{kind=link}

[ad_1]

What number of instances have you ever approached the Union Price range with immense expectations and are available again empty handed? The motion lay elsewhere. There have been necessary bulletins however in a roundabout way associated to placing more cash in your pockets.

Not this time.

The Union Price range 2023 was action-packed. So many bulletins that immediately influence the middle-class taxpayer. I listing a number of the finances proposals immediately impacting the taxpayers.

- Decrease tax charges beneath the brand new tax regime.

- Conventional plans with annual premiums over Rs 5 lacs introduced beneath the tax web.

- Taxpayers set off long run capital beneficial properties by buying a residential property. Set-off limits beneath Part 54 and Part 54F are actually capped.

- Enhance in funding cap beneath Senior Residents financial savings scheme (SCSS) from Rs 15 lacs to Rs 30 lacs.

- Enhance in Tax assortment at Supply (TCS) for remittance beneath LRS for journey and investments overseas.

- Adversarial tax modifications for REITs and Market-linked debentures

All the above modifications are usually not beneficial however the unfavourable ones principally have an effect on the HNIs.

Not doable to cowl this wide selection of matters in a single publish. Therefore, will cowl a few of these over the following few weeks. On this publish, I give attention to crucial one, the modifications to the tax construction within the new tax regime.

Now that the brand new tax regime has been made extra engaging, does it make sense so that you can change from the previous tax regime to the brand new regime?

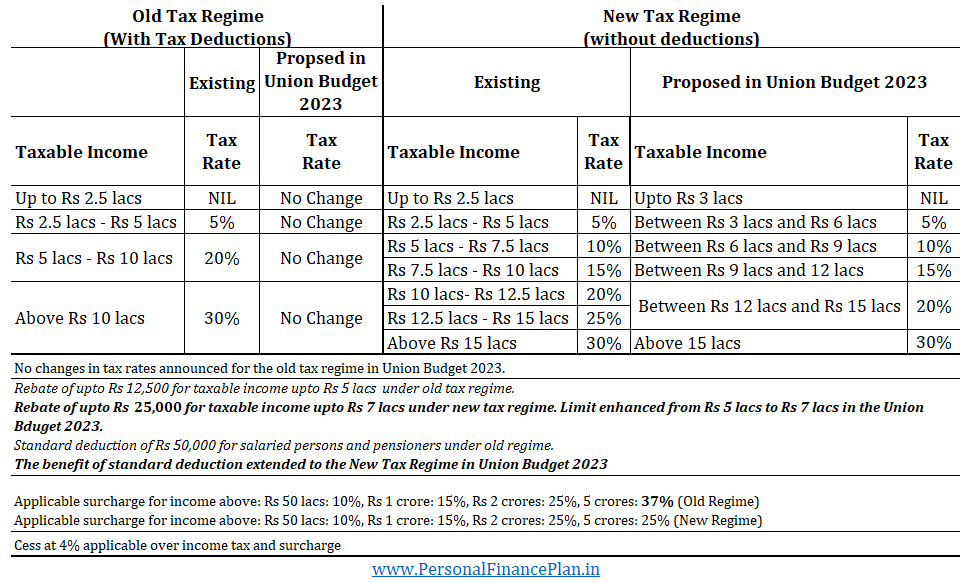

What are the brand new tax slabs?

The tax charges haven’t been modified beneath the previous tax regime (Greater tax price however deductions).

The modifications are just for the brand new tax regime (decrease tax charges with out deductions).

Incentives for the New Tax Regime

- Enhancement of minimal exemption restrict from Rs 2.5 lacs to Rs 3 lacs

- The eligibility of rebate beneath Part 87A enhanced from Rs 5 lacs to Rs 7 lacs if choosing the brand new tax regime. This ensures no taxes in case your earnings doesn’t exceed Rs 7 lacs.

- Decrease tax charges

- Normal deduction of Rs 50,000 is now allowed for Salaried individuals and pensioners. Was not permitted earlier.

- Surcharge for earnings over Rs 5 crores decreased from 37% to 25%, if choosing the brand new tax regime.

- New tax regime shall be the default possibility.

No taxes if the earnings is as much as Rs 7 lacs

In the event you go for the brand new tax regime and in case your earnings is as much as Rs 7 lacs, you do not need to pay any tax.

How does this occur?

By a provision beneath Part 87A.

Beneath Part 87A, you’re eligible for a rebate of as much as Rs 25,000 (earlier Rs 12,500) if the whole earnings doesn’t exceed Rs 7 lacs (earlier Rs 5 lacs). This transformation is just for the New tax regime.

