{kind=link}

[ad_1]

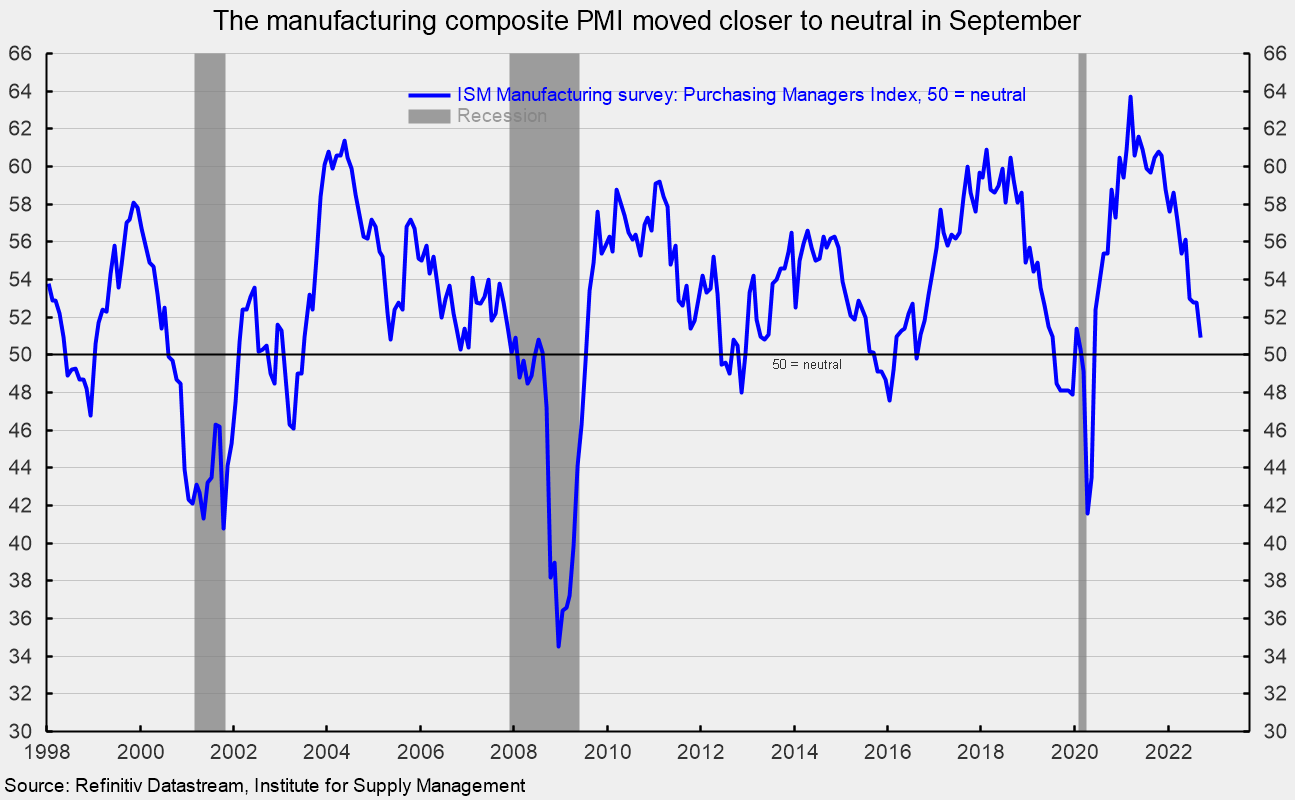

The Institute for Provide Administration’s Manufacturing Buying Managers’ Index fell to 50.9 % in September, barely above the impartial 50 stage. September is the twenty eighth consecutive studying above fifty, however the lowest since Might 2020 (see the primary chart).

A number of key part indexes have been additionally near or under impartial in September, together with the brand new orders index, the manufacturing index, the brand new export orders index, the prices-paid index, and the provider deliveries index. Based on the report, “The U.S. manufacturing sector continues to broaden, however on the lowest price for the reason that pandemic restoration started. Following 4 straight months of panelists’ corporations reporting softening new orders charges, the September index studying displays corporations adjusting to potential future decrease demand.”

