{kind=link}

[ad_1]

“We live by funding regime change”

Goal and technique

Seafarer Abroad Worth pursues long-term capital appreciation. The fund sometimes invests in widespread shares, although the managers have the power so as to add each most well-liked shares and fixed-income securities. The investable universe contains each rising markets, as historically conceived, and firms domiciled in chosen overseas developed nations (together with Australia, Hong Kong, Eire, Israel, Japan, New Zealand, Singapore, and the UK) when these corporations have “vital financial and monetary linkages to creating nations.”

The portfolio is constructed by bottom-up safety choice based mostly on elementary analysis. The managers are in search of “securities priced at a reduction to their intrinsic worth.”

Adviser

Seafarer Capital Companions is an funding adviser centered on rising markets. Based in 2011, Seafarer is an entirely employee-owned agency positioned within the San Francisco Bay. Each of their methods purpose to offer long-term funding portfolios that supply sustainable development, affordable earnings, appropriate diversification, and volatility mitigation. The agency’s aim is to construct lasting wealth for purchasers over time. Seafarer makes a speciality of co-mingled, long-only rising markets funds. The agency serves because the funding adviser to the Seafarer Abroad Progress and Earnings Fund and the Seafarer Abroad Worth Fund. Morningstar estimates that the agency has a bit over $2 billion in AUM with 1 / 4 billion in inflows over the previous 12 months (from 3/20/23).

Managers

Paul Espinosa, Brent Clayton, and Andrew Foster.

Paul Espinosa, Brent Clayton, and Andrew Foster.

Mr. Espinosa is the Lead Portfolio Supervisor of the fund and has been so since its inception, which suggests he has major duty for the day-to-day administration of the fund’s portfolio. Earlier than becoming a member of Seafarer in 2014, Mr. Espinosa was an fairness analysis analyst at Legg Mason, the place he centered on world rising markets. That was preceded by stints at Citigroup Asset Administration and J.P. Morgan.

Mr. Clayton grew to become co-manager in February 2023 although he has been with Seafarer since 2018. Earlier than that, he was Co-Portfolio Supervisor, Head of Elementary Analysis, and Fairness Analyst at LR International Companions, an funding agency centered on value-based investing in frontier and rising markets.

Mr. Foster is considered one of Seafarer’s founders, its CIO, and a Lead Portfolio Supervisor of the Seafarer Abroad Progress and Earnings Fund. Earlier than founding Seafarer Capital Companions in 2011, Mr. Foster was a Lead Portfolio Supervisor, Appearing Chief Funding Officer, Director of Analysis at Matthews Worldwide Capital Administration, and adviser to the Matthews Asia funds.

The Seafarer workforce is admirably and solely centered on their funds. Whereas managers at many different advisers break up their time between a half dozen funds, a few hedge funds, and a bunch of separate accounts, the Seafarer Funds managers centered on … nicely, the Seafarer Funds.

| Different funds managed | Different pooled automobiles managed | Different accounts managed | |

| Andrew Foster | 0 | 0 | 0 |

| Paul Espinosa | 0 | 0 | 0 |

| Lydia So | 0 | 0 | 0 |

| Kate Jaquet | 0 | 0 | 0 |

Supply: Assertion of Extra Info (2022)

Technique capability and closure

Seafarer has each a dedication to and custom of closing their funds when it’s of their present shareholders’ finest curiosity to take action. We don’t have a proper calculation of the technique’s capability, however the mixture of a concentrated portfolio (round 40 names) and substantial small cap publicity (at the moment 10 shares with market caps under $1 billion) implies a cap within the decrease billions.

Administration’s stake within the fund

Ms. Espinosa has invested between $100,000 and $500,000 in his fund. Co-manager Andrew Foster has invested over $1 million, and Mr. Clayton, who just lately moved from analyst to co-manager, has invested between $10,000 – $50,000 within the fund.

A observe on vigilance: having pores and skin within the sport usually leads managers to be relatively extra danger acutely aware than others. (Ma & Tang, “Portfolio supervisor possession and mutual fund danger taking,” 2018) Having your boss’s pores and skin within the sport ramps that up by an quantity surpassed solely by having your in-laws’ pores and skin within the sport.

Opening date

Might 31, 2016

Minimal funding

The minimal for Investor shares is $2,500, and for Institutional shares, $25,000. The Investor minimal is diminished for each retirement accounts and accounts arrange with an automated investing plan.

Expense ratio

The Investor shares carry a internet e.r., after waivers, of 1.15% on belongings of $72.8 million {dollars}. Institutional shares cost 1.05%, internet.

