{kind=link}

[ad_1]

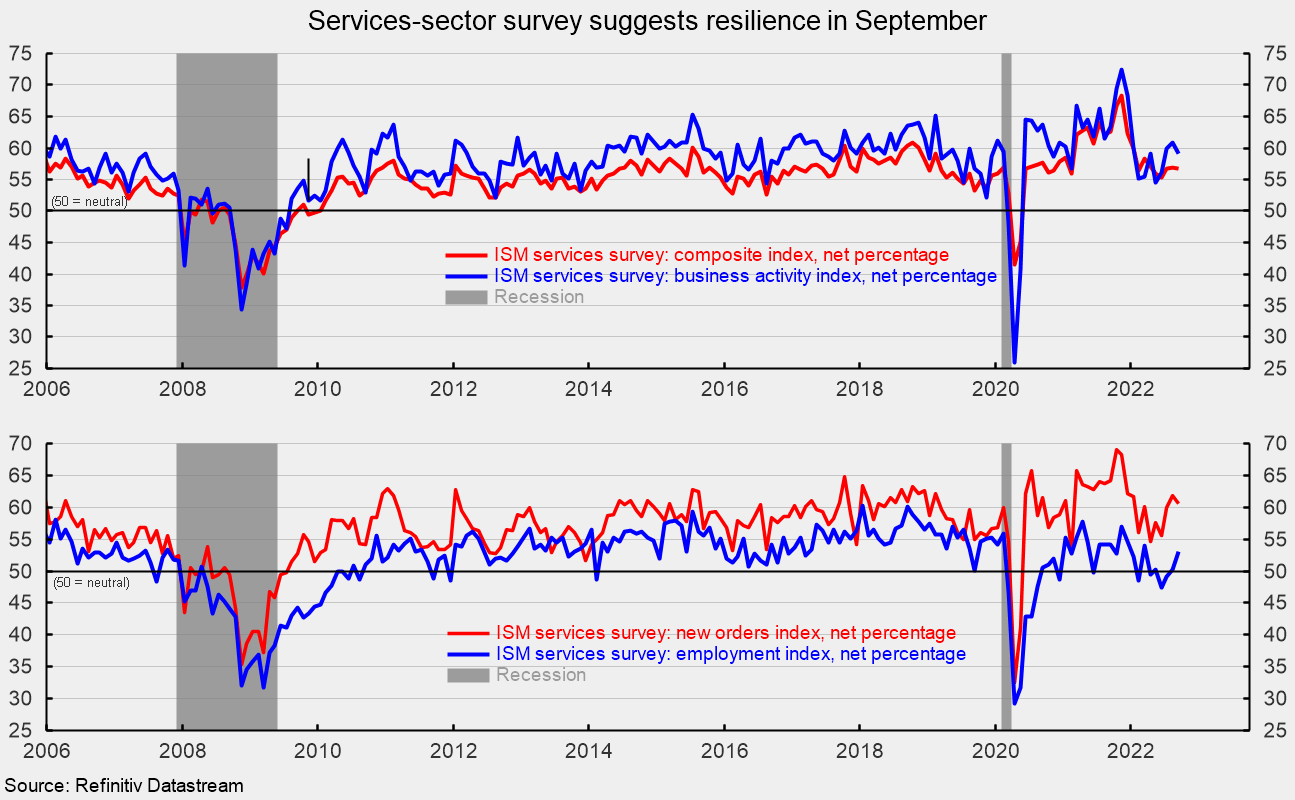

The Institute for Provide Administration’s composite companies index decreased to 56.7 % in September, falling 0.2 factors from 56.9 % within the prior month. The index stays above the impartial 50 threshold and suggests the twenty eighth consecutive month of enlargement for the companies sector (see high of first chart). The September outcomes are very near the common outcomes for the six years ending December 2019 earlier than the lockdown recession. For the composite index, the common over that interval is 56.6 %.

Among the many key elements of the companies composite index, the enterprise exercise index fell 1.8 factors to 59.1 (see high of first chart). That’s the twenty eighth month above 50, and 0.7 share factors beneath the six-year common of 59.7 %. Fourteen industries reported elevated exercise whereas two reported slower exercise.

The companies employment index improved in September, coming in at 53.0 %, up from 50.2 % in August. That’s simply the fourth time within the final eight months that the employment index was above impartial, with a median of fifty.2 % over that interval (see backside of first chart). The September consequence can be beneath the six-year common (2014-2019) of 55.1 %.

Ten industries reported employment development, whereas two reported a discount. Respondents counsel certified labor continues to be in brief provide, however a number of famous considerably simpler labor circumstances.

The companies new-orders index fell to 60.6 % from 61.8 % in August, reducing by 1.2 share factors (see backside of first chart). The brand new orders index has been above 50 % for 28 consecutive months and is 1.7 factors above the six-year common of 58.9 %.

The nonmanufacturing new-export-orders index, a separate index that measures solely orders for export, improved in September, coming in at 65.1 versus 61.9 % in August. Six industries reported development in export orders, with three reporting declines and 9 reporting no change. Nevertheless, for all respondents, solely about 23 % stated they carry out and monitor separate exercise outdoors the US.

Backlogs of orders within the companies sector possible grew once more in September although the tempo possible decelerated because the index decreased to 52.5 % from 53.9 %. September was the 21st month in a row with rising backlogs. Ten industries reported increased backlogs in September, whereas 4 reported decreases.

