{kind=link}

[ad_1]

Avenue Supermarts (DMart) Ltd. – Wealth Builder

Avenue Supermarts Restricted is an India-based firm, which owns and operates DMart shops. DMart is a grocery store chain that gives clients a spread of residence and private merchandise beneath one roof. The Firm presents its merchandise beneath varied classes, equivalent to mattress and tub, dairy and frozen meals, vegatables and fruits, crockery, toys and video games, children attire, girls’ clothes, attire for males, residence and private care, every day necessities, grocery and staples, and personal DMart manufacturers.

The Firm opened its first retailer in Mumbai, Maharashtra in 2002. As of December 31, 2022, the Firm had 306 working shops with a Retail Enterprise Space of 12.6 million sq. ft throughout Maharashtra, Gujarat, Daman, Andhra Pradesh, Karnataka, Telangana, Tamil Nadu, Madhya Pradesh, Rajasthan, NCR, Chattisgarh, and Punjab.

Merchandise & Providers:

The corporate has a variety of merchandise beneath three segments.

- Meals – This class contains staples, groceries, snacks & processed meals, dairy & frozen merchandise, drinks, and confectionery.

- Non-Meals (FMCG) – This class contains residence care merchandise, private care and toiletries, and different over-the-counter merchandise.

- Normal Merchandise & Attire – This class contains mattress & tub merchandise, toys & video games, residence home equipment, crockery, utensils, plastic items, clothes, and footwear.

Subsidiaries: As on Mar’22, the corporate has 5 subsidiaries.

Key Rationale

- Robust place within the organized retail phase – Market place is strengthened by regular same-store development (barring fiscal 2021), retail productiveness, and quick gestation for brand new shops. Avenue Supermarts at present operates 306 shops (as on Dec’30, 2022) beneath the DMart model. Robust procurement skills, low-priced merchandise together with high-cost management will result in better footfall. This leads to excessive stock turnover and income per sq. foot (sq ft) and interprets into industry-leading retail retailer productiveness. Combination income per sq. ft at about Rs.27,454 in fiscal 2022 (Rs.27306 in 2021) is larger than most retailers in the identical phase. At present, the operations of the corporate are largely concentrated in West and South India. Anticipated massive cluster-focused retailer addition over the subsequent three years will assist diversify geographical attain. Observe report of outpacing friends in development, sturdy merchandising, compelling worth proposition, and advantages of economies of scale will strengthen the market share of DMart over the medium time period.

- Q3FY23 – Avenue Supermarts reported a income development of 26% YoY in Q3FY23 to Rs.11569 vs. Rs.9218 crs in Q3FY22. The corporate added 4 new DMart retailers (22 in 9MFY23) taking the overall retailer rely to 306 with a complete enterprise space of 12.6 million sq ft. The common sq. ft of recent shops added is round 60000 (vs. FY22 common of ~41000). D-Mart prepared on-line enterprise) continues to carry out nicely with income development of 72% YoY to Rs.264 crs. Income per sq ft did witness a marginal enchancment on a YoY foundation (~3% YoY) to Rs.9182.

- New Section – DMart has entered into a brand new phase by commencing a pharmacy shop-in-shop via its subsidiary (Replicate Healthcare and Retail Non-public Restricted). At present, the challenge is within the pilot stage. The Administration highlighted that the brand new phase will complement its present enterprise mannequin because it makes use of current retailer infrastructure and no separate Capex is required. Please observe D-Mart already sells OTC merchandise, nevertheless, extra readability on the pure pharma portfolio is pending from the administration.

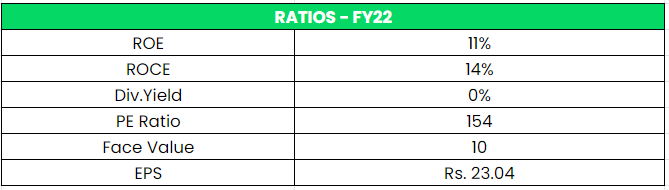

- Monetary Efficiency – Regardless of capital intensive technique, the corporate has maintained excessive ROE and ROCE compared to the {industry}. The corporate has generated a income CAGR of 30%, an EBITDA CAGR of 34%, and a PAT CAGR of 38% for the interval of FY13-22. The web money circulate from Operations grew at a 3-year 21% from Rs.1153 crs in FY19 to Rs.2050 crs in FY22.

