{kind=link}

[ad_1]

Rather less than one yr in the past I requested Are U.S. Housing Costs Changing into Unaffordable?

On the time, the Case Shiller Nationwide Dwelling Value Index had simply hit a brand new all-time excessive for year-over-year worth positive factors of round 20%.

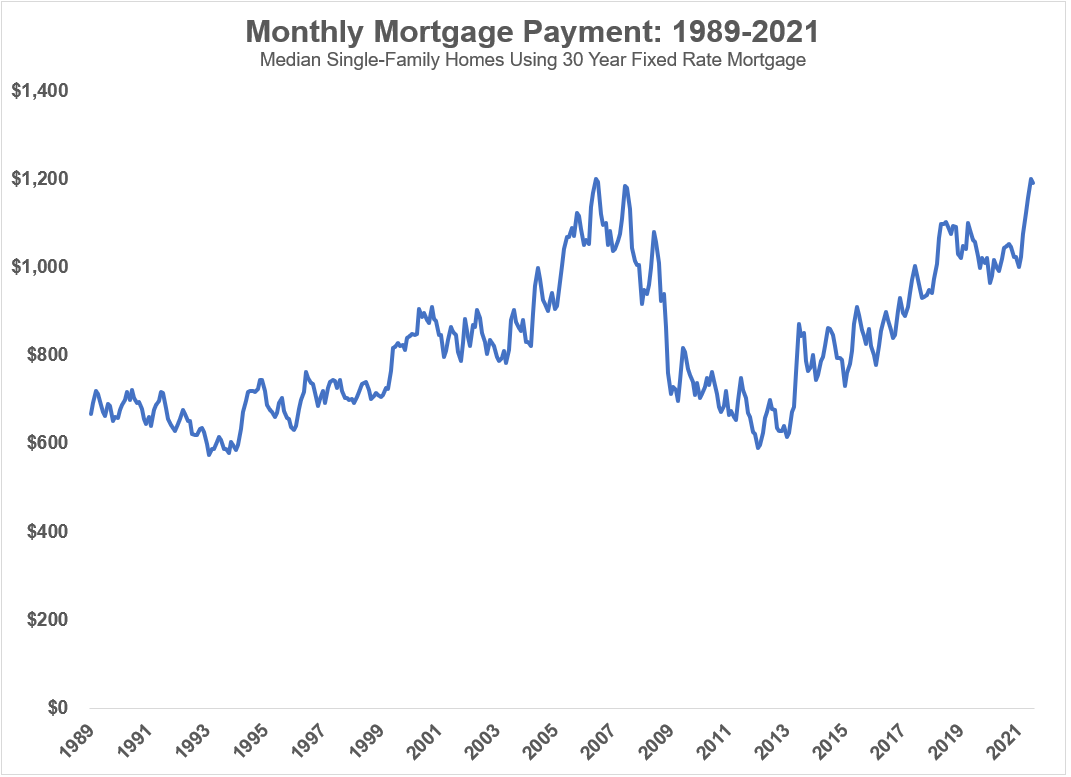

That meant month-to-month mortgage funds for median single household house costs had been reaching all-time highs:

