{kind=link}

[ad_1]

What’s the debt mutual fund taxation from 1st April 2023? Whether or not they be taxed as per tax slab or indexation profit accessible? Do you have to put money into Debt Funds?

In a shocking transfer, the federal government amended sure taxation guidelines in its Finance Invoice 2023. On this, the most important information which was making a type of NOISE from so-called monetary consultants is debt mutual fund taxation.

Debt Mutual Funds Taxation from 1st April 2023

The brand new debt mutual fund taxation is efficient from 1st April 2023. Therefore, no must press the PANIC BUTTON!!

This modification to finance invoice 2023 created three classes of mutual funds for TAXATION.

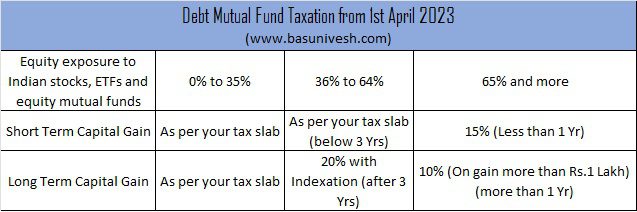

# Mutual Funds holding greater than 65% or extra in Indian fairness, Indian fairness ETFs, or fairness funds

On this class, there isn’t any change in taxation. They’re taxed like fairness funds. In case your holding interval is lower than a yr, then STCG is relevant and taxed at 15%. Nonetheless, in case your holding interval is greater than 1 yr, then LTCG is relevant and taxed at 10% (over and above the aggregated long-term capital acquire of Rs.1 Lakh). As there isn’t any change on this class, I hope it’s clear for you.

# Mutual Funds holding lower than 65% or greater than 35% in Indian fairness, Indian fairness ETFs, or fairness funds

Right here additionally there isn’t any change. They’re taxed like debt funds (as per the previous rule). In case your holding interval is lower than three years, then the acquire is taxed as STCG and the speed is as per your tax slab. Nonetheless, if the holding interval is greater than three years, then taxed at 20% with an indexation profit.

# Mutual Funds holding lower than or equal to 35% of Indian fairness, Indian fairness ETFs, or fairness funds

Here’s a large change (if the modification handed in parliament). The taxation is as per your tax slab. No query of LTCG or STCG. This taxation rule might be relevant from 1st April 2023. Although it’s unclear as of now, many assume that investments finished as much as thirty first March 2023 are grandfathered.

Due to this, many are very indignant with the federal government (I can perceive buyers’ anger however I hate the anger of the finance business. As a result of it’s primarily as a result of they lose the enterprise).

The identical might be tabulated as under.

Debt Mutual Funds Taxation from 1st April 2023 – Do you have to put money into Debt Mutual Funds?

Contemplating all these modifications, it’s nonetheless price contemplating debt mutual funds for our investments? Few funds might change the mandate by growing the publicity of arbitrage alternative for greater than 35% to be eligible for debt mutual fund indexation. To what extent such a change in mandate will impression fund efficiency is unknown to us. Nonetheless, if one is searching for a long-term tax benefit, then one can go for this.

Allow us to now talk about some positives and negatives of each Financial institution FDs (RDs) and Debt Mutual Funds primarily based on this new change.

# Security

As I’ve defined in my earlier submit “Most secure Brief Time period Funding Plans 2023“, financial institution FDs give you a assure of as much as Rs.5 lakh solely. If you’re searching for full security, then it’s important to search for Publish Workplace Time period Deposits.

Nonetheless, within the case of debt mutual funds, they’re market-linked, and the returns should not assured and are primarily based on sure dangers like rate of interest threat, default threat, or credit score downgrade threat. Those that are able to take the danger for the sake of returns can discover as now each FDs and Debt Funds have a degree play when it comes to taxation. However ensure that it’s possible you’ll achieve success or unsuccess additionally.

# Taxation

Although after this sudden change in guidelines taxation of debt funds, FDs appear to be higher. However one factor it’s important to discover is that within the case of financial institution FDs, it’s important to pay the tax on an accrual foundation (TDS can be yet one more unfavourable). Nonetheless, within the case of debt funds, the taxation might be on the time of withdrawal. With this logic, debt funds have a bonus over FDs.

# Consolation

Simply because taxation is identical for each FDs and Debt Funds doesn’t imply in observe you put money into FDs. As many people are month-to-month buyers, making a month-to-month FD could also be cumbersome. Nonetheless, within the case of mutual funds, a SIP is the only option. One might argue of RD. However many banks have restricted intervals of RD. Therefore, in observe, I feel, MFs are higher for many people.

# Liquidity

Flexi FDs give you the liquidity choice. Nonetheless, when you guide the conventional FDs, then it’s important to pay a sure early withdrawal penalty (irrespective of no matter could be the interval). Nonetheless, within the case of debt funds, after a sure interval, there won’t be any exit load. Therefore, liquidity is extra and fewer cost-effective than Financial institution FDs.

# Set off and carry ahead capital positive factors and losses

Within the case of debt mutual funds, because the acquire is taken into account capital positive factors (in FDs it’s revenue from different sources), you possibly can set off and carry ahead the capital acquire and losses. Nonetheless, this function shouldn’t be accessible with FDs.

Contemplating all these options, hoping mutual fund corporations change the mandate to align this taxation. Till that interval, higher to attend and watch. No must panic concerning the current investments.

[ad_2]