Trade Evaluation

The retail market in India has undergone a significant transformation and has witnessed great development within the final 10 years. Indian retail market is projected to succeed in roughly $2 Trn by 2032 from 690 $ Bn in 2021. India at present has the 4th Largest retail market on the planet. Indian retail market recovered from pandemic lows and grew 10% YoY from 630 $ Bn to succeed in 690$ Bn in 2021. The retail sector in India contributed ~800 Bn to India’s GDP in FY20 and employed 8% of its workforce (35+ Mn). It’s anticipated to create 25 Mn new jobs by 2030. The general retail {industry} is estimated to have grown by 16-17% in FY2021-22 and inside this, the organized brick-and-mortar {industry} is estimated to have grown by 19-21%. E-Commerce continued its acceleration throughout FY2021-22. Client adoption of E-Commerce continued in the course of the yr. The {industry} is estimated to have grown by 27-32% throughout FY2021-22. Inside the E-Retail, Meals & Grocery phase continued to see sturdy development in FY2021-22.

Development Drivers

- By 2030 India will add 140 mn middle-income and 21 mn high-income households – Resulting in an enormous rising center class.

- Rural per capita consumption will develop 4.3 occasions by 2030, in comparison with 3.5 occasions in city areas.

- India’s retail buying and selling sector attracted US$ 4.11 billion FDIs between April 2000-June 2022. 100% FDI in single-brand retail beneath the automated route.

Peer Evaluation

Rivals: Vmart, Trent, and so forth.

D-Mart is the one profitable retail enterprise even within the pandemic occasions in contrast with its friends. It’s simply understood via the comparability that D-Mart has a wholesome RoE and RoCE with a powerful EPS in FY22. The corporate is repeatedly producing working money circulate which is used within the growth of additional shops.

*Took TTM EPS & P/E for Comparability

Outlook

The corporate has been on an growth spree within the final 3 years with a powerful sq. ft addition. The common dimension of recent shops is 60000 sq. ft vs. 35000 sq. ft just a few years again (3 Yr CAGR of ~22%). The Administration highlighted that FMCG and staples continued to outperform the overall merchandise and attire phase. On the account of festive purchases within the Normal Merchandise & attire phase, Q3 usually tends to yield gross margins in extra of 15%. Nonetheless low gross margin (14.8%) recorded in Q3FY23 displays some challenges within the quick time period, which may presumably be on account of heightened aggressive depth over the previous two years and inflationary stress nonetheless pertaining to the discretionary worth phase. Regardless of the scenario, D-Mart continues to stay India’s most worthwhile low-cost retailer, a powerful play on India’s retail development story, and a key beneficiary of the unorganized to organized phase shifts.

Valuation

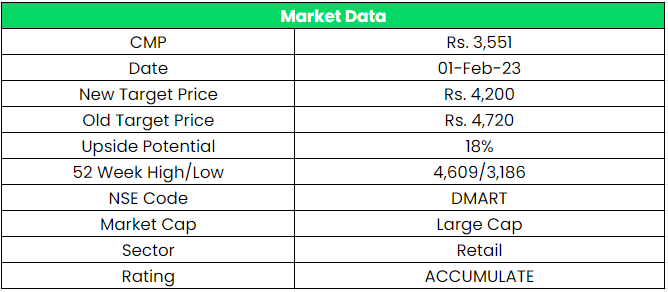

We imagine the restoration in gross sales of normal merchandise and attire phase is across the nook as FMCG corporations are more likely to go on the decrease uncooked materials value advantages to the shoppers. Furthermore, the RBI’s stance on controlling the general inflation will profit the decrease finish of the shoppers which is able to improve the general demand cycle. Therefore, we suggest an ACCUMULATE ranking within the inventory with the goal value (TP) of Rs.4200, 70x FY25E EPS.

Dangers

- E-Commerce Threat – There was a major shift in shopper habits post-Covid-19 – in direction of on-line commerce. Underinvestment in on-line grocery would harm DMart’s market share. On-line would harm DMart’s margins, as sometimes on-line accounts for decrease gross sales of normal merchandise, which has excessive margins.

- Free Cashflow Threat – DMart owns a majority of the shops, because it buys actual property. With sturdy retailer opening capex, FCF era over the subsequent couple of years may stay subdued and will get delayed much more if leased retailer openings are low.

- Aggressive Threat – Sustenance of on a regular basis decrease costs is crucial for the success of the corporate. Nonetheless, with rising competitors, the corporate might be compelled to extend discounting to keep up its loyal clients and its aggressive benefit. This might affect margins which are already wafer-thin.

Supply – Tickertape, Firm’s Web site, BSE Web site

Different articles it’s possible you’ll like

Submit Views:

137

[ad_2]