{kind=link}

[ad_1]

Readers know that I way back concluded that energetic administration not often provides worth to an investor’s portfolio. There are too many managers preventing over the identical shares. Only a few of them have a significant Edge over the others. Most of those that add some worth not often add sufficient to beat the drag imposed by their bills and better tax burden. Some few add critical worth, however they’re virtually unimaginable to reliably determine prematurely.

That mentioned, I’m about to commit two heresies in a single column: I’ll counsel that you just contemplate investing internationally, and for those who select to take action, I’ll counsel that you just contemplate entrusting your cash to an skilled energetic supervisor. (I do know. It shocked me, too.)

Worldwide equities and a superb query:

“Why do you continue to put money into the worldwide markets (shares exterior the USA)?” I used to be requested by a extremely astute head of a big household workplace at a latest lunch. The query was in response to my description of an asset allocation portfolio that invested in U.S., Worldwide, and Rising Markets Shares, together with Bonds and REITs.

The final decade has not been variety to international shares:

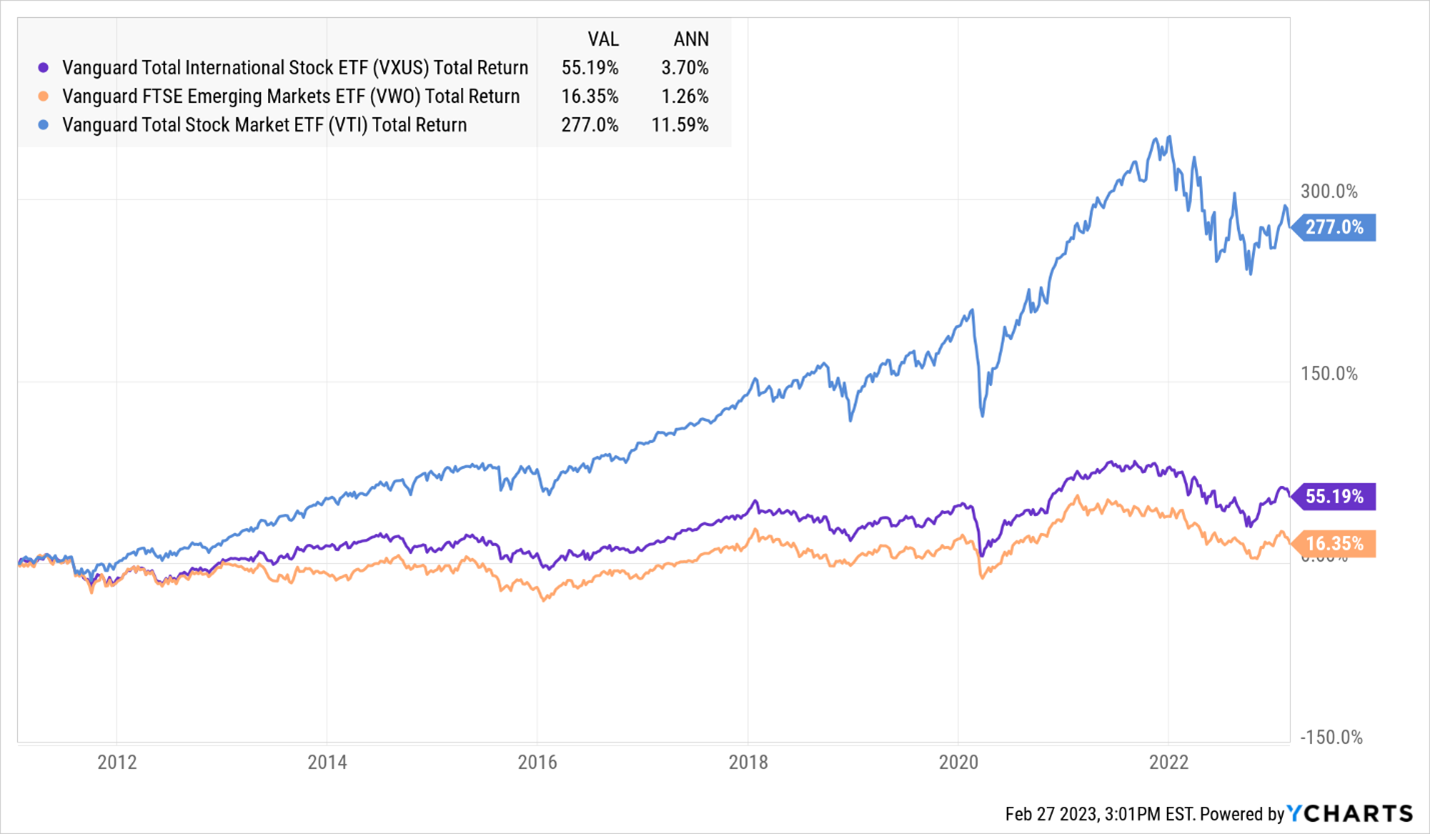

It takes one take a look at the next chart to find out the idea for his query. From the beginning of 2009 to Feb-end 2023, U.S. equities measured by the returns of the Vanguard Whole Inventory Market ETF (VTI) loved a complete return of 277%, whereas the Vanguard Worldwide Developed Markets (VXUS) returned 55%, and Vanguard Rising Markets (VWO) solely 16% (or an annualized return of 1%, simply 1% a 12 months … a return I’d have crushed with a fastidiously timed funding in a lemonade stand!!). Since that features dividends, the value returns are even much less.

His arrow, subsequently, was aimed on the follow of the Vanguard concept of low-cost, passive, broad-based investing – besides this time in international and rising markets shares. Whereas within the a long time previous, it was thought-about acceptable to say some nonsense like “the diversification advantages of investing in a significant asset class uncorrelated to U.S. equities,” anybody with cash in these international markets is aware of higher. It’s now clear that the thought of passive investing that works so nicely in the US has been a catastrophe when international fairness property.

