{kind=link}

[ad_1]

Latest analysis has linked local weather change and socioeconomic inequality (see right here, right here, and right here). However what are the results of local weather change on small companies, notably these owned by folks of coloration, which are usually extra resource-constrained and fewer resilient? In a sequence of two posts, we use the Federal Reserve’s Small Enterprise Credit score Survey (SBCS) to doc small companies’ experiences with pure disasters and the way these experiences differ based mostly on the race and ethnicity of enterprise homeowners. This primary publish exhibits that small corporations owned by folks of coloration maintain losses from pure disasters at a disproportionately larger price than different small companies, and that these losses make up a bigger portion of their whole revenues. Within the second publish, we discover the flexibility of small corporations to reopen and to acquire catastrophe reduction funding within the aftermath of local weather occasions.

What Components Contribute to Catastrophe Vulnerabilities?

Catastrophe vulnerability, outlined because the susceptibility to extreme local weather occasions, is linked to financial, social, and locational components. For instance, folks of coloration and people with low incomes are extra seemingly to reside in high-risk flood zones. And in states like Florida, a rising choice for prime elevation is rising housing costs in areas with decrease flood danger that have been historically inhabited by folks of coloration. To the extent that corporations owned by folks of coloration usually tend to be positioned in communities of coloration, these tendencies suggest that they could be priced out of areas with decrease local weather danger.

Disparities within the impression of pure disasters, amongst those that are uncovered to them, are additionally associated to current inequalities. Practices like “redlining” have continued to maintain residence values in low-income and predominantly Black areas decrease. This may increasingly scale back the capability of communities to finance disaster-resilient infrastructure if, for instance, authorities applications favor areas with larger property values within the allocation of catastrophe mitigation grants. Certainly, people residing in previously redlined districts—lots of whom are folks of coloration—stay weak to higher flood danger as in comparison with non-redlined districts.

Are Small Companies Owned by Individuals of Shade Extra More likely to Report Catastrophe-Associated Losses?

We use knowledge from the SBCS for the interval 2019-21 to doc the impression of pure disasters on small companies. The annual survey offers detailed info on the operations and monetary circumstances of companies with fewer than 500 workers and data the demographics of agency homeowners. Notably, this info permits us to narrate local weather outcomes to race instantly, relatively than to the racial profile of geographic areas, as in some current analysis.

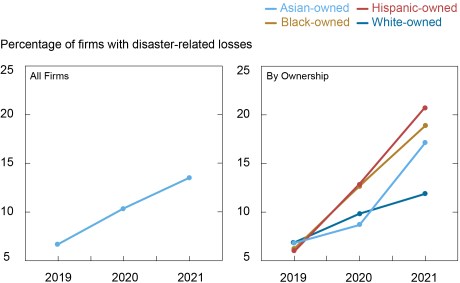

The 2019, 2020, and 2021 surveys included 9,315, 15,234, and 18,190 respondents, respectively. The pure catastrophe module of the survey asks respondents whether or not their enterprise sustained any direct or oblique losses from a pure catastrophe previously twelve months. The fraction of corporations experiencing disaster-related losses rose from 7 p.c in 2019 to 14 p.c in 2021 (see left panel of the chart beneath). The racial disparities in these losses elevated as nicely. Whereas there have been few disparities in 2019, in 2021, 19 p.c of Black-owned corporations, 21 p.c of Hispanic-owned corporations, and 17 p.c of Asian-owned corporations reported disaster-related losses whereas solely 12 p.c of white-owned corporations did (see proper panel beneath).

The incidence and racial disparity of losses seem to maneuver collectively, a sample that exists even outdoors our pattern interval. For instance, in 2017 (a yr with widespread hurricanes and extreme storms), there have been giant disparities between Hispanic- and white-owned corporations in reported losses amongst SBCS respondents.

Fraction of Companies with Losses and Disparities in Losses Have Each Elevated since 2019

Notes: For respondents in every year and race/ethnicity class, the traces present the share of corporations who answered sure to the query “Inside the previous 12 months, did your small business maintain direct or oblique losses from a pure catastrophe apart from COVID-19 (e.g., hurricane, wildfire, earthquake, and so on.)?” A agency is taken into account Black-, Hispanic-, or Asian-owned if a minimum of 51 p.c of its fairness stake is held by homeowners figuring out with the group. A agency is outlined as white-owned if a minimum of 50 p.c of its fairness stake is held by non-Hispanic white homeowners. Race/ethnicity classes will not be mutually unique. An statement is excluded from the pattern whether it is lacking a response to the query or if the proprietor’s race is just not noticed. The pattern swimming pools employer and nonemployer corporations. Responses by employer and nonemployer corporations are weighted individually on quite a lot of agency traits to match the nationwide inhabitants of employer and nonemployer corporations, respectively. To assemble a pooled weight, we use the employer (nonemployer) weight if the agency is an employer (nonemployer).

