{kind=link}

[ad_1]

Hindustan Unilever Ltd. – Irresistible Development

Hindustan Unilever Restricted (HUL) is India’s largest fast-moving shopper items firm. It’s a majority-owned subsidiary of UK large Unilever, one of many world’s main suppliers of meals, dwelling care, private care, and refreshment merchandise with gross sales in over 190 nations. As India’s largest shopper items agency, HUL markets manufacturers that embody drinks, meals, and residential and private care items.

With 50+ manufacturers spanning 15 distinct classes similar to material options, dwelling and hygiene, life necessities, pores and skin cleaning, skincare, hair care, color cosmetics, oral care, deodorants, tea, espresso, ice cream & frozen desserts, meals, and well being meals drinks. The corporate is part of the on a regular basis lifetime of thousands and thousands of shoppers throughout India. The corporate has about 21,000 staff, ~1330 suppliers, and round 9 mn shops promoting their merchandise. 9 out of 10 Indian households use a number of of their manufacturers.

Merchandise:

Its portfolio contains main family manufacturers similar to Lux, Lifebuoy, Surf excel, Rin, Wheel, Glow & Pretty, Pond’s, Vaseline, Lakmé, Dove, Clinic Plus, Sunsilk, Pepsodent, Closeup, Axe, Brooke Bond, Bru, Knorr, Kissan, Kwality Wall’s, Horlicks and Pureit.

Subsidiaries: As on March 31, 2022, the corporate has a complete of 12 subsidiaries particularly Unilever India Exports Ltd, Lakme Lever Pvt. Ltd, Hindustan Unilever Basis, and so on.

Key Rationale:

- Market Chief – HUL is the biggest FMCG firm in India with market management throughout product segments. The corporate has 16 manufacturers with over Rs.1,000 crore in annual gross sales. By way of market share, its manufacturers maintain the highest two spots in most classes it has a presence in. Greater than 75% of its enterprise is profitable each worth and quantity market shares. The market share acquire of the corporate in FY22 was the best it had in additional than a decade. The market share in Hair Care touched a 15-year excessive in 2021. Surf Excel is the number one laundry model and within the final 5 years, the liquid detergents and material conditioners enterprise has grown 4 instances.

- Q3FY23 – HUL posted general income of Rs.15,597 crs, a rise of 16% YoY in Q3FY23, supported by elevated quantity progress (5% YoY), considerably outperforming the market. The house care phase had one other wonderful quarter, logging income of Rs.5,514 crs (32% YoY, 7% QoQ) and double-digit quantity progress. Development was pushed by increased costs for the material wash and family care portfolios. The wonder and private care phase grew 11% YoY to Rs.5,764 crs (3% QoQ), led by sturdy worth and quantity progress in pores and skin cleaning, in addition to different segments. In the meantime, income from the meals and refreshment phase income grew 7% YoY to Rs.3,700 crs (-1% QoQ), led by sturdy efficiency in meals, ice cream, and low merchandise.

- New Royalty Construction – Administration has authorised new royalty and central providers association charge construction that includes a rise from 2.65% to three.45% (+80bps) of the turnover. The rise can be staggered over the subsequent 3 years, with a 45bps enhance from February to December 2023, 25bps from January to December 2024, and 10bps from January 2025. That is anticipated to influence margins within the close to time period. Nonetheless, with the noticed moderation in inflation charges, the corporate, supported by its premiumisation and economies of scale, will be capable to offset the influence.

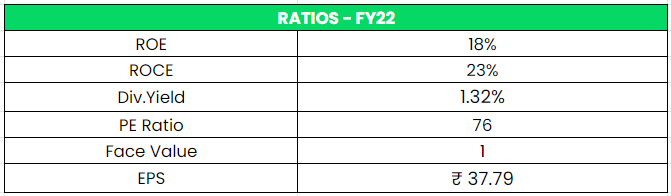

- Monetary Efficiency – The corporate is financially sturdy with zero debt and wholesome money & equivalents of Rs. 7490 crs. It has a very good return on fairness (ROE) observe report with 5 Yr avg. RoE of 30%+. The corporate additionally pays a wholesome dividend for the buyers persistently. The working money move of the corporate has grown at a 12% CAGR for the interval between FY17-22.

