{kind=link}

[ad_1]

Key Highlights

1. Persevering with on the trail of Fiscal Consolidation

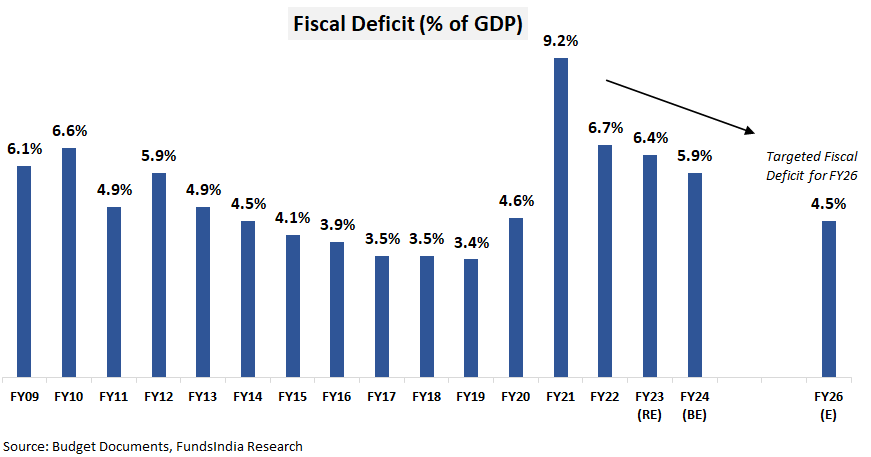

- Projected fiscal deficit at 5.9% of GDP for FY24 – according to the fiscal consolidation glide path – to scale back fiscal deficit to 4.5% of GDP by FY26

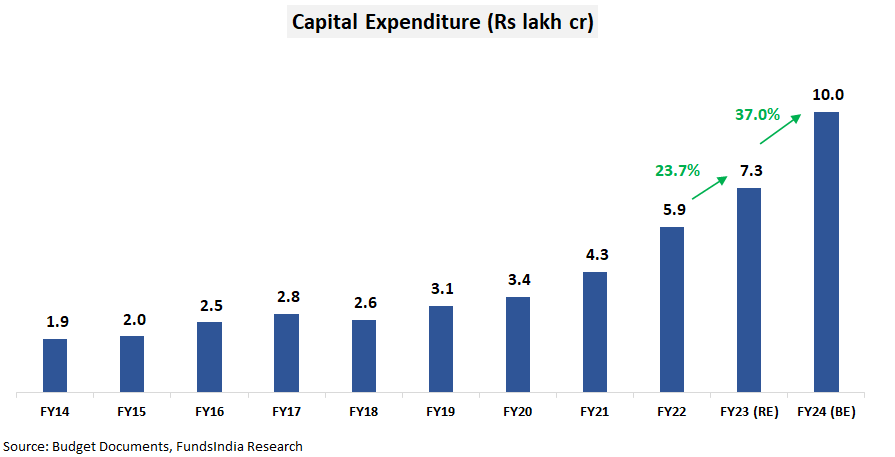

2. Robust thrust on Capital Expenditure (Infrastructure) – has important multiplier results on progress and employment

- 37% enhance in Capital Expenditure from Rs 7.3 lakh cr in FY23 (RE) to Rs 10 lakh cr in FY24

- Main focus is on:

- Street Transport and Highways (Rs 2.6 lakh cr)

- Railways (Rs 2.4 lakh cr)

- Defence (Rs 1.6 lakh cr)

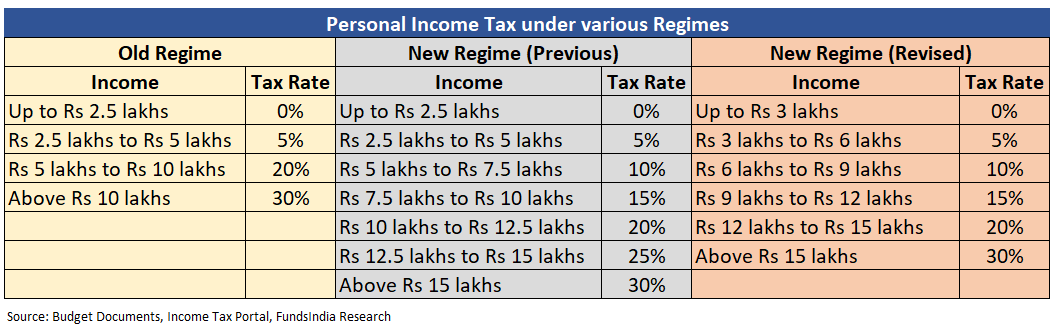

3. Lower in Private Earnings Tax underneath New Tax regime

A number of modifications have been made to the brand new revenue regime to make it extra enticing (particulars in a later part).