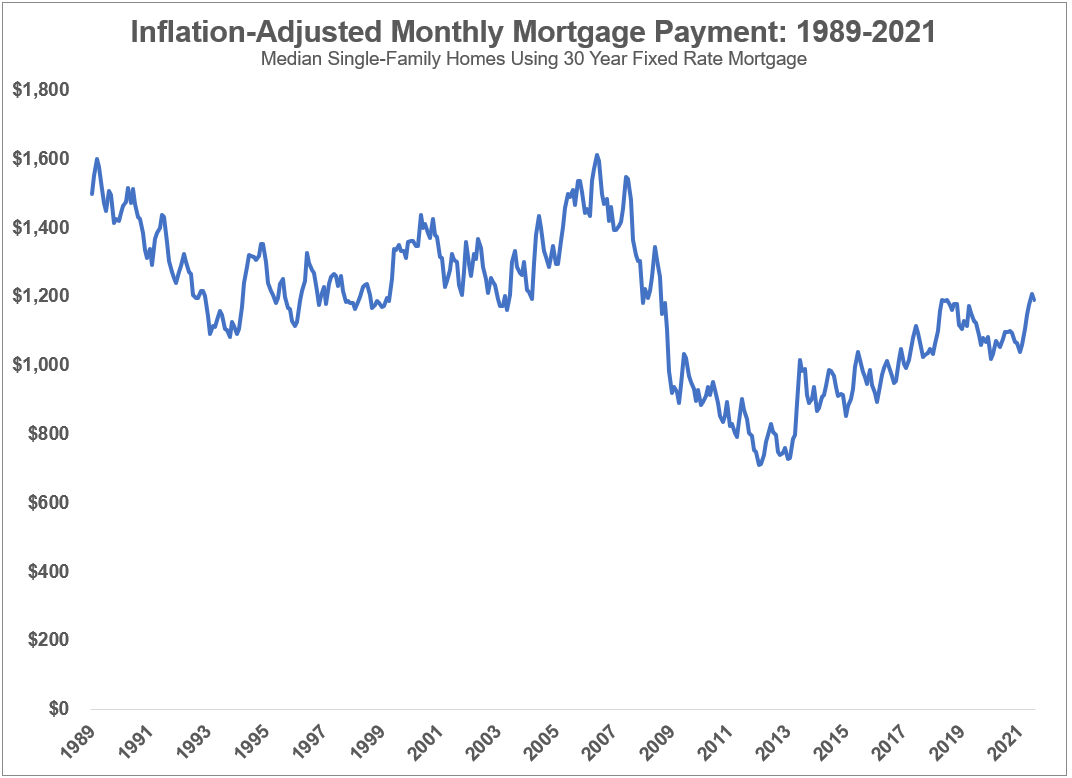

However for those who adjusted these month-to-month funds for inflation issues didn’t look so dangerous:

Adjusted for low rates of interest and inflation, mortgage funds had been a lot increased within the Nineteen Eighties and Nineteen Nineties.

However it was low mortgage charges that actually helped that affordability. Right here’s what I mentioned on the time:

The one variable that would throw a wrench into this equation can be increased mortgage charges.

In my instance from above, a $308k home at 5% mortgage charges can be a month-to-month fee of $1,322. A $367k home can be $1,576/month. These are will increase of round $300/month versus 3% mortgage charges.

Rising charges are much more impactful than rising costs in your month-to-month funds.

If charges had been to rise considerably, you’d anticipate housing costs to fall, at the very least in principle.

The worst-case state of affairs for would-be first-time homebuyers can be for mortgage charges to rise whereas costs don’t fall. Demand would certainly soften if charges rise previous a sure threshold however I don’t know what that threshold is. And there’s no assure housing costs would instantly fall if charges do rise.

Nicely, mortgage charges have risen, greater than doubling from these ranges to greater than 6%.