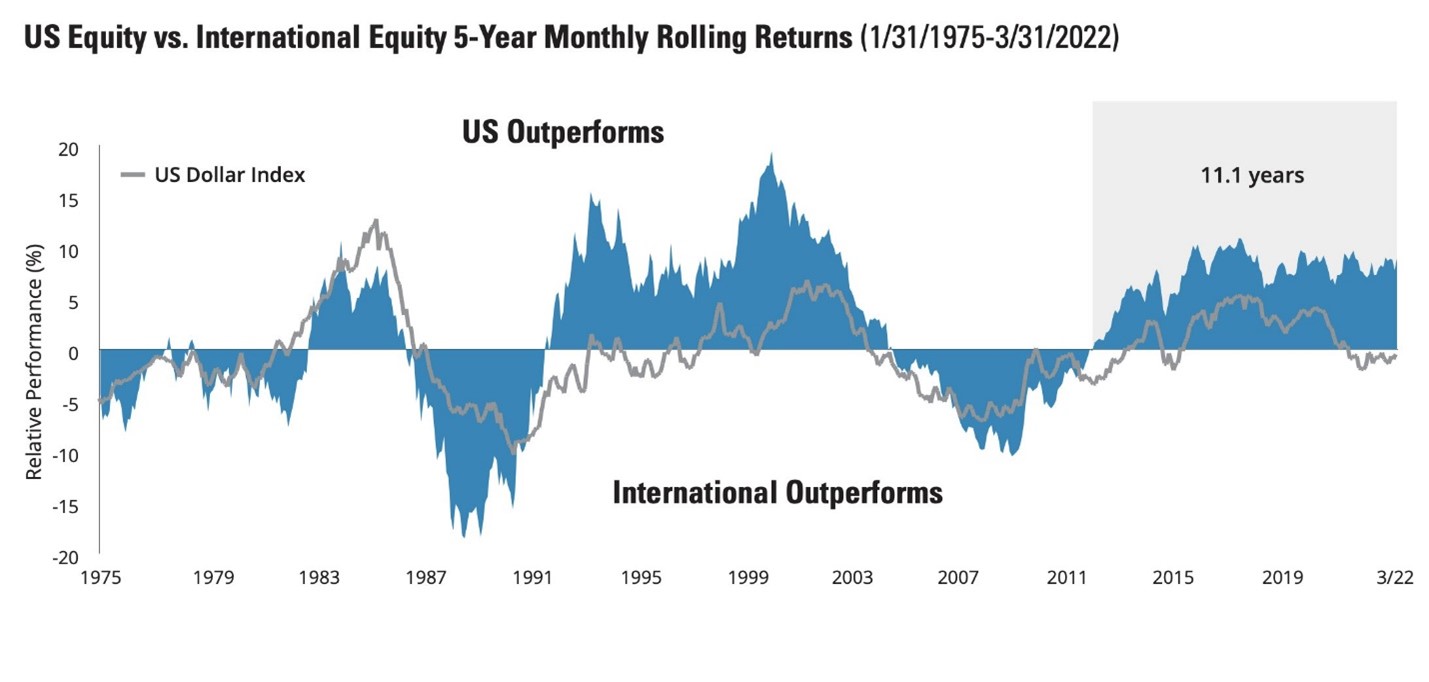

That decade-long lag raises two necessary views. First, as a result of valuations globally are decrease than valuations domestically, many capital fashions venture a decade of worldwide outperformance relative to U.S. shares. Charles Schwab’s capital mannequin, as an example, tasks a 150 bps benefit for worldwide massive caps over home ones with returns of seven.6% versus 6.1% yearly. Second, the mere existence of a interval of U.S. outperformance shouldn’t be exceptional. Traditionally, U.S. and worldwide shares fairly sometimes commerce durations of prolonged dominance.

Supply: The Onveston Letter (2023) through Alex MacKinnon, Twitter

We is likely to be on the level of such a commerce.

Passive diversification has not labored

For the well-meaning U.S. investor making an attempt to behave virtuously by spreading her bets in a scientific method internationally, the fact is humbling. Throughout any latest time interval, worldwide shares haven’t zigged when the U.S. shares zagged, subsequently, offering no explicit diversification profit. There are not any massive swaths of international markets the place capitalism works higher than the U.S., the place company administration is best, the place earnings are increased or smoother, and the place the foreign money is persistently extra steady than the U.S. greenback due to institutional strengths of the regulatory and judicial our bodies or their prudential Central financial institution insurance policies. It took a few of us just a few a long time to be taught this, however now we all know.

When does passive worldwide investing work?

House Candy House Investing

The disdain for investing in “international” markets – even when the international market in query is the US – is described as “residence bias,” and it’s practically common. House bias in India is sort of 100%, in keeping with Morningstar. An evaluation of fairness holdings in mutual funds from 26 completely different nations exhibits that fairness residence bias is common. All 26 exhibit home bias: Greece, for instance, has the very best share of common mutual fund holdings in its home market (93.5%), as in comparison with its imply world market capitalization weight of 0.46%, a 200:1 chubby. In Austria, the chubby was 75:1; in Mexico, 30:1. Chan, et al, “What determines the home bias and international bias? Proof from mutual fund fairness allocations worldwide. Journal of Finance (2005)