So, let’s say your earnings is Rs 6.5 lacs. As per the revised tax slabs/charges, your tax legal responsibility shall be Rs 20,000. Nevertheless, because the earnings is under Rs 7 lacs, you’ll be eligible for a rebate of Rs 20,000. Decrease of (Rs 20000, 25000). Therefore, zero tax legal responsibility.

If you’re a salaried worker or a pensioner, you may as well take commonplace deduction. This can push the tax-free restrict to Rs 7.5 lacs.

Word: The foundations haven’t been modified for the previous tax regime. Beneath the previous tax regime, the rebate continues to be capped at Rs 12,500 if the earnings doesn’t exceed Rs 5 lacs.

For dedication of complete taxable earnings, it isn’t simply your wage that’s counted. The capital beneficial properties or curiosity earnings or another taxable earnings should even be added to calculate the whole earnings. Even the LTCG on fairness/fairness funds of as much as Rs 1 lac have to be added since it isn’t exempt earnings however taxable earnings on which no tax have to be paid.

Aid for Excessive Revenue Earners

In the event you earn very well, the Authorities asks you to pay extra taxes. The tax slabs don’t change however the surcharge kicks in.

Above 50 lacs: 10%

Above Rs 1 crores: 20%

Above Rs 2 crores: 25%

Above Rs 5 crores: 37%

Thus, in case your taxable earnings is greater than Rs 5 crores, your tax price in your whole earnings above Rs 10 lacs is 30% * (1+37% surcharge) * (1 + 4% cess) = 42.77%

The Authorities proposes a change right here.

For earnings above Rs 5 crores, the surcharge shall be decreased from 37% to 25%, however provided that you go for the brand new regime. This reduces marginal tax price = 30% * (1+25% surcharge) * (1+4% cess) = 39%

No change in surcharge price for the previous tax regime. And the speed of surcharge stays 37% if the whole earnings is greater than 5 crores.

Clearly, for such taxpayers with annual earnings above Rs 5 crores, new tax regime is a simple alternative regardless of the tax deductions taken.

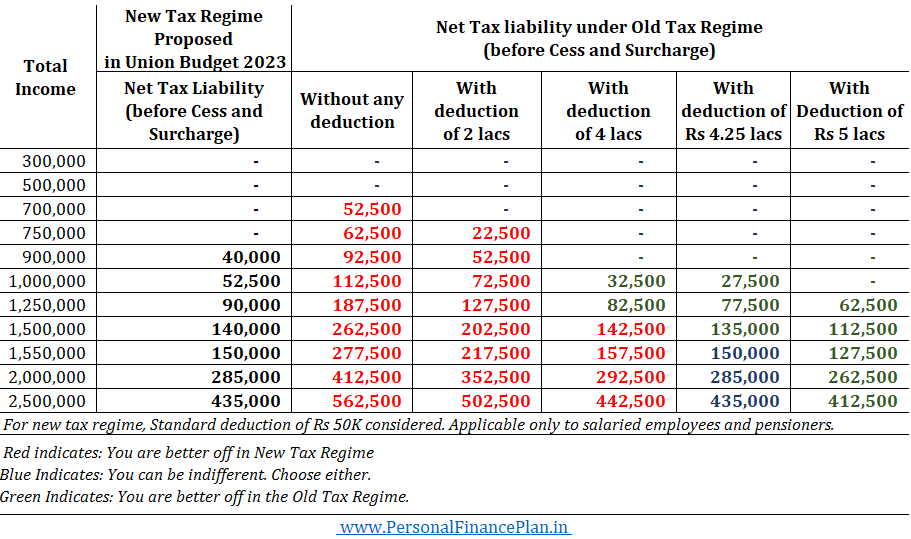

How higher is the Proposed New Tax Regime in comparison with the Current New Regime?

The next illustration demonstrates the influence for salaried taxpayers.

Since the advantage of commonplace deduction is accessible solely to salaried workers and pensioners, the distinction will cut back for professionals.

What must you decide: New Tax Regime or the Previous Tax Regime?

Now to the true query.

Between the previous and the brand new tax regime, which one must you decide?

The brand new Tax regime has decrease tax charges however doesn’t permit deductions.

Previous tax regime has greater taxes however permits to scale back earnings by tax deductions.

Due to this fact, if you happen to can avail sufficient tax deductions, you would possibly nonetheless be higher off within the previous regime.

However what’s the tipping level? What’s “sufficient”?

What ought to be the quantity of tax deductions to make the previous regime extra engaging?

