{kind=link}

[ad_1]

Pidilite Industries Ltd. – Keep it up for long run

Pidilite commenced operations in 1969, with two major divisions: pigment emulsions and adhesives. Over time, the corporate diversified into branded client and bazaar merchandise, and enterprise to enterprise phase , which accounted for 80% and 20%, respectively, of gross sales in fiscal 2022. In addition to the mom model, Fevicol, outstanding manufacturers embrace Steelgrip, Dr. Fixit, M-seal, Fevicryl, Fevikwik, Fevistik, Fevilite, Fevibond, and Acron.

The corporate has 30 manufacturing crops, in Mumbai, Mahad, Panvel, Taloja, all in Maharashtra; Vapi, Gujarat; Daman, Union Territory of Daman and Diu; Baddi and Kala Amb, Himachal Pradesh; Guwahati, Assam and Vishakhapatnam, Andhra Pradesh.

To diversify its income stream and facilitate international attain, the corporate has subsidiaries within the US, Thailand, Dubai, Brazil, Egypt, Bangladesh, Sri Lanka , Kenya, Indonesia, Singapore, Ethiopia and China.

Merchandise & Companies:

The Firm provides pigment emulsions and adhesives underneath varied well-known manufacturers particularly Fevicol, Fevicol MR, Dr.Fixit, Fevikwik, M-Seal, Fevistik, Passion Concepts, Fevicryl and Others.

Subsidiaries: As on 31st Mar 2022, the Firm has 33 subsidiaries, each direct and oblique. 13 of those subsidiaries are in India and 20 of them are situated overseas.

Key Rationale:

- Robust Market Place – Pidilite is the Largest participant and the market chief within the client adhesive and Sealant Business. Fevicol is the eminent and legendary model of Pidilite the place Individuals used to assume as Fevicol itself a synonym for adhesive. The corporate has leveraged the model worth and the presence of Fevicol to develop new variants and merchandise. The robust model fairness is backed by larger deal with high quality, diversified distribution community, and robust promoting help. Over time, the corporate has imparted model fairness to commoditised merchandise, via its aggressive and revolutionary advertising and marketing type.

- Concall Highlights – The corporate generates ~65% of its complete income from restore and upkeep segments whereas relaxation is derived from new development. Water proofing, tile adhesive (Pioneer class) rising sooner than different product classes. The corporate added ~2100 new villages (with inhabitants ranging between 5000 and 10000) to develop its retail distribution community ‘Pidilite Ki Duniya’. The corporate has guided to launch one main and two minor revolutionary merchandise in each quarter for the following 12-18 months.

- Q3FY23 – The corporate reported a muted consolidated income development of 5% to ~Rs.2998 crore primarily as a result of muted quantity offtake (up ~1% YoY) within the C&B (Client & Bazaar) phase. The decrease quantity offtake is attributable to increased base and decrease rural demand amid excessive inflations. On a 3 yr CAGR foundation, income grew at a CAGR of 16% led by ~10% quantity CAGR. Administration acknowledged the corporate has consumed majority of the high-cost stock in Q3 and the remaining will probably be consumed in This fall. Administration reported that demand in Nov-Dec’22 was higher than in Oct’22.

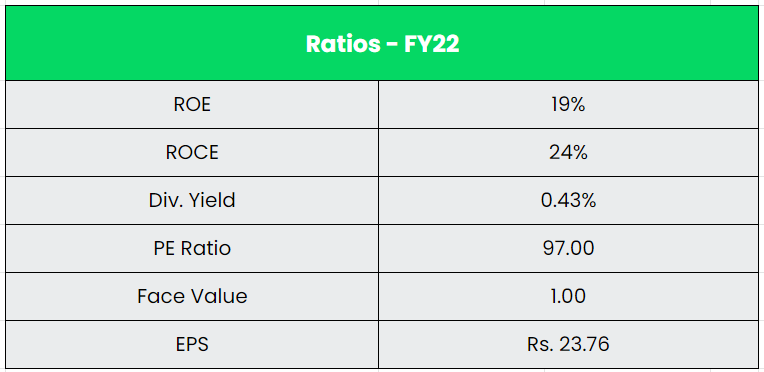

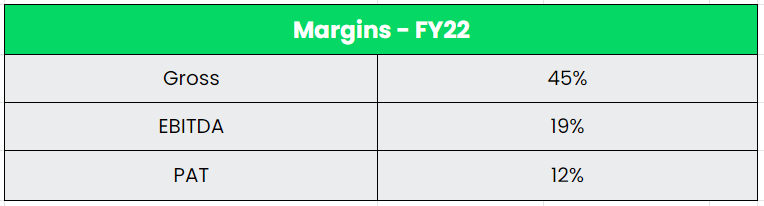

- Monetary Efficiency – The corporate’s 10 Yr Income and PAT CAGR stood at 12% and 14% between FY12-22, respectively. The Cashflow from operations of the corporate grew 10% between FY12-22. The corporate has maintained a mean ROE of 25% and ROCE of 35% for the previous 10 years. The corporate has a robust steadiness sheet with a low debt to fairness ratio of 0.10x and a money and equivalents of Rs.815 crs.