To be honest, there are occasions when passive investing in international shares does work nicely:

- If you get fortunate – For instance, for those who picked India, reasonably than Brazil or China.

- When foreign currency rise in worth in comparison with the U.S. {Dollars}. Often, throughout these durations, commodities are inclined to go up in value as nicely. Overseas fairness indices in U.Ok. and Australia are closely made up of commodity firms. Thus, a lift from each the F.X. and Commodities results in international shares doing nicely.

- After a big crash in threat property, international shares, which typically decline greater than U.S. shares due to their illiquidity, often see a giant rebound when the markets quiet down.

Predicting the longer term (India over China), or the route of F.X. and commodity costs shouldn’t be a requirement for investing. That belongs extra within the class of tactical reasonably than strategic investing. Shopping for shares after a crash is all the time a good suggestion, it doesn’t matter what asset class, however what number of will?

We will maintain making excuses for the U.S. fairness outperformance – progress shares, tech shares, quantitative easing, stimulus, buyback, and so forth. However in some unspecified time in the future, we should face the music. Giant US firms appear to be largely a high quality technique to achieve publicity to worldwide markets. The necessity and rationale for passive investing overseas is the weakest it’s been shortly, and there’s no purpose to see that change. True, valuations overseas are low cost and have been seen so for a protracted interval. We solely perceive the explanations now. These markets by no means deserved a excessive valuation. U.S. shares can come down too, however for this text, we’re discussing Worldwide equities.