Shut your eyes and picture seeing “an rising markets metropolis.” What do you see? The crowded streets of Mumbai? An open-air spice market in Istanbul? A shining sea of skyscrapers ringed by tin-roofed huts?

Do the identical train with skilled buyers and, as an alternative of cityscapes, there’s a tumult of ideas: obscure and unreliable accounting, opaque company constructions, arcane market guidelines, wild forex fluctuation, infinite authorities meddling … an unmanageable swamp.

Do the identical train with skilled buyers and, as an alternative of cityscapes, there’s a tumult of ideas: obscure and unreliable accounting, opaque company constructions, arcane market guidelines, wild forex fluctuation, infinite authorities meddling … an unmanageable swamp.

Conclude the train with Paul Espinosa, and a wholly totally different image seems:

He sees a number of the finest administration groups on the planet whose members have graduated from a number of the world’s finest universities and who’ve been examined in some extremely difficult markets. These groups, he suggests, “by advantage of their cosmopolitan domicile, are inclined to have a mix of home and worldwide administration, and on the danger of overgeneralizing, a level of professionalism that one doesn’t all the time discover elsewhere.”

He sees a number of the best-run, best companies that are steadily incomes market share within the US and Europe by out-competing their home rivals. Samsung could be one instance, and China’s WH Group, proprietor of Smithfield within the US, could be one other, however Mr. Espinosa thinks the clearest is Ambev.

Ambev was shaped in 1998 by the merger of two Brazilian brewers: Brahma and Atarctica. The administration workforce that oversaw that company marriage was the one which developed the now well-known “zero-budgeting” course of employed by 3G Capital and Warren Buffet to handle the Kraft-Heinz merger. The serial acquisitions to construct the Ambev empire within the Americas culminated with the merger with Interbrew (Belgium-based) and subsequent merger with Anheuser Busch (US-based). The dominant shareholders of Anheuser-Busch InBev are the unique Brazilian and Belgian households. The highest administration of ABI has additionally been Brazilian. At its coronary heart, ABI is the manifestation of a Brazilian takeover of the worldwide brewing trade.

He sees constant mispricing pushed by the placement of company workplaces since most of the largest mutual funds are constrained from touching “the rising markets.”

He sees constant mispricing pushed by the dimensions of the firms since enormous and passive funds are constrained by liquidity screens from taking a look at smaller companies; in consequence, 201 of 224 rising markets funds fall solidly in Morningstar’s “giant cap” field.

He sees constant mispricing pushed by the truth that many rock-solid investments don’t bear the normal markers of “development shares,” the popular model of most EM buyers. Solely 50 of the 224 rising markets funds fall into the “worth” realm.

He sees Anheuser Busch, “a world brewer that derives most of its income from rising markets,” and the road of Brussels.

He sees issues investing in nations the place politicians, relatively than managers and boards, management the selections that companies make (Mr. Foster was as soon as informed that any vital layoffs at Sberbank must be reviewed by Mr. Putin himself), and so his publicity to China and Russia has been one-third of his friends. Morningstar celebrated Seafarer’s flagship as one of many few EM funds to overlook the Russian collapse (Katharine Lynch, “Simply 8% of Rising-Markets Funds Miss Russian Collapse,” 3/9/2022).

And he sees these variations clearly sufficient that Abroad Worth has an energetic share of 98. It was the best-performing diversified rising markets fund of 2022, posting a lack of -0.7% in opposition to a peer common of -20.8%, and has earned each MFO’s Nice Owl designation and Morningstar’s backward-looking 5-Star and forward-looking Silver recognitions.

MFO doesn’t endorse utilizing quick time period returns as a approach to make funding selections; that’s nothing however a recipe for heartache. Seafarer has a 6.8-year observe document. Over the previous five- and six-year durations, it has been a top-five diversified EM fund based mostly on each whole returns and risk-adjusted returns (mirrored in its Sharpe ratio, in addition to the extra risk-sensitive Sortino and Martin ratios and Ulcer Index). Morningstar locations its whole returns over 5 years within the prime 3% of its peer group (as of three/28/2023).