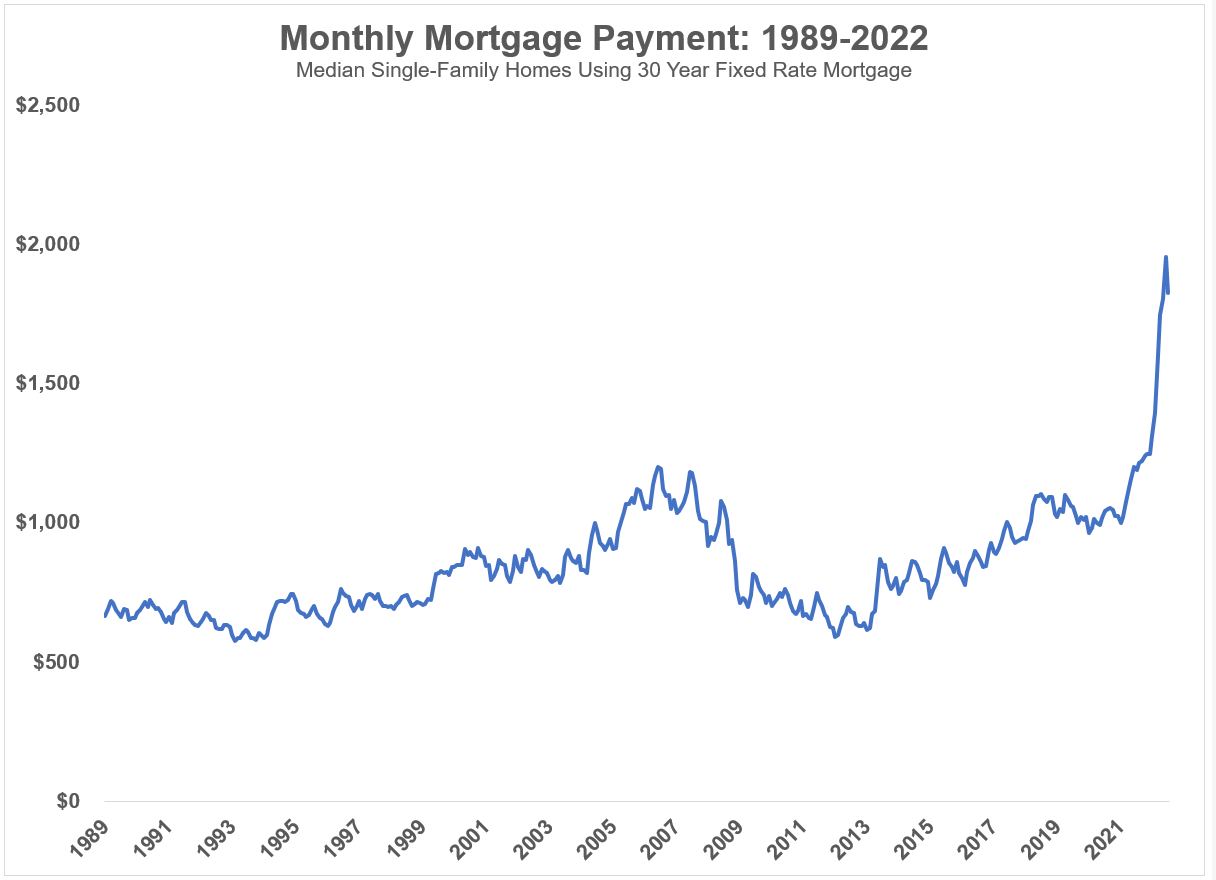

Let’s have a look at these charts only one yr later. The median mortgage fee is now off the charts from a continued improve in house costs and far increased mortgage charges:

Have a look at that blow-off. Not good for anybody trying to purchase their first house.