Amongst these in disaster-related areas, extra corporations owned by folks of coloration face damages than white-owned corporations. We present this by specializing in the subsample of small companies positioned in counties designated as disaster-affected by the Federal Emergency Administration Company (FEMA) within the interval of the survey. We discover that 24 p.c of Black-owned corporations, 23 p.c of Hispanic-owned corporations, and 22 p.c of Asian-owned corporations reported disaster-related losses in 2021, in comparison with 17 p.c of white-owned corporations.

Present disparities, similar to the situation of communities of coloration in low-lying areas with poor disaster-resilient investments, can differ inside counties. Utilizing county fastened results regressions, we discover that in 2021, Black-owned small companies have been 5 proportion factors extra seemingly than their white-owned counterparts to report disaster-related losses, supporting the disparity in local weather results even inside comparatively small geographic areas.

Are Enterprise House owners in Some States Extra Weak to Catastrophe-Associated Losses?

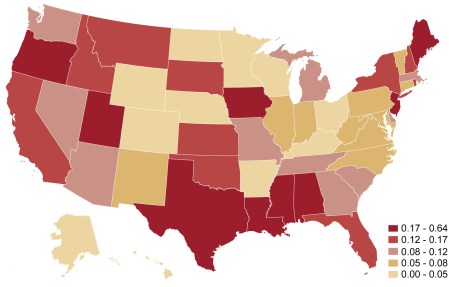

States and cities positioned within the Southern U.S. are notably prone to disasters, as they’ve older infrastructure and are disproportionately positioned in floodplains; because the map beneath exhibits, the fraction of corporations reporting pure disaster-related losses in 2021 is very excessive in states alongside the Gulf Coast. States within the Center Atlantic (New Jersey and New York) and on the West Coast even have a excessive fraction of small companies reporting disaster-related losses. In 2020 Census knowledge, the states with the very best focus of African Individuals—Mississippi, Georgia, and Louisiana, and in addition Washington, D.C.—overlap with these high-risk areas. This means that companies owned by folks of coloration (additionally concentrated in these 4 localities, based on the SBCS) could also be weak resulting from their focus in notably prone states. When wanting inside Census Divisions, we discover {that a} higher fraction of Black-owned corporations report disaster-related losses than white-owned corporations, and this disparity has elevated between 2019 and 2021. Thus, regional disparities have elevated pari passu with nationwide disparities.

Fraction of Companies Reporting Catastrophe-Associated Losses by State, 2021

Notes: The warmth map exhibits the fraction of corporations in a given state that answered sure to the query “Inside the previous 12 months, did your small business maintain direct or oblique losses from a pure catastrophe apart from COVID-19 (e.g., hurricane, wildfire, earthquake, and so on.)?” All observations which might be lacking a response to the query are excluded from the pattern. The pattern swimming pools employer and nonemployer corporations. Responses by employer and nonemployer corporations are weighted individually on quite a lot of agency traits to match the nationwide inhabitants of employer and nonemployer corporations, respectively. To assemble a pooled weight, we use the employer (nonemployer) weight if the agency is an employer (nonemployer). The survey was fielded September-November 2021.

Do Companies Owned by Individuals of Shade Undergo Bigger Catastrophe-Associated Losses?

The 2020 and 2021 surveys ask respondents that report disaster-related losses to estimate the worth of these losses. We notice that, since responses are voluntary (with 78 p.c of eligible respondents opting in), corporations with decrease losses could also be much less prone to full the climate-related questions, implying an upward bias within the reported losses. Nevertheless, there isn’t any motive to suppose that less-impacted corporations owned by folks of coloration usually tend to skip these questions than less-impacted white-owned corporations.