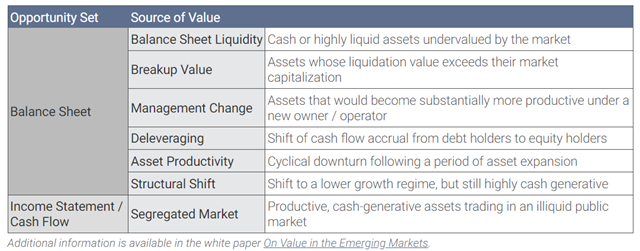

The method: In broad phrases, Mr. Espinosa works inside a universe of roughly 450 EM worth shares whose internet worth is one thing like $1.5 trillion. His self-discipline is constructed round figuring out essentially the most compelling investments by assessing every company in opposition to a rubric that identifies seven potential sources of worth.

He invests, usually for the long-term, within the 40 most compelling alternatives. Turnover tends to be within the teenagers, and he reviews that the final time he eliminated a reputation from the portfolio was within the third quarter of 2021.

Mr. Espinosa sees an epochal change in funding actuality coming. The story for the previous three a long time has been the identical: purchase the US, purchase giant caps, purchase development, purchase funding grade debt, purchase indexes and also you’re certain to win. His tone is much less derisive than sorrowful:

The price of preconceptions grew to become obvious in 2022. In the USA, fastened earnings devices generated returns as adverse as these of fairness securities. The returns of rising market fairness indexes have been corresponding to these of the S&P 500 in a down 12 months. The standard security of the fastened earnings asset class was conspicuous by its absence, as was the beta traditionally related to rising market equities.

Whereas buyers may have anticipated each the chance related to potential bond returns when rates of interest are pegged to the ground and the diminished danger related to the decrease valuations of rising markets in contrast with U.S. equities, what number of acted on stated funding circumstances? Arguably, a significant set of buyers recognized these insights final 12 months, however few invested with anticipation, in any other case market returns wouldn’t have confirmed as expensive.

It’s certainly troublesome for an investor to beat the preconception {that a} balanced portfolio is safer than an equity-only one, or that rising market fairness indexes are extra unstable than a U.S. market index.

One other preconception the longer term could problem is the view that rising market (EM) corporates are riskier than developed market ones, a minimum of on a selective foundation. Seafarer’s work over time has revealed a rising checklist of EM corporations which can be managed simply in addition to main world corporates and have expanded internationally, together with into developed markets, mirroring the conduct of multinational companies that increase into rising markets. Furthermore, many of those EM corporations’ administration groups are battle examined in navigating excessive inflation, unstable overseas trade charges, and erratic financial development – challenges that developed market administration groups have confronted much less acutely, and few Chinese language administration groups have confronted in any respect. I might argue that these choose EM corporates redefine danger in a approach which will transcend the normal definition of danger when it comes to nations. The standard definition of danger could show a handicap to producing funding returns in choose EM corporates in the identical approach that preconceptions proved a handicap to buyers in 2022.

We live by an funding regime change, and I discover the foregoing redefinition of danger a cause to be optimistic in regards to the prospect for future funding returns even in a slower-growth world. That’s, so long as the investor is selective and unencumbered by preconceptions.

Seafarer has an extended historical past of dogged independence, of managing to protect their buyers’ wealth, and of manufacturing affordable returns in unreasonable markets. Seafarer Abroad Worth Fund has embodied these household traits and has served its buyers exceptionally nicely, even in markets that didn’t favor their model. Because the world begins to grapple with the realities that Seafarer has already mastered, their prospects appear exceptionally vibrant. It absolutely deserves a spot on any fairness investor’s due-diligence checklist.

The Seafarer Funds website is extremely wealthy. It presents a wealth of historic fund composition and efficiency knowledge that’s largely unmatched for the investor. Seafarer Abroad Worth Fund’s homepage is clear and readable. You may be taught rather a lot there. I significantly like Paul’s behavior of flagging the potential sources of worth for every reported holding. An instance from their January 2023 portfolio evaluate illustrates the notion:

The Fund’s appreciation this quarter seems to narrate to the mix of low valuations and bettering revenue prospects of the Fund’s holdings. China’s rest of its zero-Covid insurance policies contributed to vital appreciation of a number of China-related holdings. Particularly, the share value of Melco Worldwide (Asset Productiveness and Breakup Worth supply of worth; the “supply of worth” for a Fund holding is hereafter referenced in parentheses), a on line casino proprietor and operator in Macau, rose 38.69% in U.S. greenback phrases through the fourth quarter, on the expectation that the comfort of journey restrictions in China would improve the variety of guests to Macau, which had fallen to an all-time low. The share costs of Shangri-La (Breakup Worth and Asset Productiveness), a resort proprietor and operator, and DFI Retail (Administration Change and Asset Productiveness), a multi-format retailer working in Asia, rose for a similar cause.

[ad_2]