I in contrast the tax liabilities for varied ranges of earnings and tax deductions for salaried workers (who will get the advantage of commonplace deduction beneath each previous and new regime).

As you may see above, the brink of tax deduction the place previous regime turns into extra engaging than the brand new regime is Rs 4.25 lacs (together with commonplace deduction).

Due to this fact, if you happen to can handle tax deduction of Rs 4.25 or extra (Rs 3.75 lacs excluding commonplace deduction), you’ll be higher off within the previous regime.

For non-salaried (who don’t get profit of ordinary deduction), the tipping level shall be Rs 3.75 lacs.

Now, it’s essential to see if you happen to can take tax deductions to that extent.

Part 80C: As much as Rs 1.5 lacs (life insurance coverage premium, ELSS, PPF, EPF, and many others.)

Part 80D: As much as Rs 25,000. For medical insurance premium. In the event you (or your partner) are a senior citizen, the profit goes as much as Rs 50,000. As well as, if you’re paying the premium in your dad and mom, you get a further 25,000 tax profit. If both mother or father is a senior citizen, the extra profit goes to 50,000.

Part 80CCD(1B): As much as 50,000 for personal contribution to NPS.

Normal deduction of Rs 50,000.

These numbers add as much as about 2.75 lacs.

The opposite distinguished ones are as much as Rs 2 lacs for Dwelling Mortgage Curiosity (Part 24) and home lease allowance (HRA) adjustment . In case you have taken an training mortgage, you get tax profit for curiosity cost on training mortgage (no cap on the tax profit) beneath Part 80E.

So, if you’re staying in a home you personal (self-occupied) and you’ve got repaid the house mortgage in full, you may’t take profit beneath Part 24 (residence mortgage curiosity) and home lease (HRA).

In such a case, it’s tough to the touch that magical mark of Rs 4.25 lacs (for salaried/pensioners) and Rs 3.75 lacs (for self-employed).

And if you happen to can’t hit the mark, you’re higher off within the new tax regime.

Tax Advantages which are nonetheless permitted beneath the New Tax Regime

Normal deduction of Rs 50,000. Allowed just for salaried workers and pensioners.

Employer contribution to NPS, EPF, and superannuation fund. Part 80CCD (2). Word solely employer contributions are allowed as deduction. Not personal contribution. Therefore, when you have been investing in NPS and taking advantage of as much as 50K beneath Part 80CCD(1B), you gained’t have the ability to get that profit if you happen to change to the brand new tax regime.

The Verdict

It’s evident that the Authorities is making an attempt to extend acceptance of the New Tax regime by incentives.

By decreasing tax charges for the middle-income earners.

And decreasing surcharge for very high-income earners.

And probably step by step section out the previous regime. Or if only a few individuals go for the previous regime, it would mechanically turn out to be irrelevant.

And I believe the Authorities is doing it the precise manner. Quite than abolishing the previous regime or withdrawing tax advantages beneath the previous regime, they’ve simply made the New Tax Regime extra engaging.

The Authorities did the identical with crypto investments. It may have banned crypto investments. As an alternative, it discouraged the funding in cryptos by greater taxes, TCS, disallowing setoffs, or carry ahead of loss. So, not an outright ban however a nudge to not make investments.

Going ahead, if the Authorities desires to place more cash within the pockets of the traders, it would merely tweak the tax charges or tax slabs beneath the brand new regime. And never contact the previous tax regime.

With this, it’s honest to NOT count on an enhancement within the Part 80C restrict. Not now and never sooner or later. Or another particular tax advantages. I don’t count on any recent tax profit solely for the previous tax regime sooner or later. If a brand new tax profit (deduction) is introduced, it might be for each the previous and the brand new regime.

By the way in which, if we hold including tax deductions to the brand new regime, we are going to beat the final word goal of the New Tax Regime. An easier tax construction. And the brand new regime turns into the New “Previous Regime”.

The brand new tax regime is easy.

Will get you out of that tax-saving mindset.

Complete industries have mushroomed across the idea of tax-saving. Taxpayers purchase insipid funding merchandise simply to avoid wasting taxes. Beneath stress to make that tax-saving funding earlier than the top of March, they purchase something with little regard to their wants and utility of their portfolios. Gross sales brokers construct their whole gross sales pitch round tax-saving. Not anymore.

I don’t deny that taxation is a vital choice variable when choosing an funding, however it shouldn’t be the one choice variable.

And sure, it’s effective to get out of the tax-saving mindset. Nevertheless, don’t let go of the investment-making mindset. You will need to nonetheless make investments in your monetary targets.

Featured Picture Credit score: Unsplash

[ad_2]