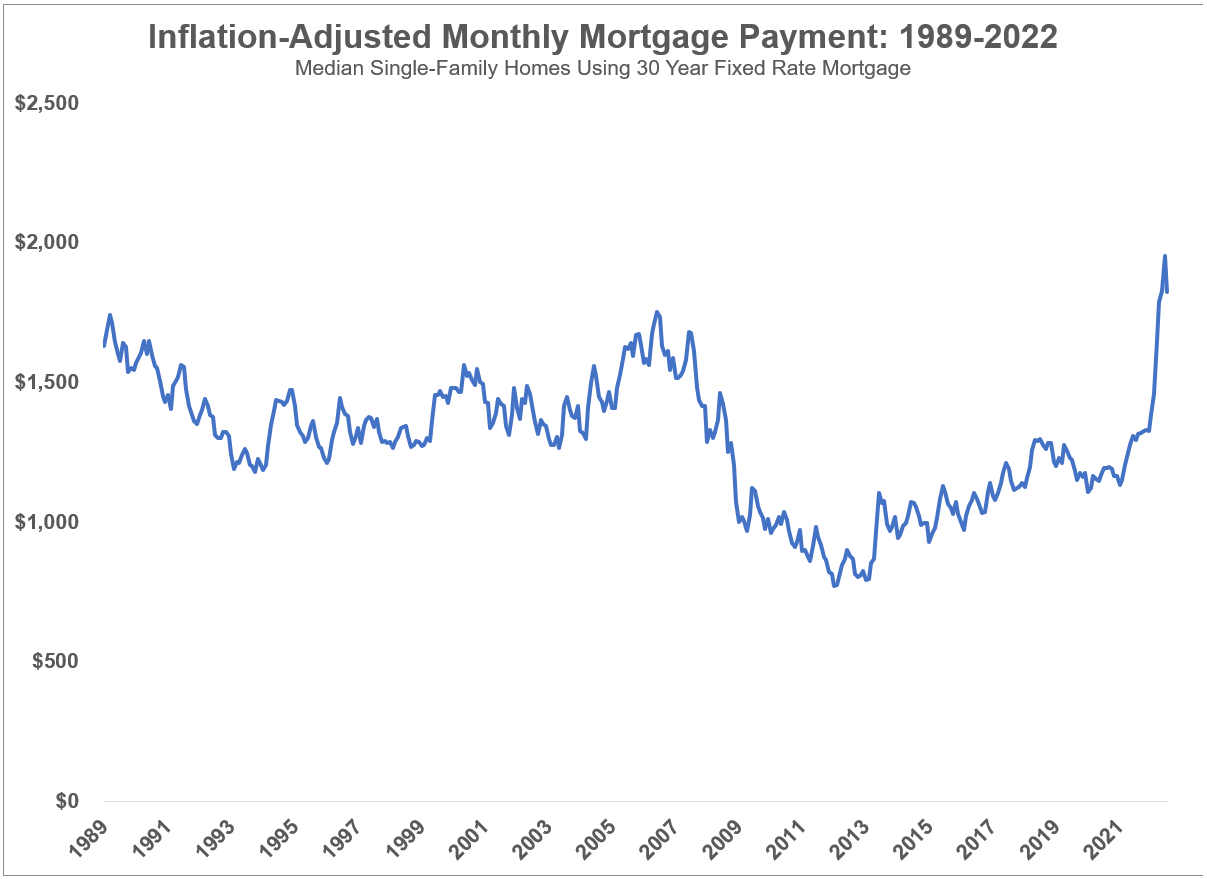

Now let’s see how issues look on an inflation-adjusted foundation:

That is the worst degree of unaffordability we’ve seen because the late-Nineteen Eighties and it occurred within the blink of a watch.1