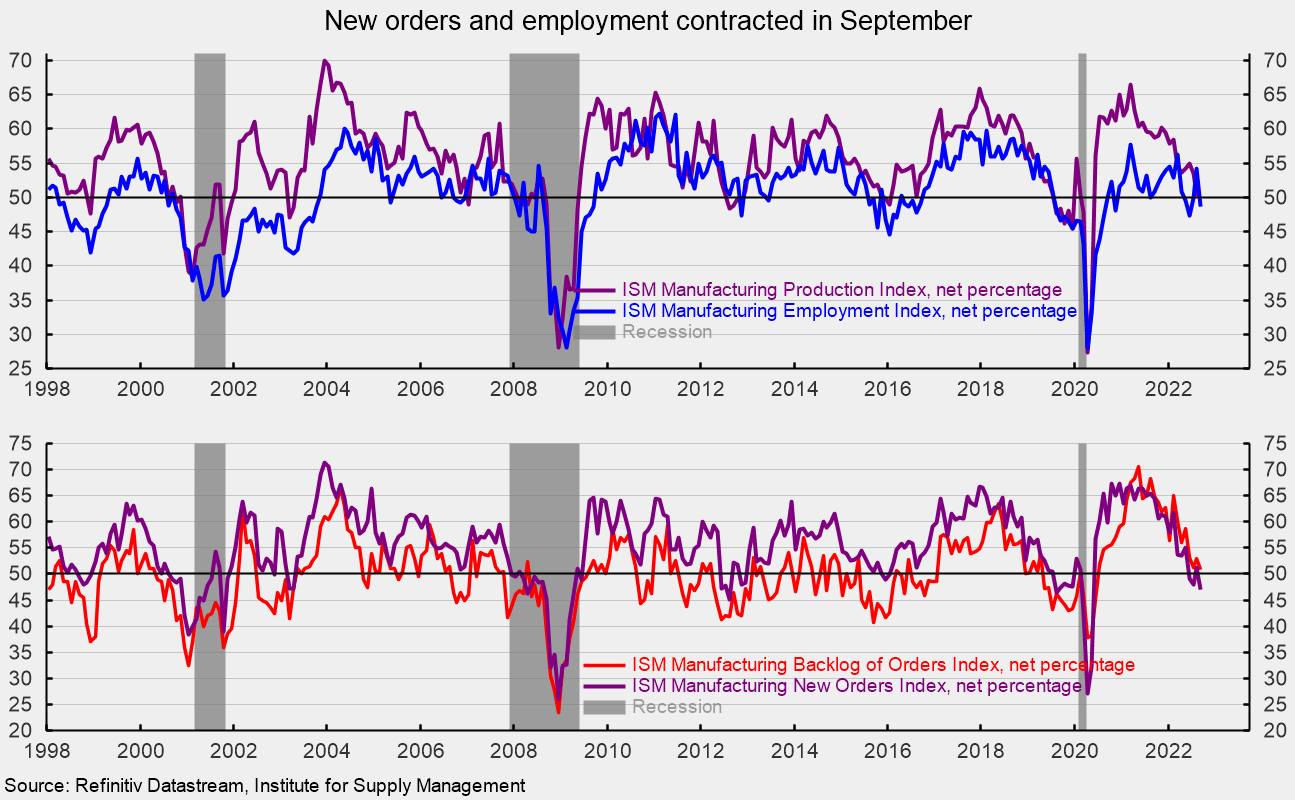

The brand new orders index fell by 4.2 factors to 47.1 % in September, the third studying under impartial within the final 4 months. The consequence suggests orders contracted once more in September (see the underside of the second chart). The brand new export orders index, a separate measure from new orders, remained under impartial at 47.8 % versus 49.4 % in August. The newest studying is the second consecutive month under impartial.

The Backlog-of-Orders Index got here in at 50.9 % versus 53.0 % in August, a 2.1-point fall (see the underside of the second chart). This measure has pulled again from the record-high 70.6 % lead to Might 2021 however has been above 50 for 27 consecutive months. The index suggests producers’ backlogs proceed to rise, however the tempo is sort of weak.

The Manufacturing Index registered a 50.6 % lead to September, gaining 0.2 factors from August (see the highest of the second chart). The index has been above 50 for 28 months however stays very near impartial.

The Employment Index fell sharply in September, falling again under the impartial threshold. The 48.7 % studying suggests payrolls contracted within the manufacturing sector in September (see the highest of the second chart). The report states, “Labor administration sentiment shifted in September, with a better variety of panelists’ corporations pausing hiring via hiring freezes and permitting attrition to cut back employment ranges. Turnover charges eased, with 28 % of feedback citing backfill and retirement points, a lower from 33 % in August.” Among the many six massive sectors within the survey, solely two reported expanded payrolls in September.

The Bureau of Labor Statistics’ Employment State of affairs report for September is due on Friday, October 7, and expectations are for a acquire of 250,000 nonfarm payroll jobs, together with the addition of 20,000 jobs in manufacturing. Buyer inventories in September are nonetheless thought-about too low, with the index coming in at 41.6 %, up 2.7 factors from August (index outcomes under 50 point out clients’ inventories are too low). The index has been under 50 for 72 consecutive months. Inadequate stock is a optimistic signal for future manufacturing.