4. No modifications to Fairness or Mutual Fund taxation

Finances in Visuals

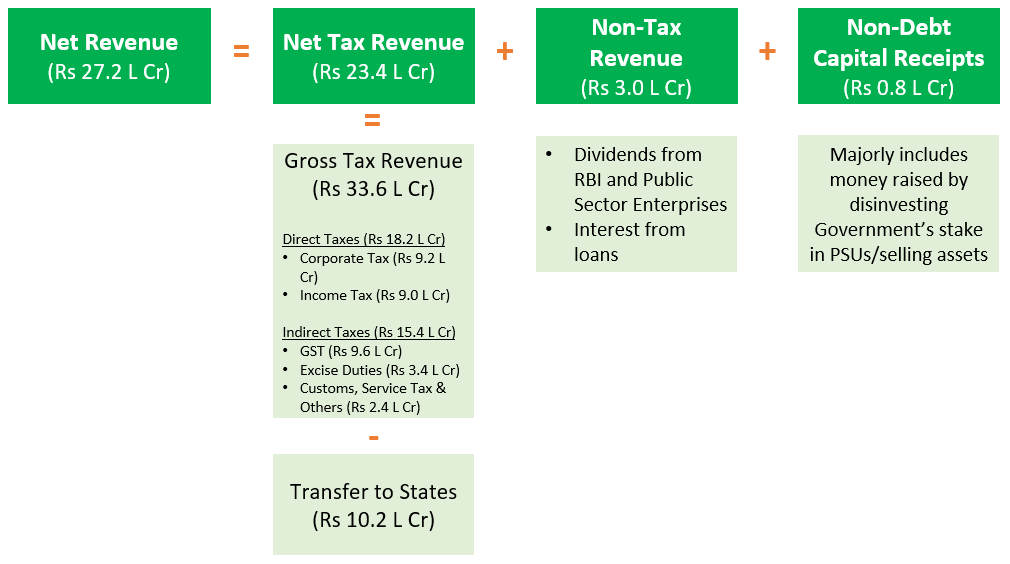

The place does the cash come from?

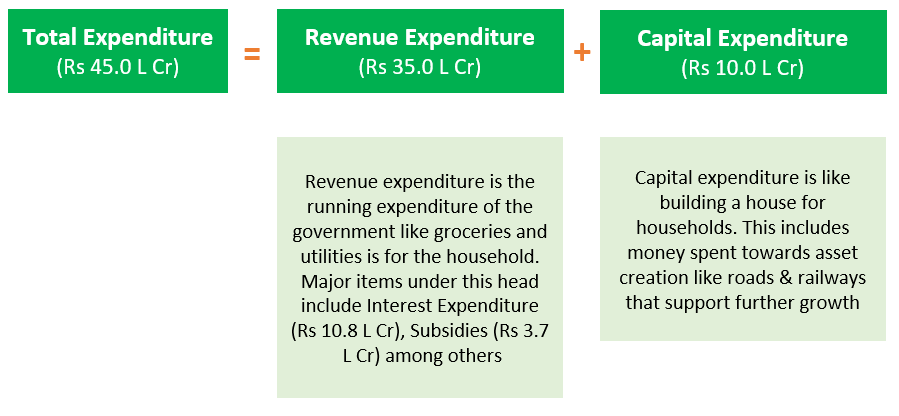

The place does the cash go?

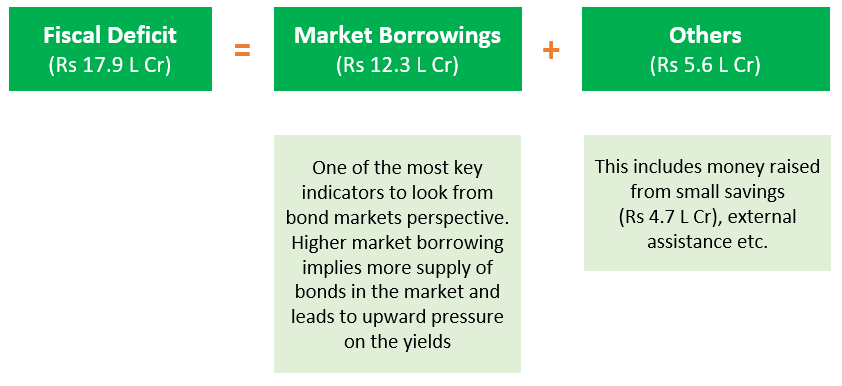

How is the deficit financed?

