{kind=link}

[ad_1]

Firm Overview:

Avalon Applied sciences Restricted (“Avalon Applied sciences”) was included on November 3, 1999. Avalon Applied sciences is among the main absolutely built-in Digital Manufacturing Providers (“EMS”) corporations with end-to-end capabilities in delivering field construct options in India, with a give attention to excessive worth precision engineered merchandise. They supply a full stack product and answer suite, proper from printed circuit board (“PCB”) design and meeting to the manufacture of full digital programs (“Field Construct”), to sure international unique gear producers (“OEMs”), together with OEMs situated in the US, China, Netherlands, and Japan.

Objects of the Provide:

- Prepayment or compensation of all or a portion of sure excellent borrowings availed by the corporate and certainly one of its Materials Subsidiaries, i.e., Avalon Expertise and Providers Non-public Restricted.

- Funding the working capital necessities.

- To hold out the Provide for Sale of Fairness Shares by the Promoting Shareholders.

- Obtain the advantages of itemizing the Fairness Shares on the Inventory Exchanges.

Funding Rationale:

- Distinctive Place: Avalon Applied sciences has a singular international supply mannequin, comprising design and manufacturing capabilities throughout each India and the US. Avalon Applied sciences is the one Indian EMS firm with full-fledged manufacturing services in the US, which provides them a singular aggressive benefit within the North American markets. The corporate has 12 manufacturing models situated throughout the US and India: one unit in Atlanta, Georgia, one unit in Fremont, California, seven models in Chennai, one unit in Kanchipuram and two models in Bengaluru. The electronics manufacturing companies (EMS) market in India was valued at Rs.1.5 trillion (trn) in FY2022 and is anticipated to develop at a CAGR of 32.3% to succeed in a price of Rs.4.5 trn by FY2026. It will create an opportunity to drive the income progress of the corporate.

- Excessive Entry Limitations: Avalon Applied sciences has constructed long run relationships with its purchasers and as of November 30, 2022, that they had a median relationship of 8 years, with purchasers who accounted for 80% of their income. Their expertise in providing EMS companies throughout product and business verticals for purchasers globally for a number of years serves as an entry barrier within the business for any new entrants. Given the depth and nature of the engagement with longstanding prospects, their prospects wouldn’t discover it straightforward to switchover to different EMS suppliers as the associated fee, effort and time for such transitions is excessive. Most of their buyer engagements are with the lengthy lifecycle industries similar to energy, railways, aerospace, medical, and many others.

- Monetary Observe Report: The consolidated income from operations have elevated at a CAGR of 14% between FY20-FY22 from Rs.642 crs in FY20 to Rs.841 crs in FY22. The PAT margin posted a powerful progress of simply 1.9% in FY20 to eight% in FY22. The corporate has a diversified income base with 20% of the general income caters to scrub power, 27% to mobility, 30% to Industrial, 7% to communication and eight% every to Medical and others. Their order e-book (open order) has stood at Rs.1190 crs (1.4x of FY22 Income) as of November 30, 2022. Most of their open orders might be fulfilled inside one 12 months to 18 months.

Key Dangers:

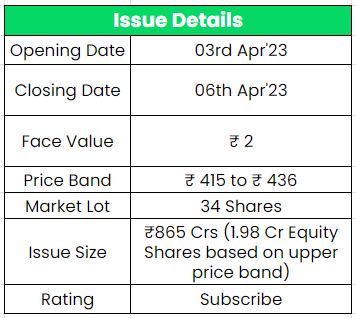

- OFS – The IPO is a mixture of supply on the market (OFS) and Recent challenge with OFS being 63% of the general challenge dimension. Within the supply on the market (OFS), current promoters and shareholders will offload shares price of Rs.545 crs. Promoter & Promoter group promoting shareholders will offload shares price Rs.329 crs and different promoting shareholders will offload shares price Rs.216 crs. The corporate is not going to obtain the proceeds price Rs.545 crs from the OFS half.

- Shopper focus Threat – Greater than 50% of the income comes from Prime 5 purchasers of the corporate. A lack of relationship with any of those prospects can have a big impact on the profitability of the enterprise.

Outlook:

Avalon is among the main built-in digital manufacturing companies corporations in India with properly diversified enterprise resulting in sturdy progress. Its revenues and margins improved considerably in the previous couple of years. The corporate’s listed friends in accordance with the RHP are Dixon Applied sciences, Amber Enterprises, Kaynes Expertise India, Syrma SGS Expertise and Elin Electronics. Evaluating to its friends, Avalon is a pure B2B participant with essentially the most diversified finish person Industries and solely Kaynes and Avalon have a ten%+ EBITDA Margin when in comparison with others. At increased value band, the itemizing market cap might be round ~Rs.2847 crs and Avalon Tech is demanding a P/E a number of of 42x based mostly on FY22 EPS. Whereas evaluating with the Business P/E of 76x, the corporate appears to be positioned between undervalued to Pretty valued class. Based mostly on the above views, we offer a ‘Subscribe’ ranking for this IPO.

If you’re new to FundsIndia, open your FREE funding account with us and revel in lifelong research-backed funding steerage.

Different articles it’s possible you’ll like

Submit Views:

53

[ad_2]