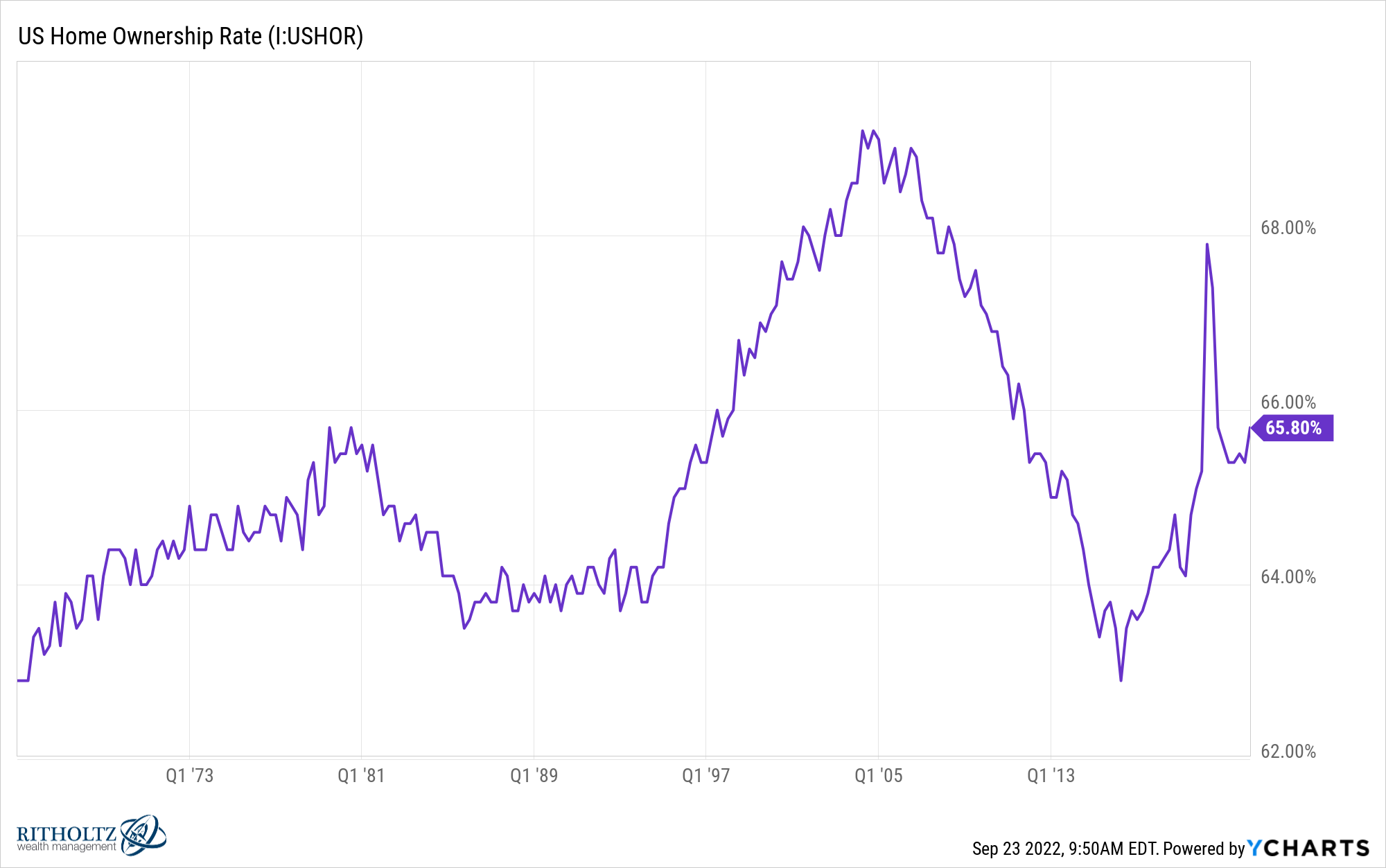

The homeownership price in the USA is round two-thirds:

If you happen to’re one of many fortunate folks on this group who bought a house pre-2022 and locked in a price of three% or decrease, these affordability numbers don’t matter to you (except you propose on buying and selling up).

And it’s luck for those who occurred to purchase or refinance in recent times.

Let’s say you’re an older millennial who bought a house someday between 2015-2020.

The worth of your private home might be up 40-60%. Your mortgage price is round 3% vary. Which means the Fed’s short-term borrowing price is now increased than your mounted price mortgage, which simply so occurs to be top-of-the-line inflation hedges you would ask for. Your fee is mounted and also you’re a lot wealthier from the increase in house costs since 2020.

However what for those who’re a youthful millennial or Gen Z one that lives in an enormous metropolis or missed the window to purchase a home?

Your hire is rising at a quick clip. It’s now rather more costly to purchase a house and kind of unaffordable for a lot of younger folks. Your greatest guess is shopping for a spot now with a excessive mortgage price and hoping the Fed lowers charges after they ship us right into a recession so you’ll be able to refinance. Decide your poison.

If you happen to occurred to purchase at decrease costs with decrease charges you’re not a genius. You bought fortunate.

And for those who didn’t purchase at decrease costs with decrease charges you’re not an fool. It was a case of dangerous luck.

Sadly, luck permeates a lot of your monetary expertise.