Fiscal Consolidation On Observe

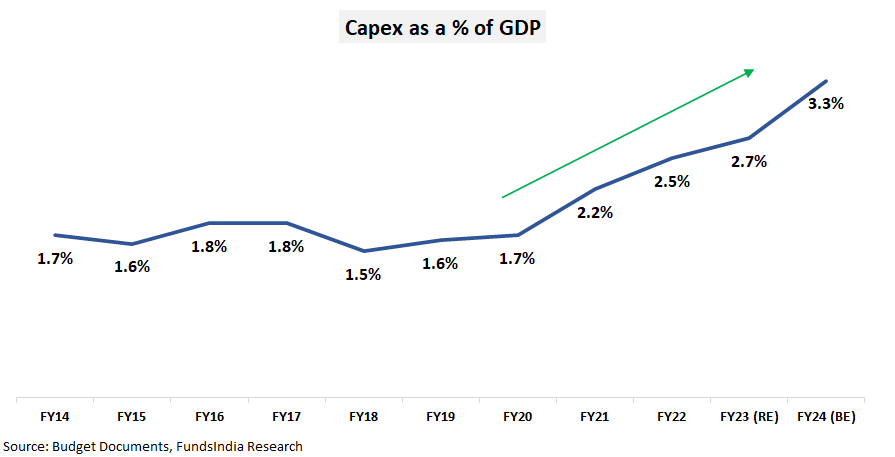

Thrust on Capex Continues

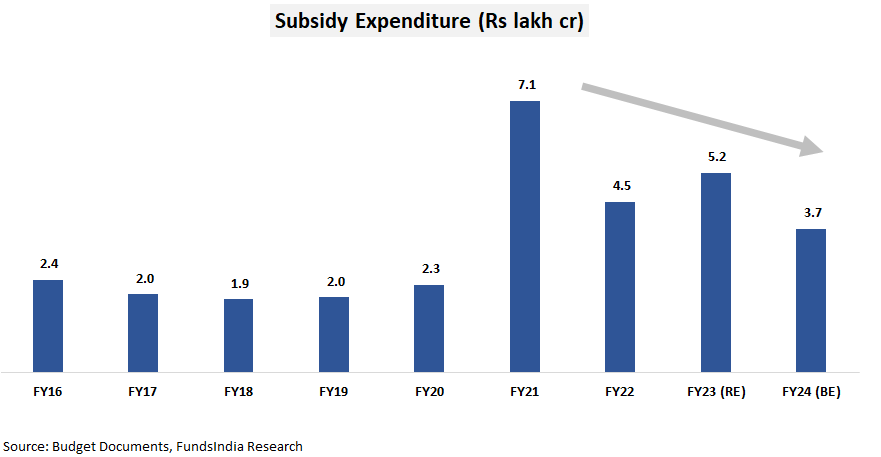

Subsidy bills proceed to slip

What’s in it for you?

1. No change in Fairness or Mutual Fund Taxation

- Taxation of fairness, fairness mutual funds and different non-equity mutual funds stays the identical

2. Nudge in the direction of New Earnings Tax Regime with a number of revisions

- Revisions within the revenue tax slabs – The tax slab underneath the new regime has been revised as follows

- Improve within the Tax Rebate restrict – The tax rebate restrict has been elevated to Rs. 7 lakhs (from Rs. 5 lakhs). Which means taxable revenue as much as Rs. 7 lakhs can be basically tax-free from FY24 (any tax paid may be claimed again when submitting the returns).

- Normal deduction profit prolonged to the brand new regime – Normal deduction of Rs 50,000 which was thus far accessible solely underneath previous tax regime has now been prolonged to new tax regime.

- Reduction for Excessive Earners – Surcharge on the tax paid by people incomes over Rs. 5 crores has been lowered from 37% to 25%. This transformation reduces the efficient tax price from 42.7% to 39%.

3. Maturity quantity on Insurance coverage premium above Rs 5 lakhs can be taxed

Earnings from life insurance coverage insurance policies (non-ULIPs) the place the mixture premium is as much as Rs 5 lakhs will proceed to be tax exempt. However revenue from insurance policies with yearly premium greater than Rs 5 lakhs can be taxed on the relevant slab charges.

4. Cap imposed on reinvestment of positive factors from residential property

At present, there isn’t any must pay taxes on the long-term capital positive factors from the sale of an asset, if the positive factors are used to buy a residential property. This tax exemption has now been capped at Rs 10 crores.

5. Market Linked Debentures to get taxed per slab

Till now, there was a taxation arbitrage in Market Linked Debentures (a sort of a listed debt safety). When you held an MLD for greater than a 12 months after which bought it, it was labeled as long run capital positive factors which had been taxed at 10%. Going ahead, this taxation arbitrage received’t be relevant and any capital positive factors from MLDs can be handled as short-term capital positive factors and can get taxed on the relevant slab charges no matter the holding interval. This has no impression on the taxation of mounted revenue mutual funds.

