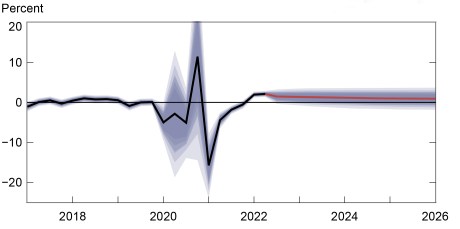

Actual Pure Fee of Curiosity

Notes: The black line exhibits the mannequin’s imply estimate of the actual pure charge of curiosity; the pink line exhibits the mannequin forecast of the actual pure charge. The shaded space marks the uncertainty related to the forecasts at 50, 60, 70, 80, and 90 % likelihood intervals.

The DSGE mannequin is a product of the New York Fed’s Utilized Macroeconomics and Econometrics Middle (AMEC). To be taught extra about AMEC’s work, please go to the Middle’s web site.

Marco Del Negro is an financial analysis advisor in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Keshav Dogra is a senior economist in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Aidan Gleich is a senior analysis analyst within the Financial institution’s Analysis and Statistics Group.

Donggyu Lee is a analysis economist in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ramya Nallamotu is a senior analysis analyst within the Financial institution’s Analysis and Statistics Group.

Sikata Sengupta is a senior analysis analyst within the Financial institution’s Analysis and Statistics Group.

The best way to cite this put up:

Marco Del Negro, Keshav Dogra, Aidan Gleich, Donggyu Lee, Ramya Nallamotu, and Sikata Sengupta, “The New York Fed DSGE Mannequin Forecast—September 2022,” Federal Reserve Financial institution of New York Liberty Avenue Economics, September 23, 2022, https://libertystreeteconomics.newyorkfed.org/2022/09/the-new-york-fed-dsge-model-forecast-september-2022/.

[ad_2]