{kind=link}

[ad_1]

Most American customers possible are aware of credit score scores, as each lender in the US makes use of them to judge credit score threat. However the Buyer Lifetime Worth (CLV) that many corporations use to focus on adverts, costs, merchandise, and repair ranges to particular person customers could also be much less acquainted, or the Affluence Index that ranks households based on their spending energy. These are just some amongst a plethora of scores which have emerged lately, consequence of the considerable client information that may be gathered on-line. Such client scores use information on age, ethnicity, gender, family revenue, zip code, and purchases as inputs to create numbers that proxy for client traits or behaviors which might be of curiosity to corporations. In contrast to conventional credit score scores, nevertheless, these scores aren’t accessible to customers. Can a client profit from information assortment even when the following scores are ultimately used “towards” her, as an example, by enabling corporations to set individualized costs? Would it not assist her to know her rating? And the way would corporations attempt to counteract the buyer’s response?

Considerations about “Scoring”

A distinguishing characteristic of those scores is that the information brokers that produce them additionally promote them to corporations for market-segmentation methods. Thus, these scores don’t merely have an effect on a client’s interplay with a single agency: the knowledge carried by the rating creates hyperlinks throughout interactions with completely different corporations and industries over time. The argument in favor is that information assortment provides worth by creating beneficial properties from commerce, and scores are a handy manner of packaging information. However opposed welfare results can come up. For instance, if a client makes a giant buy, main her “profitability” rating to extend, she might face greater costs tomorrow.

In a latest paper, we developed a mannequin of score-based value discrimination. Our mannequin shuts down any worth creation to isolate the mechanisms by which customers might be harmed by information assortment, and the concentrate on value discrimination stems from the more and more granular e-commerce focusing on and product-steering methods that make de facto discriminatory pricing an actual chance. In our setup, a client interacts with a sequence of corporations, and her willingness to pay for the corporations’ merchandise is her non-public data. As a result of purchases carry details about willingness to pay, and the latter is positively correlated over time, corporations use scores which might be primarily based on indicators of previous purchases to set costs. On this context, our evaluation examines how client welfare is affected by the interaction between completely different levels of client sophistication (does the buyer know concerning the scores and the hyperlinks they create?) and of rating transparency (can customers verify their present rating?).

Harms and Advantages

Value discrimination unambiguously harms naïve customers—that’s, those that don’t acknowledge the hyperlinks throughout transactions—however it may possibly profit strategic customers. Particularly, within the naïve case, client welfare falls with the standard of the indicators accessible to the corporations. Companies in flip are higher off. Extra strikingly, compressing information right into a rating doesn’t shield customers in any respect. It’s because corporations can combination information about purchases within the type of a rating belonging to the category that we examine, with none loss in predictive energy. This class is parametrized by the relevance that every rating offers to previous indicators of conduct, in order that a big weight on the previous results in a rating with excessive persistence.

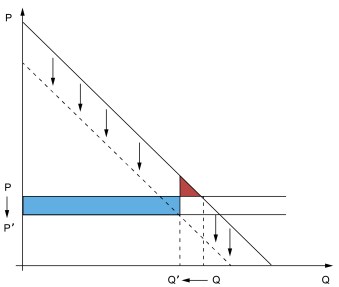

Against this, a strategic client can profit from the presence of scores even when corporations in the end use them towards her, since she will scale back her amount demanded to govern her rating. Contemplate the determine beneath, depicting a standard monopoly drawback between a client with downward-sloping demand and a single agency, say Agency 1. If there is just one interplay, the buyer doesn’t regulate her conduct, leading to an final result with Q models bought at value P. However suppose now {that a} second agency interacts with the buyer tomorrow after seeing a sign of the first-period buy. As a result of the buyer acknowledges the impression of her first-period alternative on the second interval value, she is going to try to scale back Agency 2’s sign—and therefore her rating—by adopting a decrease demand, which reduces her purchases to Q’.

Positive aspects and Losses from Strategic Demand Discount

The patron suffers as a result of she buys much less (with the loss represented by the crimson space). And whereas not depicted, she additionally suffers from future value discrimination on account of details about her willingness to pay (that’s, the intercept of her demand operate) getting transmitted to Agency 2. Nevertheless, Agency 1 is compelled to decrease its value (P’ within the determine) after the strategic demand discount happens. If the buyer has excessive willingness to pay, the good thing about this low cost utilized to many models is such that she needs to be tracked (the blue space—a profit—grows because the intercept of demand will increase).

Managing Customers’ Strategic Response

The strategic demand discount implies that purchases are much less delicate to adjustments in willingness to pay. Thus, indicators lose informativeness, and value discrimination with scores is much less efficient. These losses can’t be eradicated: if corporations use scores which might be greatest predictors in an ex-post sense, that’s, given the accessible information, strategic customers will regulate their conduct making the information much less informative within the first place. A fancy “cat and mouse” state of affairs emerges, with customers trying to “conceal” as corporations search to estimate their preferences.

Our first contribution consists of uncovering that corporations select a suboptimal use of the accessible information to enhance the standard of the underlying information. Particularly, corporations can mitigate their losses in the event that they decide to persistent scores—people who give extreme significance to previous data. This will appear counterintuitive, because the long-term penalties of a really persistent rating counsel customers may turn out to be extra scared of showing data and dealing with excessive costs for a very long time. However a rating that overweighs the previous additionally correlates much less with present willingness to pay, so costs initially react much less to adjustments within the rating. Due to this fact, scores which might be extra persistent than people who come up in a cat and mouse world might be extra worthwhile, as a result of they incentivize customers to sign extra of their data.

Rating “Transparency” Is Crucial

Our second contribution consists of displaying that the opportunity of information assortment benefiting customers by way of decrease costs depends closely on making scores clear. To make this level, we assess the present market paradigm whereby the rating is hidden to the buyer.

When indicators of purchases are imperfect, a strategic client won’t know her rating simply by figuring out her previous conduct. However costs will convey data. Particularly, the remark of a excessive value as we speak tells the buyer that corporations assume she has a excessive willingness to pay, and therefore that costs will stay excessive sooner or later because of the rating’s persistence. If the buyer then expects to buy comparatively few models, she is much less inclined to scale back her demand because of the low cost being utilized to some models solely. Thus, the buyer turns into much less value delicate relative to the case through which the rating is observable. (On this latter case, the buyer would be capable to determine “abnormally” excessive costs as these above what her rating dictates, enabling her to forgo dangerous affords.)

With a diminished sensitivity, corporations make costs extra aware of the rating. Whereas this exacerbates the demand discount and ends in decrease purchases, costs are however greater, which finally ends up hurting customers. What’s extra, strategic customers to whom scores are hidden might be worse off than their naïve counterparts. Our outcomes can inform coverage: client consciousness of the potential for value discrimination and rating transparency have complementary roles, and one with out the opposite could also be detrimental to welfare.

Alessandro Bonatti is a professor of utilized economics on the MIT Sloan College of Administration.

Gonzalo Cisternas is a monetary analysis advisor in Non-Financial institution Monetary Establishment Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How one can cite this submit:

Alessandro Bonatti and Gonzalo Cisternas, “Client Scores and Value Discrimination,” Federal Reserve Financial institution of New York Liberty Avenue Economics, July 11, 2022, https://libertystreeteconomics.newyorkfed.org/2022/07/consumer-scores-and-price-discrimination/.

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).

[ad_2]