{kind=link}

[ad_1]

Let’s discuss jellyfish danger for a second. I noticed a lot of them on trip this yr at Gulf Shores, Alabama on daily basis!

In a world crammed with dangers of all types, styles and sizes, the jellyfish is slightly tough to pin down. To some, the chance may appear insignificant, invisible, or shapeless — sort of just like the jellyfish itself. We don’t see them simply, in order that they fly below the radar. There isn’t any horrifying dorsal fin protruding of the water.

But the chance that jellyfish pose is actual and rising. Roughly 150 million persons are stung every year by jellyfish and tons of are killed.[i] In reality, you could be shocked to know that extra folks die every year from jellyfish stings than from shark assaults. Within the Philippines alone, 20-40 folks die from jellyfish stings every year.[ii] And no … I used to be not stung by one!

“Effectively, that’s a life insurance coverage statistic,” you may suppose.

Jellyfish, nevertheless, unfold the chance round. P&C insurers could be to know that jellyfish can harm private watercraft. They will disrupt water-based companies. Yearly, they shut down 2-3 energy stations by clogging water filtration methods. They’ve precipitated close to meltdowns at nuclear energy vegetation.[iii]

Larger total ocean temperatures possible from local weather change are inflicting jellyfish to roam additional afield from their frequent habitats. The expansion of recent breeding areas, reminiscent of offshore wind generators, oil rigs, and oyster beds, has allowed jellyfish to realize a foothold in additional northern tidal areas. In brief, jellyfish are thriving, and jellyfish danger is an actual factor.

Are insurance coverage underwriters protecting observe of world jellyfish developments?

The world of danger is altering quicker than we will be taught.

It might nonetheless appear trite to us, however the jellyfish makes an important instance of dangers that exist and are rising, however nobody is monitoring as a result of nobody, besides marine biologists, actually has the time to trace jellyfish or the chance implications. Each danger, nevertheless, is trending in some route. Dangers are rising. Dangers are combining. Dangers are shrinking. Some dangers are staying the identical. How can we see what we don’t acknowledge as a danger till it sneaks up on us too late? What different dangers are altering resulting from local weather change we’re unaware of? How can we predict what may occur with that danger sooner or later?

Prefer it or not, the world is altering quicker than we will study new dangers and danger developments. On the identical time, now we have applied sciences able to monitoring practically any danger with knowledge, improved methodologies, and AI/ML. In Majesco’s latest thought management report, Underwriting and Loss Prevention to Deal with Rising Insurance coverage Prices, we check out a few of these adjustments in danger and take a better take a look at the applied sciences that ought to be employed to handle danger and decrease prices for insurers to grow to be adept at studying simply as quick because the world is altering. In in the present day’s weblog, we take into account timing. Ought to insurers be making an attempt to sort out in the present day’s underlying dangers, or may they start to assemble what Majesco would time period, “tomorrow’s insights in the present day?”

Is the unpredictable really predictable?

At present, we are actually seeing rising environmental, societal, and expertise dangers which have the potential to intersect and considerably disrupt folks and companies. The Marsh World Dangers Report 2021 for companies notes that the financial, technological, and reputational pressures of the current second danger a disorderly shakeout, threatening to create a big cohort of staff and corporations which can be left behind within the markets of the long run.

For instance, elevated excessive climate occasions and pure disasters have an unprecedented and more and more important impression. In response to the Nationwide Oceanic and Atmospheric Administration, america skilled 20 separate distinctive billion-dollar climate and local weather disasters in 2021, putting it second to 2020 when it comes to the variety of disasters, 20 versus 22, and third in whole prices of $145 billion, solely behind 2017 and 2005.[iv] Forest fires appear to be rising, and with them, property loss. Current twister harm has elevated, and the standard twister avenues appear to be increasing.

In a converging pattern, building prices are rising resulting from provide chain points, elevated prices for supplies resulting from inflation, and a scarcity of building staff. The fast rise in dwelling costs and excessive demand has left many properties uninspected (consumers comply with forego inspection as a “perk” for sellers). A member of the family did and inside weeks we needed to substitute not solely the furnace and air conditioner but in addition {the electrical} panel that was recalled years in the past resulting from fireplace hazard – a major unknown danger. The result’s possible unidentified dangers and underinsured properties for each the insurer and the insured – creating important danger gaps which have monetary, buyer expertise and reputational implications. Loss prevention methods should change if insurers want to stay steady and rising.

Insurers should adapt. The one means the unknown dangers grow to be part of enterprise technique is that if underwriting accounts for adjustments which can be in fixed movement, utilizing variables as numerous as local weather change and building costs. In some ways, each of those parts are predictable. Local weather change is definitely headed in a specific route whereas labor and building prices have really been rising pretty constantly for over a decade, with a bigger bump up to now yr. (See the Mortensen Development Price index right here.) Despite the fact that the chance could seem like rising quicker than we will be taught, the truth is that we could merely want to make use of expertise to show us quicker.

Limiting the aspect of economic shock

Whether or not or not insurers can study danger quick sufficient, a scarcity of efficient pricing adaptation will come again to chunk them with excessive loss ratios and unprofitable books of enterprise. Insurers don’t want to manage the uncontrollable world. They should perceive it in ways in which assist them adapt pricing earlier than monetary outcomes trigger undesirable surprises. Granular element is not about “getting within the weeds.” It’s about stopping the loss that comes from a scarcity of danger data and pricing utility.

Operationally this requires a mix of digital enterprise options together with next-generation

core, digital loss management, digital underwriting workbench, AI/ML fashions, and the power to ingest a variety of information sources from prospects, together with unstructured, video, geospatial, social, IoT units, and extra, to create real-time danger administration and insights.

Insurers are more and more focusing their time and assets on how they will higher assess danger and stop losses to enhance underwriting profitability and buyer experiences.