Lively Investing over Passive exterior the USA

No worldwide massive cap index fund has received within the long-term

We searched the MFO Premium database for the 20-year returns of all worldwide massive cap funds and ETFs. No diversified passive fund outperformed its peer group common and just one matched the group common. Of 71 qualifying funds, no index fund made the highest 50%. The one exception: MSCI Canada ETF, a non-diversified fund that badly trailed the one actively managed Canada fund, Constancy Canada, on the record

At MFO, we have now the privilege of assembly a lot of Lively Fund managers specializing in worldwide markets. To their credit score, a lot of them have accomplished significantly better than the passive indices they monitor. We did a chunk on Rising Markets Gamers that lined a number of the well-run Lively EM funds from Seafarer, Rondure, Causeway, William Blair, Pzena, and Harding Loevner. Fortified with the information acquired in speaking to many of those managers and studying their letters, my response to the proposed query of “why worldwide markets” was that the case for Worldwide Investing now rests on the shoulders of Lively Administration. It’s higher to adapt and select Lively Managers reasonably than fully exit worldwide investing. There are alternatives all over the place and we have to discover ways to seize them.

Good Lively Investing can also be about what to not purchase

Main Holders of Adani Enterprises

Of the 20 largest holders of Adani Enterprises, the corporate’s flagship entity, 17 are index funds, two are energetic funds for Indian buyers – Kotak Balanced and SBI Balanced, one is a worldwide fund – GS EM Core – not obtainable to US buyers. None of the 20 largest holders is an actively managed US fund or ETF. Per Morningstar.com

Good energetic investing is as a lot about what to not maintain as it’s about what to carry. Take the case of the assorted Adani firms primarily based in India. As of Aug 2022 prospectus, the MSCI India ETF owned Adani Transmission ($61mm), Adani Whole Fuel ($58mm), Adani Inexperienced Power ($43mm), Adani Energy ($17mm), Adani Enterprises ($51mm), and Adani Ports ($25mm). That’s $255mm out of an AUM of $4.1 Billion, or roughly 6.2% of the fund. When the US-based brief vendor, Hindenburg Analysis, put out a damaging thesis on Adani, many of those shares misplaced greater than 50-70% in lower than a month. A few of the Adani shares haven’t even opened for buying and selling because the day after the analysis be aware.

Right here’s the attention-grabbing half – each sensible fund supervisor centered on India had lengthy prevented all Adani shares. One understood Mr. Gautam Adani’s particular place in Indian enterprise due to his long-standing friendship with the present Prime Minister, and subsequently, didn’t brief the businesses. However most Indian fund managers price their salt weren’t lengthy the shares both. The bag holders have been native retail buyers chasing momentum and native and international ETF buyers. MSCI India not too long ago decreased Adani inventory weights by adjusting down its free float, and several other ESG funds decreased their holdings after “additional evaluation” – also called shopping for places after the market has crashed.

How my private portfolio has developed:

My very own portfolio of non-US inventory investments has developed over time. I can attest that I at the moment don’t personal any Worldwide or Rising Passive ETFs. I personal an actively managed Non-public Fairness fund in India, the place I’ve been an investor for over 15 years. I personal a Hedge fund, additionally centered on India. Each these funds are run by associates, making them a lot simpler to  be invested in. I grew up with these folks. In public markets, I personal two actively managed fairness mutual funds run by Seafarer – the Rising Market fund (Andrew Foster) and the Worldwide Worth Fund (Paul Espinosa). I’d tactically buy particular nation or fashion ETFs however could be hard-pressed to strategically and long-term put money into international markets anymore utilizing passive investing.

be invested in. I grew up with these folks. In public markets, I personal two actively managed fairness mutual funds run by Seafarer – the Rising Market fund (Andrew Foster) and the Worldwide Worth Fund (Paul Espinosa). I’d tactically buy particular nation or fashion ETFs however could be hard-pressed to strategically and long-term put money into international markets anymore utilizing passive investing.

In conclusion:

- Worldwide investing shouldn’t be for everybody. Most of us will lose endurance alongside the best way.

- If you will go down the highway of investing in international securities, select Lively over Passive. Passive indices are constructed poorly abroad. What’s labored within the U.S. doesn’t work overseas.

- Correct Lively wants expertise and ability.

- Much more importantly, correct Lively wants <<<TIME>>>

- After we put money into Mutual Funds pursuing Worldwide investing, particularly these with a Worth bent, we have to give them a whole lot of time – virtually as if it was an illiquid personal fairness funding.

- It helps to take a position with managers with vital battle expertise and a major quantity of their very own property within the fund.

[ad_2]