{kind=link}

[ad_1]

Firm Overview:

Electronics Mart India Ltd (EMIL) was arrange within the yr 1990 by Pavan Bajaj and Karan Bajaj. It’s the 4th largest client sturdy & electronics retailer in India and the biggest participant within the Southern area in income phrases with dominance within the states of Telangana and Andhra Pradesh. With a focus on main home equipment (equivalent to air conditioners, televisions, washing machines, and fridges), cellphones, small home equipment, IT, and different merchandise, the corporate presents all kinds of products. It stacks over 6000 inventory conserving items (SKUs) throughout client durables and electronics unfold throughout greater than 70 manufacturers; each Indian and international.

Funding Rationale:

Diversified Portfolio: As of Aug’31, 2022, the corporate operates and manages 112 shops with a retail enterprise space of 1.12 million sq. ft., situated throughout 36 cities/city agglomerates. The Firm has a long-standing relationship with main client manufacturers which permits them to acquire merchandise at aggressive charges. EMIL retails a diversified product portfolio of client sturdy objects, which embrace mobiles, massive home equipment equivalent to air conditioners, fridges, and different small home equipment. The corporate retails merchandise of well-known manufacturers equivalent to Sony, LG, Oppo, and Vivo amongst others. Aside from its generic model of Bajaj Electronics used to market all merchandise, the corporate has additionally created two area of interest retail manufacturers. It has specialised shops beneath the identify “Kitchen Tales” which cater to kitchen specific-requirements. As well as, there’s additionally a specialised retailer format known as “Audio & Past” which is targeted on high-end residence audio and residential automation options and merchandise.

Monetary Observe Document: Electronics Mart India has generated good income progress within the final 4 years. The corporate’s 3 12 months income CAGR (FY19-22) stands at 38% and PAT CAGR stands at 29%. For FY22, the corporate reported a 35.8% YoY progress in its income from operations at Rs.4349 crs. The corporate additionally reported a 76.2% YoY enhance within the internet income at Rs.104 crs for a similar interval. After all, the web margins at 2.39% could also be low, however that’s usually the character of the retail enterprise. Gross sales of mobiles throughout FY22 had been Rs.1395 crs, the biggest contributor to the general income of the corporate. The mobiles additionally remained the quickest rising phase, reporting a 22% CAGR over FY19-FY22.

Versatile Enterprise Mannequin: The corporate operates with a mixture of possession and lease rental fashions. To be able to optimise profitability, operational flexibility, and make sure the excellent retailer places (in densely populated neighbourhoods and residential places), the corporate has a versatile technique of proudly owning or leasing the premises based on availability, value, and different concerns. Out of the entire 112 client sturdy and digital retail shops, 93 retail shops have been taken on lease and 11 retail shops are owned by the corporate and eight retail shops are partly owned and partly leased.

Key Dangers:

Geographical Focus Danger – The vast majority of the corporate shops’ focus is in Andhra Pradesh and Telangana. It at present plans to broaden in different areas too, nevertheless such investments could or is probably not profitable.

Aggressive Danger – The standard organised brick-and-mortar gamers face stiff competitors from e-commerce gamers and different smaller unorganised gamers. Though the market is at present dominated by brick-and-mortar gamers as bodily shops allow prospects to the touch and really feel the product they’re shopping for, steering given by gross sales representatives additionally instills confidence in first-time patrons.

Outlook:

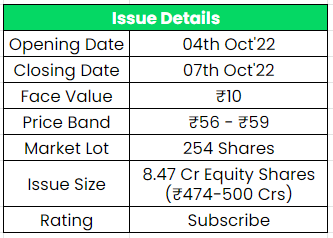

The IPO being solely a recent concern would improve the share capital of the corporate and therefore it will be EPS dilutive for the shareholders. The corporate has just one listed end-to-end peer named “Aditya Imaginative and prescient” based on its DRHP. The corporate has stiff competitors from Reliance digital (a subsidiary of Reliance retail), Croma, Vijay Gross sales, Girias, Viveks, and so forth. If we annualize FY23 earnings and attribute it to the post-IPO totally diluted fairness capital base, then the asking worth is at a P/E of round 13.95x. Primarily based on FY22 earnings, the P/E stands at 21.85x which could be very much less in comparison with its closest peer Aditya imaginative and prescient which is buying and selling at 48.5x P/E for a similar interval. Therefore, we offer a ‘Subscribe’ ranking for this IPO.

In case you are new to FundsIndia, open your FREE funding account with us and revel in lifelong research-backed funding steering.

Different articles you could like

Put up Views:

108

[ad_2]