Insurance coverage has at all times been a data-driven enterprise, however entry to new knowledge sources with AI/ML is redefining the business. At present’s elevated catastrophes, market atmosphere, and strain on profitability demand a better concentrate on preventable losses and higher outcomes by underwriting profitability, proactive danger mitigation to attenuate or remove claims, and enhanced buyer experiences.

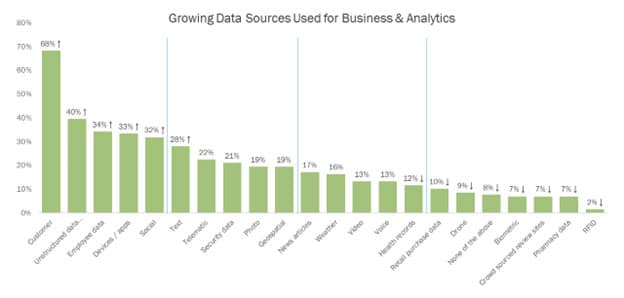

Majesco’s 2022 Strategic Priorities analysis signifies that insurers are more and more investing in clever digital underwriting, loss management, and AI/ML options.[v] Insurers are increasing the information sources from buyer knowledge to unstructured knowledge reminiscent of loss runs and loss management stories to new digital knowledge sources from units, video, geospatial and extra, as represented in Determine 1 under. All of those efforts maintain one factor in frequent: the discount of economic shock by efforts by quicker studying.

Determine 1: Information sources used for Enterprise & Analytics

The brand new and tremendously improved function of information — trainer, tutor, and communicator

An elevated concentrate on loss management and different knowledge has resulted in elevated quantity, selection, and velocity of structured and unstructured knowledge sources. Loss management has moved from surveys with

questions, checklists, and pictures; to leveraging real-time knowledge from sensible units, video, photographs of labels, and extra by danger engineering corporations, buyer self-surveys, and video-guided surveys.

Insurers can use the richer knowledge loss management and different knowledge ingested with superior AI/ML for improved danger evaluation, urge for food evaluation, underwriting, and pricing. Superior AI/ML permits insurers to investigate knowledge in real-time to drive clever decision-making. By figuring out hazards and offering suggestions as knowledge is ingested or collected, carriers and distributors can now create extra worth by proactively addressing points and offering suggestions in actual time.

This considerably broadens the function of underwriting and loss management in a company. All of the sudden, as a substitute of simply pricing with better readability, new knowledge and analytics together with loss management can educate insurers on tips on how to finest reply to danger developments. When paired with the brand new instruments of digital customer support, we might help prepare insureds on tips on how to keep away from dangers, then talk the upcoming dangers as shortly as they’re acknowledged. It shortens the time interval between knowledge seize, predictive analytics, and well timed communication.

Letting the previous educate the long run utilizing cutting-edge expertise

We could not have an correct image of what jellyfish will do subsequent yr, however we do have a reasonably correct understanding of the harm they’ve achieved lately and up to now. On this means, a greater grasp of the actual impression will be ascertained with a point of certainty. The previous will be successfully utilized to the long run.

Loss management applied sciences, reminiscent of these provided by Majesco, have this system in thoughts.

As shortly as the long run is altering, insurers nonetheless perceive the outcomes of damaging and catastrophic impacts. On the subject of constructions and property, they will get a reasonably correct image of which properties are in danger.

In Majesco’s latest weblog, “Is it Time to Rent New Information?,” Patrick Davis explains how Majesco shoppers can now entry loss management knowledge from 16 million property surveys, together with 200 million pictures. When insurers plug new pictures into loss management software program, machine studying takes over and analyzes the dangers inside {an electrical} panel, a sizzling water tank, a roof, a yard, and many others.

Danger traits contained inside the database enable Majesco to create fashions that may decide how a lot danger there may be for nearly any particular given property. It is a superb instance of how expertise might help insurers address a world that’s altering quicker than we will be taught.

The next move now

Insurers have been glorious danger product suppliers for a really very long time. However as the long run appears to come back quicker and unpredictable dangers like jellyfish appear to come out of nowhere, insurers must get forward of the long run in any means they will. They want applied sciences that may work holistically to ingest excessive volumes of information, analyze disparate sorts of knowledge, be taught what’s up forward, and talk it each internally and to policyholders.

The “subsequent technology” of underwriting makes use of in the present day’s expertise in methods that may assist insurers perceive and handle the way forward for danger earlier than it occurs.

To learn extra about loss management, make sure you obtain Underwriting and Loss Prevention to Deal with Rising Insurance coverage Prices. Contained within the report is a brief case examine on how the described applied sciences have helped a business property provider to enhance income with higher knowledge and fewer journey and staffing hours.

And keep in mind … be careful for the jellyfish!

To be taught extra about Majesco’s Underwriting 360, Loss Management, Information & Analytics, and P&C Core Suite options, go to the Majesco web site in the present day.

[i] Chabin, Michael, The best way to deal with the worldwide jellyfish risk, The Washington Publish, July 5, 2019

[ii] Legislation, Yau-Hua, Jellyfish nearly killed this scientist. Now, she needs to save lots of others from their deadly venom, Science.org, November 8, 2018

[iii] Izadi, Elahe, How jellyfish have grow to be nature’s final guerrilla protesters in opposition to energy vegetation, The Washington Publish, July 7, 2015

[iv] Smith, Adam, “2021 U.S. billion-dollar climate and local weather disasters in historic context,” NOAA Local weather.gov, January 24, 2022, https://www.local weather.gov/news-features/blogs/beyond-data/2021-us-billion-dollar-weather-and-climatedisasters-historical

[v] Majesco, “2022 Strategic Priorities Report”

[ad_2]