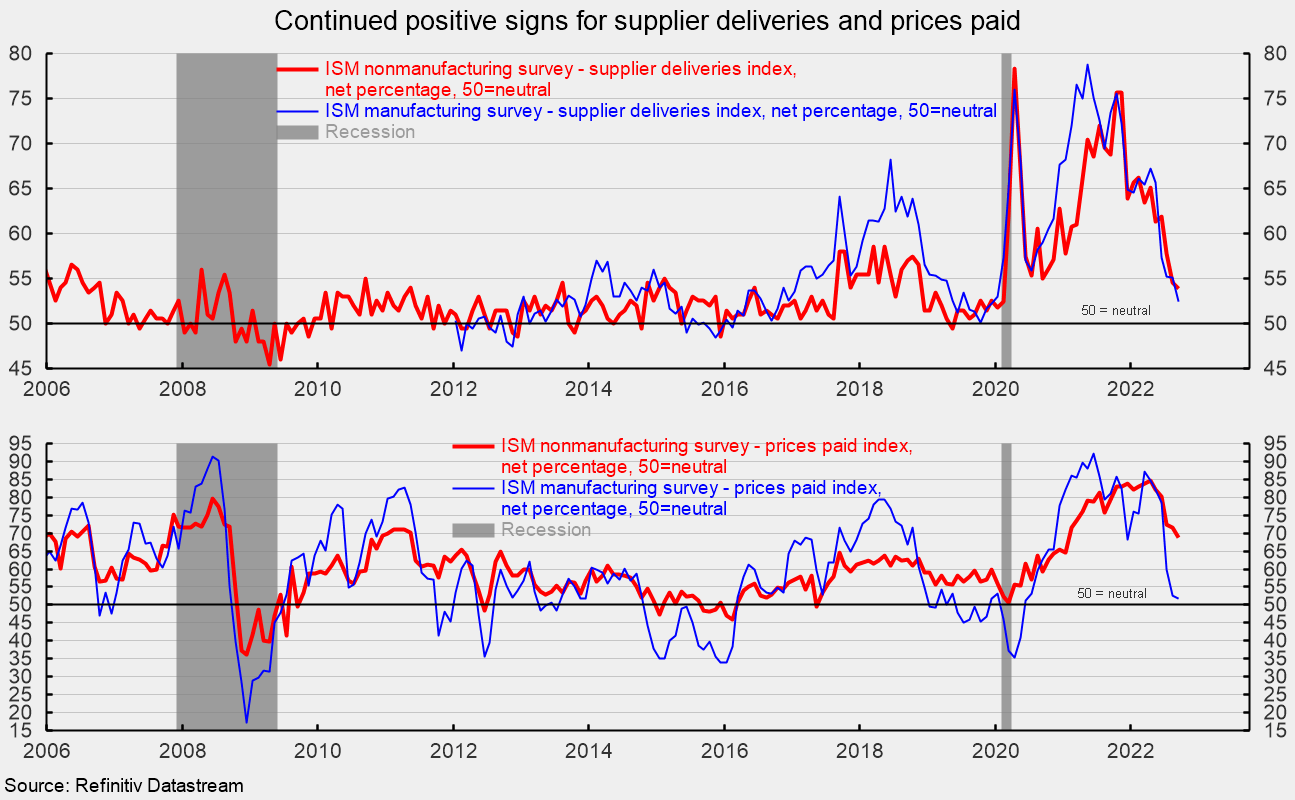

Provider deliveries, a measure of supply instances for suppliers to nonmanufacturers, got here in at 53.9 %, down from 54.5 % within the prior month (see high of second chart). It suggests suppliers are falling additional behind in delivering provides to companies enterprise, however the slippage has decelerated from the prior month. The index has moved sharply decrease since back-to-back readings above 75 in October and November 2021, and is on the lowest stage since February 2020, simply earlier than the lockdown recession. The manufacturing sector survey matches the latest enchancment (see high of second chart). For the companies sector, ten industries reported slower deliveries in September whereas six reported sooner deliveries.

The nonmanufacturing costs paid index fell to 68.7 % in September, the fifth consecutive decline from a record-high 84.6 % in April (see backside of second chart). Eighteen industries reported paying increased costs for inputs in September. Value pressures have eased considerably for the companies sector whereas the manufacturing sector has seen a big decline in worth pressures (see backside of second chart).

The most recent Institute of Provide Administration report means that the companies sector and the broader financial system expanded for the twenty eighth consecutive month in September. Respondents to the survey proceed to spotlight ongoing enter worth pressures, in addition to supplies and labor shortages although a number of the respondents famous some indicators of enchancment. Respondents additionally reported indicators of easing demand and concern concerning the financial outlook.

Robert Hughes

Robert Hughes joined AIER in 2013 following greater than 25 years in financial and monetary markets analysis on Wall Avenue. Bob was previously the top of World Fairness Technique for Brown Brothers Harriman, the place he developed fairness funding technique combining top-down macro evaluation with bottom-up fundamentals.

Previous to BBH, Bob was a Senior Fairness Strategist for State Avenue World Markets, Senior Financial Strategist with Prudential Fairness Group and Senior Economist and Monetary Markets Analyst for Citicorp Funding Companies. Bob has a MA in economics from Fordham College and a BS in enterprise from Lehigh College.

[ad_2]