{kind=link}

[ad_1]

Lately, I had a protracted chat with Amit Wadhwaney, the founding father of Moerus Capital Administration and the adviser to Moerus Worldwide Worth Fund. He’s a really considerate and seasoned investor. Listed below are a few of his ideas on his fund and his stock-picking model. I’ve offered a abstract of my notes moderately than an precise Q&A, however the taste of their investing model will hopefully come by way of.

Historical past and coaching:

Mr. Wadhwaney is broadly educated. He earned a Bachelor of Science in chemical engineering from Minnesota, then each a Bachelor of Arts and a Grasp’s in Economics from Concordia College, Montreal. He adopted these with an M.B.A. from the College of Chicago.

His profession started as a enterprise analyst at Domtar, a Canadian forest merchandise firm, then on the Canadian brokerage Bunting Warburg, finding out … effectively, the forest merchandise business. He earned a place as a securities analyst after which as Director of Analysis at M.J. Whitman LLC, a New York-based broker-dealer. Mr. Whitman based Third Avenue Administration, the place Amit labored from 1990 – 2014. In his time on the agency, he was chargeable for each hedge funds (Third Avenue International Worth Fund, LP and the Third Avenue Rising Markets Fund, LP) and a US mutual fund (Third Avenue Worldwide Worth). Amid what may be politely described as “appreciable turmoil at Third Avenue,” Mr. Wadhwaney left to discovered Moerus Capital Administration.

Mandate at Moerus:

The mandate is to run an unconstrained, international portfolio. Which means US, developed worldwide, and rising market shares. The objective is to be prudently opportunistic however with a low turnover. The portfolio modifications each three to 5 years.

Moerus at the moment has about 34 holdings, with Tidewater being the most important place. Wadhwaney acknowledges the excessive mutual fund bills ratio of 1.65%, however it’s a small fund, and he has bills to pay. Wadhwaney says that Moerus is at one finish of the worth chain. Various their friends have disappeared, and a few have diminished. The enterprise of worth investing needed to stretch very exhausting to justify its existence. Moerus will not be nice storytellers, however they know how you can purchase companies which might be capable of repair themselves, and so they purchase these companies at good costs. That’s their Edge.

Why International? Why not simply purchase US corporations for worldwide publicity?

- Cheapness is difficult to search out within the USA.

- There are companies – enterprise fashions or monopolies – overseas that you’ll not discover within the US.

How do you concentrate on threat?

After they consider what can harm the enterprise of the shares they purchase, they have a look at:

- FX Asset-liability mismatch

- Nature of debt construction

- Sensitivity to inflation

Thus, they’re macro-aware. However macro doesn’t decide their inventory selecting. They don’t seem to be sitting round attempting to guess the extent of rates of interest, central financial institution coverage, or commodity costs. They attempt to be in good neighborhoods and attempt to purchase crushed up and depressed shares. They perceive that the time to fixing a beaten-up inventory is kind of variable. Not like bonds, shares have an indeterminate payoff date.

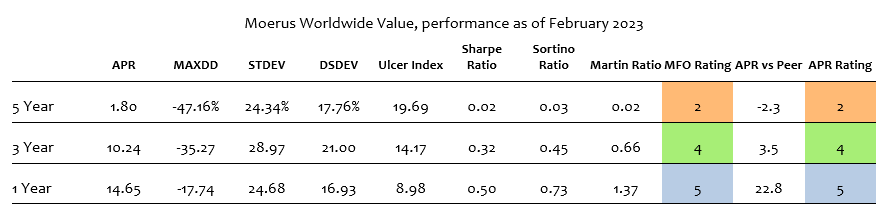

Current efficiency

2020 was a foul yr for the fund, down 10%. They bounced again in 2021, up a strong 18%. However they did even higher in 2022. The fund was up 6% when the markets have been down 15-20%.

What modified in 2021 and particularly 2022, in comparison with 2020?

In what “we did,” nothing modified. Let’s take the case of three shares through which we have been invested.

Inventory 1: Tidewater

Tidewater, an offshore oil exploration and drilling firm, is considered one of their largest holdings, purchased 3-4 years in the past. They purchased it when it emerged from chapter with a clear steadiness sheet. Then in 2020, oil went to a unfavourable worth. Inventory went from $20 to $4. The corporate was financially strong and effectively set as much as take care of it. Due to its nice steadiness sheet, it’s a most well-liked counterparty to the biggies like Exxon and Amerada Hess, who need sturdy service suppliers within the North Sea. The inventory got here again in a really huge manner. Tidewater was not an oil guess. It was a guess on a financially sturdy firm that was constructed to outlive in a low oil worth regime and thrived when oil costs went larger.

Inventory 2: UniCredit

UniCredit, an Italian banking group, is one other instance. When rates of interest have been low, all types of economic corporations – banks and insurance coverage corporations – have been impacted. Moerus purchased UniCredit as a result of such low stage of rates of interest was unintuitive to them. UniCredit did an enormous fairness issuance and jettisoned loads of dangerous debt. Internally, it continued to repair the enterprise and steadiness sheet. The financial institution offered a unit to Amundi, a European asset supervisor. Enhancements have been taking place and the corporate was all set to declare dividends and buybacks, when impulsively, the pandemic hit. Banks, UniCredit together with, cratered. Moerus purchased extra of the inventory. After the pandemic, UniCredit got here out a lot stronger on account of all of its inner fixing. Lately, the ECB has allowed UniCredit to conduct buybacks. Now, the inventory is doing nice.

Inventory 3: Customary Chartered Financial institution

Customary Chartered Financial institution (Stanchart) is a really huge financial institution working in Asia. The earlier CEO was concerned in reckless lending. To win capital markets enterprise from Indian promoters and Indian corporations, the financial institution prolonged these promoters unsecured loans. This led to predictable catastrophe. Invoice Winters was employed from JP Morgan and began cleansing up. Whereas 2020 was a tricky yr for the financial institution, the capital internally was increase. Rising rates of interest and inner self-help have gone a good distance to assist Stanchart’s inventory worth.

Backside Line: studying from his embrace of Astoria, Queens

Wadhwaney got here to New York, and in 1991 decided Manhattan actual property costs have been too excessive. As soon as a worth investor, at all times a worth investor. He went to Astoria, preferred what he noticed, and nonetheless lives in that a part of Queens. “I just like the house and entry to contemporary produce, and the price of dwelling is a lot better.”

That tells an investor all the things they wish to find out about Moerus. They don’t seem to be chasing development. They’re searching for a margin of security in investments, an artwork that’s now misplaced in an age of Zero Day Buying and selling Choices. Don’t ask if Moerus is an efficient fund. Ask if you’re the proper investor to be invested in Moerus. If the frequency matches, it’s exhausting to not become profitable over a protracted interval.

[ad_2]