6. Greater Tax Collected at Supply for overseas remittances

The Tax Collected at Supply on funds made by the Liberalised Remittance Scheme (excluding training and medical bills) has been elevated from 5% to twenty%. For example, if you happen to spend money on overseas shares underneath LRS, you’ll have to shell out 20% extra on the time of cost. Nonetheless this may be adjusted towards the tax payable or claimed again as refund whereas submitting the returns.

7. Improve in Earned Depart Encashment Restrict

The restrict of Rs 3 lakhs for tax exemption on go away encashment on retirement of non-government salaried workers has been elevated to Rs 25 lakhs.

8. Most Deposit Restrict for SCSS has been doubled

The restrict for the quantity that may be deposited underneath the Senior Residents Financial savings Scheme has been doubled from Rs 15 lakhs to Rs 30 lakhs

9. What may get Cheaper / Costlier?

- Cheaper: Mobiles Telephones, TV Units, Lab Grown Diamonds, Pecan Nuts and so forth

- Costlier: Cigarettes, Gold & Silver articles, Imitation Jewelry, Imported Vehicles, Toys and so forth

Fairness View: Development stays the precedence – Optimistic for Fairness Markets

The Union Finances FY24 continues to place progress on the forefront. The main focus stays on capital expenditure that may drive a multiplier impression on financial progress and employment. That is evident from the sharp 37% enhance in capital expenditure for FY24 (versus a meagre 1% enhance in income expenditure).

Opposite to some pre-budget rumours, no modifications had been made to the fairness capital positive factors taxation. This removes the close to time period uncertainty on the subject of fairness taxation.

Previous to the finances, we had a POSITIVE view on Equities with a 5-7 12 months horizon

Our Fairness view is derived primarily based on our 3 sign framework pushed by

- Earnings Cycle

- Valuation

- Sentiment

As per our present analysis we’re at

NEUTRAL VALUATIONS + EARLY PHASE OF EARNINGS CYCLE + NEUTRAL SENTIMENTS

We anticipate a strong earnings progress atmosphere over the following 3-5 years. This expectation is led by Manufacturing Revival, Banks – Bettering Asset High quality & pickup in mortgage progress, Revival in Actual Property, Authorities’s concentrate on Infra spending (which continues in FY24 Finances), Early indicators of Company Capex, Structural Demand for Tech companies, Structural Home Consumption Story, Consolidation of Market Share for Market Leaders, Robust Company Steadiness Sheets (led by Deleveraging) and Govt Reforms (Decrease company tax, Labour Reforms, PLI) and so forth.

The fairness market valuation measured through FundsIndia Valuemeter has turned NEUTRAL as on 31-Jan-2023 (was within the costly zone in Dec-22).

From a sentiment standpoint, path of FII flows stays a key close to time period set off. The market expectations on subsequent 12 months elections which can begin getting constructed by the fag finish of this 12 months can even have an affect on close to time period returns.

General, we preserve our Optimistic view on Indian equities from a 5-7 12 months time-frame. The Finances bulletins reinforce our sturdy earnings progress outlook.

Mounted Earnings View: Stability on the fiscal entrance – Beneficial for Debt Markets

The Fiscal Deficit for FY24 at 5.9% of GDP is broadly constant with the fiscal glide path and according to our expectation. The federal government additionally reiterated its intention to deliver this deficit quantity right down to 4.5% of GDP by FY26.

FY24 Internet Market Borrowing (Gsec +T payments) at INR 12.3 lakh crores is also according to the bond markets expectations.

The absence of serious detrimental surprises within the finances appears to have saved the bond yields in verify.

In our evaluation, we could also be near peak coverage charges pushed by

- Sharp fall in home inflation in current months – CPI inflation dropped by 169 foundation factors from 7.41% in Sep-22 to five.72% in Dec-22

- The present repo price at 6.25% is comfortably above RBI’s inflation expectation of 5.0% in Q1 FY24.

- The exterior financial atmosphere is displaying some indicators of easing amid falling world inflation and slowing tempo of price hikes by the US FED.

We anticipate RBI to go for an extended pause in price hikes from hereon or after yet another price hike to six.50% within the subsequent coverage.

Given the sharp enhance in yields over the past 12 months, 3-5 12 months bond yields (GSec/AAA) proceed to stay enticing. The present yields present a adequate buffer for increased returns in comparison with FDs over a 3+ 12 months time-frame even when yields had been to quickly barely inch up additional.

We desire debt funds with

- Excessive Credit score High quality (>80% AAA publicity)

- Brief Length (1-3 years) or Goal Maturity Funds (3-5 years)

Different articles you might like

Submit Views:

296

[ad_2]