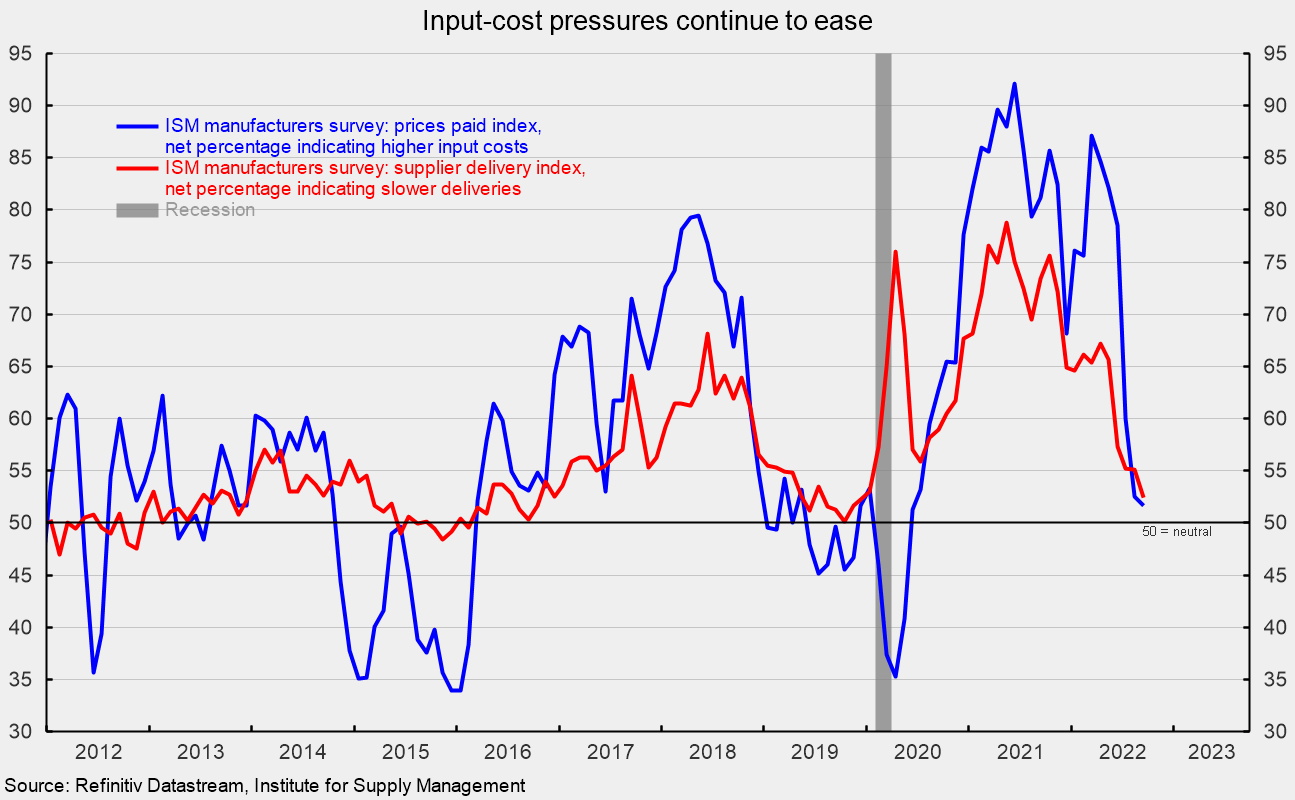

The provider deliveries index registered a 52.4 % lead to September, down 2.7 factors from August and the bottom studying since December 2019. The index was at 78.8 % in Might 2021. The easing development over the previous 16 months recommend supply lead occasions are slowing at a a lot slower price (see third chart).

The index for costs for enter supplies sank once more, dropping one other 0.8 factors to 51.7 in September and is the sixth consecutive month-to-month decline (see third chart). The index is down from 87.1 % in March 2022 and is on the lowest stage since June 2020. The consequence suggests value pressures have eased considerably. The report notes, “That is the second consecutive month the Costs Index registered under 60 %, a stage not seen since August 2020 (59.5 %), and that is additionally the bottom studying since June 2020 (51.3 %). Over the previous six months, the index has decreased 35.4 proportion factors, together with a mixed 26-percentage level plunge in July and August.” The report provides, “The slowing in value will increase is being pushed by continued (1) rest within the power markets, (2) softening within the copper, metal, aluminum and corrugate markets and (3) persevering with sluggishness in chemical and plastics demand. Notably, 28.1 % of respondents reported paying decrease costs in September, in comparison with 26.7 % in August.”

The manufacturing sector is exhibiting clear indicators of weak spot although not collapse. Financial dangers stay elevated because of the affect of inflation, an aggressive Fed tightening cycle, and continued fallout from the Russian invasion of Ukraine. The outlook stays extremely unsure. Warning is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following greater than 25 years in financial and monetary markets analysis on Wall Avenue. Bob was previously the top of World Fairness Technique for Brown Brothers Harriman, the place he developed fairness funding technique combining top-down macro evaluation with bottom-up fundamentals.

Previous to BBH, Bob was a Senior Fairness Strategist for State Avenue World Markets, Senior Financial Strategist with Prudential Fairness Group and Senior Economist and Monetary Markets Analyst for Citicorp Funding Companies. Bob has a MA in economics from Fordham College and a BS in enterprise from Lehigh College.

[ad_2]