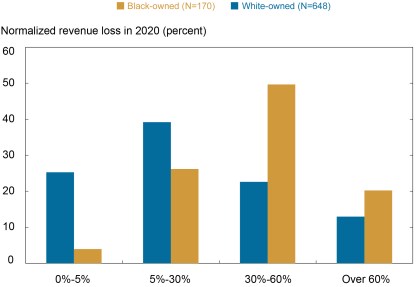

We normalize these losses as a proportion of a agency’s whole income within the yr prior. As a result of folks of coloration confronted higher income losses on account of the COVID-19 pandemic, we depend on disaster-loss knowledge from the 2020 survey, which is normalized by whole revenues from 2019, earlier than the onset of the pandemic.

For many small companies of coloration, disaster-related losses have been a big share of their revenues. For instance, 20 p.c of Black-owned companies reported losses that quantity to greater than 60 p.c of 2019 income, whereas simply 4 p.c of such corporations had losses of 0-5 p.c of 2019 income (see chart beneath). In distinction, for many white-owned companies, disaster-related losses have been a comparatively small share of revenues. For instance, 25 p.c of white-owned corporations skilled disaster-related losses of 0-5 p.c of 2019 income and 39 p.c had losses of 5-30 p.c, whereas solely 13 p.c had losses of greater than 60 p.c of whole income.

Black-Owned Companies Have Larger Income Shares of Catastrophe-Associated Losses

Notes: Amongst corporations that reported disaster-related losses, the 2020 SBCS asks “What’s the estimated worth of your small business’s losses on account of the pure catastrophe?” Respondents can choose from six classes. Companies are additionally requested to report their whole revenues from 2019 by choosing from eight ranges. To compute the normalized income loss, we divide the midpoint of the disaster-related losses vary by the midpoint of the agency’s income vary. The normalized losses are grouped into 4 bins, that are proven on the x-axis. The bars present the share of corporations in every race/ethnicity class with normalized disaster-related losses in a given bin. A agency is taken into account Black-owned if a minimum of 51 p.c of its fairness stake is held by homeowners figuring out as Black. A agency is outlined as white-owned if a minimum of 50 p.c of its fairness stake is held by non-Hispanic white homeowners. Race/ethnicity classes will not be mutually unique. An statement is excluded from the pattern whether it is lacking a response to the query or if proprietor race is just not noticed. The pattern swimming pools employer and nonemployer corporations. Responses by employer and nonemployer corporations are weighted individually on quite a lot of agency traits to match the nationwide inhabitants of employer and nonemployer corporations, respectively. To assemble a pooled weight, we use the employer (nonemployer) weight if the agency is an employer (nonemployer). The survey was fielded September-October 2020.

It is very important notice that, after we examine disaster-related losses on a greenback foundation, relatively than as a proportion of revenues, there’s little proof of racial disparities. This means that our result’s pushed by the decrease revenues of Black-owned corporations, implying that pure disasters are a higher burden for corporations owned by folks of coloration by way of their interplay with current racial disparities which have a unfavourable impact on small enterprise revenues. For instance, relative to white-owned corporations, Black-owned companies are youthful, have much less entry to startup capital, make use of fewer folks, have a more durable time accessing credit score, and lack expertise in household companies—all of that are related to decrease revenues.

Wanting Forward

Our findings recommend that small companies owned by folks of coloration and positioned specifically geographic areas are particularly weak to pure disasters. Furthermore, these disparities have elevated over the three years in our pattern, in tandem with the frequency and severity of catastrophe occasions. These disparate outcomes are prone to be carefully linked to the broader challenges confronted by small companies of coloration in accessing credit score in addition to to underinvestment in local weather infrastructure in areas the place low-income and high-minority communities reside. As such, addressing these challenges could show particularly efficient in ameliorating disparities in local weather outcomes. In our subsequent publish, we study the sources that small companies can depend on to deal with losses following disasters, similar to entry to catastrophe reduction.

Martin Hiti was a summer season analysis intern within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Claire Kramer Mills is a Communication Improvement Analysis Supervisor within the Federal Reserve Financial institution of New York’s Communications and Outreach Group.

Asani Sarkar is a monetary analysis advisor in Non-Financial institution Monetary Establishment Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this publish:

Martin Hiti, Claire Kramer Mills, and Asani Sarkar, “How Do Pure Disasters Have an effect on U.S. Small Enterprise House owners?,” Federal Reserve Financial institution of New York Liberty Road Economics, September 6, 2022, https://libertystreeteconomics.newyorkfed.org/2022/09/how-do-natural-disasters-affect-u-s-small-business-owners/.

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).

[ad_2]