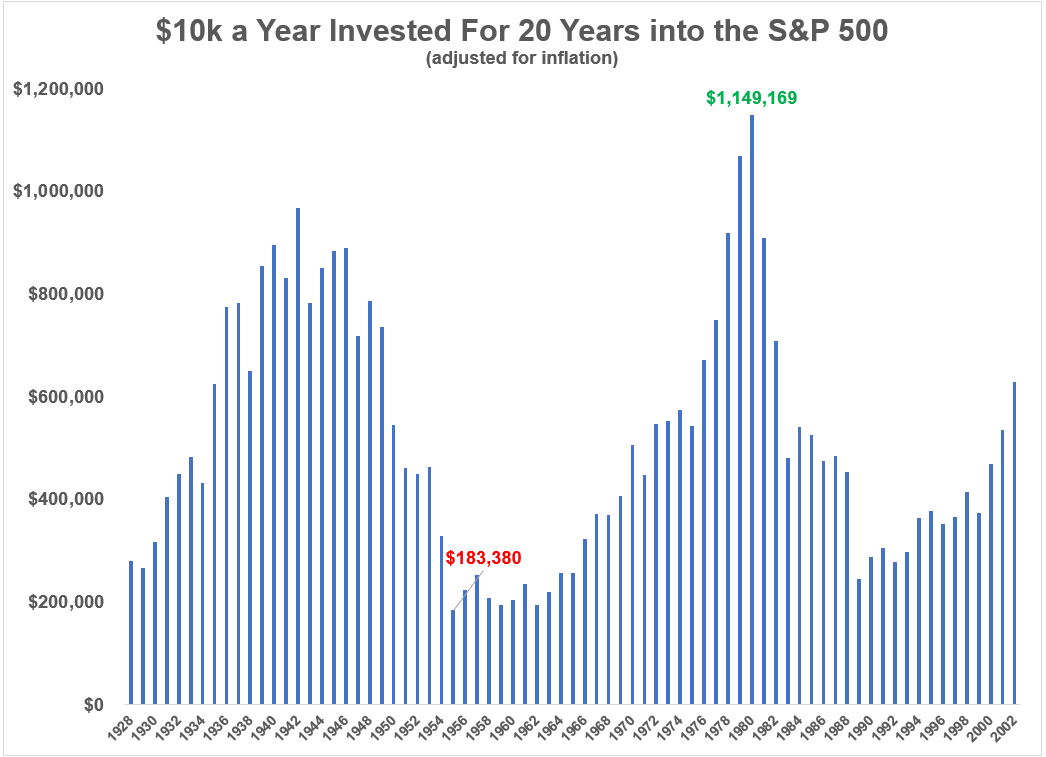

I ran the numbers on a $10k annual funding into the S&P 500, adjusted for inflation, and the outcomes are all around the map:

The distinction between the most effective and worst consequence had nothing to do with the person dutifully saving cash and every little thing to do with after they had been born and commenced saving.

If you happen to had the tailwind of the Fifties, Nineteen Eighties, Nineteen Nineties or 2010s bull market at your again, you probably did rather well within the inventory market.

If you happen to occurred to begin investing within the Thirties or lived by way of the Seventies or 2000s, not a lot.

Sadly, numerous what occurs together with your monetary life is out of your management.

You haven’t any management over what occurs within the inventory market, the housing market, bond market or commodities market. You can not management inflation or rates of interest or tax charges or the Fed or what sort of monetary state of affairs you’re born into.

You’ll be able to management your financial savings price, asset allocation, diversification and work ethic.

It may not appear honest however generally you simply should play the playing cards you’re dealt.

Michael and I spoke about good and dangerous luck within the housing market on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

How the Fed Screwed Up the Housing Market

Now right here’s what I’ve been studying these days:

1And it’s value mentioning I solely have knowledge by way of July 31, 2022. Mortgage charges have risen since then and housing costs haven’t actually softened simply but so it’s solely gotten worse.

[ad_2]