Business:

The fast-moving shopper items (FMCG) sector is India’s fourth-largest sector and has been increasing at a wholesome price through the years on account of rising disposable revenue, a rising youth inhabitants, and rising model consciousness amongst shoppers. With family and private care accounting for 50% of FMCG gross sales in India, the business is a crucial contributor to India’s GDP. Indian magnificence and private care (BPC) market are the eighth largest on this planet. Fragrances, Make-up and Cosmetics, and Males’s Grooming are all anticipated to develop at a CAGR of 12-16%. The non-public hygiene market is predicted to succeed in $15 Bn by 2023 in India. Conventional commerce is the dominant retail channel in India accounting for 81.8% of FMCG gross sales and main the way in which for FMCG progress. With over 11.5 million offline shops rising at a 4% compounded annual price, at the moment, this extremely dynamic retail channel is evolving to be extra handy for shoppers.

Development Drivers:

- The Authorities of India has authorised 100% FDI within the money and carry phase and in single-brand retail together with 51% FDI in multi-brand retail.

- Rural per capita consumption will develop 4.3 instances by 2030, in comparison with 3.5 instances in city areas.

- India’s retail buying and selling sector attracted US$ 4.11 billion FDIs between April 2000-June 2022. 100% FDI in single-brand retail beneath the automated route.

Peer Evaluation:

The corporate has generated higher Gross sales and PAT CAGR than its friends traditionally and has been constant by way of general Efficiency. By way of profitability progress, HUL is likely one of the finest amongst FMCG firms.

Opponents: P&G Hygiene, Colgate-Palmolive, and so on.

Outlook:

The Administration is seeing a gradual enchancment within the FMCG enterprise atmosphere. The corporate stays cautiously optimistic within the close to time period and expects price-led progress. The corporate has skilled an actual comeback in rural markets in comparison with the earlier months. It additionally believes that the height inflation has cooled off and on the present inflation ranges, the margins can develop on the again of premiumisation. The corporate continued to launch new merchandise with a give attention to improvements. It launched a brand new model beneath the cleaning soap class ‘St. Ives’ & variants beneath Lifebuoy and new shampoo variants beneath ‘Tresemme’. It additionally launched variants within the tea, espresso, and jams & soup phase. With commodity costs staying at present ranges, the gross margin trajectory stays upward. The corporate is more likely to enhance advert spending to perk up quantity progress within the subsequent few quarters.

Valuation:

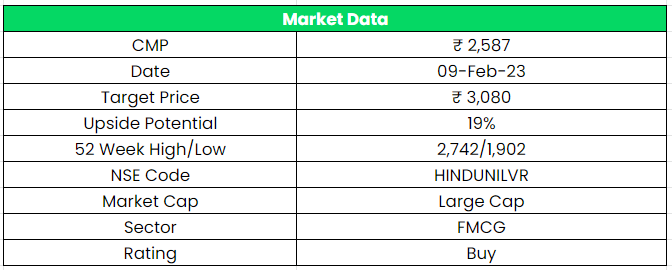

Hindustan Unilever continues to outperform the market and acquire market share regardless of the macro challenges. With the inflation cooling off on account of steady price hikes and enhancing rural demand, we anticipate the amount progress to proceed throughout the portfolio. Therefore, we suggest a BUY score within the inventory with a goal worth (TP) of Rs.3080, 55x FY25E EPS.

Dangers:

- Uncooked Materials Danger – Any enhance in uncooked materials prices similar to Crude oil and Palm oil will influence the margins of the corporate.

- Royalty Worth Danger – Any slowdown within the rural restoration will influence the income and thereby influence the power of the corporate to offset the Royalty worth hike.

- Aggressive Danger – The Indian FMCG business has each organised and unorganised gamers throughout segments and merchandise. HUL continues to face stiff competitors, with the entry of recent gamers, together with multinationals, in segments similar to soaps and detergents, private care merchandise, and packaged meals.

Different articles you might like

Publish Views:

149

[ad_2]