Business:

The Indian adhesives and sealants market is projected to succeed in USD 1,703.68 mn by 2026, rising at an estimated CAGR of 8.07% over the interval of 2021-26. India adhesives and sealants market is extremely concentrated when it comes to income. The highest 5 gamers account for a mixed share of greater than 90%, thus making the market extremely aggressive. Main elements driving the market studied are growing demand from the packaging trade and the rising development trade within the nation. In India, packaging is the fifth largest sector in its financial system and is likely one of the highest development sectors within the nation. In line with the Packaging Business Affiliation of India (PIAI), the sector is rising at CAGR of twenty-two% to 25%. Over the previous few years, packaging trade has been an essential sector in including worth to the assorted manufacturing sectors together with agriculture and FMCG segments.

Development Drivers:

The expansion of particular person finish person segments of meals, drinks, FMCG and prescribed drugs will trickle down into rising demand of packaging options.

A dedication of Rs.79,000 crore for PMAY homes has been made within the Union Price range 2023-24. This can be a 66% enhance in comparison with final yr. The quantity will assist enhance the provision of low-cost properties underneath the Pradhan Mantri Awas Yojana.

The India Paper and Paperboard Packaging Market was valued at USD 10.77 Bn in 2021 and is anticipated to succeed in USD 15.69 bn by 2027, registering a CAGR of 6.63% in the course of the forecast interval of 2022-2027.

Rivals: Asian Paints, Kansai Nerolac, and so on.

Peer Evaluation:

Pidilite is a close to monopoly in its enterprise within the listed house. So, we’ve got in contrast with the paint firms which caters to the same development trade. Pidilite and Asian Paints are examples of Indian firms which have efficiently transitioned commoditized merchandise into client manufacturers via revolutionary promoting, packaging and creating a robust join with the intermediaries (carpenter and painter, respectively). Nevertheless, the important thing distinction between the 2 firms is that paints is a major product whereas adhesive is an ancillary product. Furthermore, repainting cycles are considerably shorter that alternative cycles for furnishings.

Outlook:

In line with the administration, rural demand restoration has began from December 2022 onwards with easing of inflationary stress and pick-up in development actions. Uptick in actual property trade will assist quick restoration within the demand from Tier I and II cities. The corporate has reiterated double digit quantity development within the medium to long run. The ‘Core’ class (contains Fevicol, FeviKwik, m-seal, fevicryl, contributes ~70% to total income) development steering at 1-1.5x GDP, ‘Development’ class (contains Dr.Fixit, Roff, Nina, contributes ~20% to total income) to 2-5x GDP development, ‘Pioneer’ class (CIPY, Jowat, ICA Pidilite) Rs.100 crore within the subsequent three years. Over the following 5 years, the corporate plans to extend the income contribution of ‘Development and Pioneer’ to 50%.

Valuation:

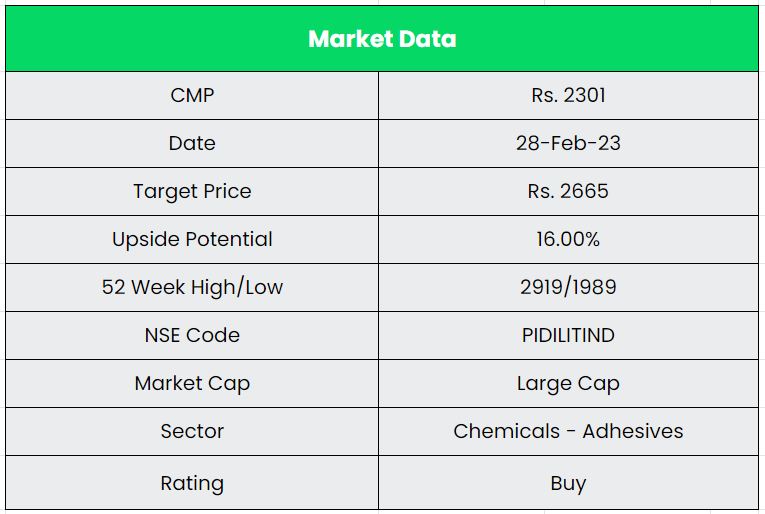

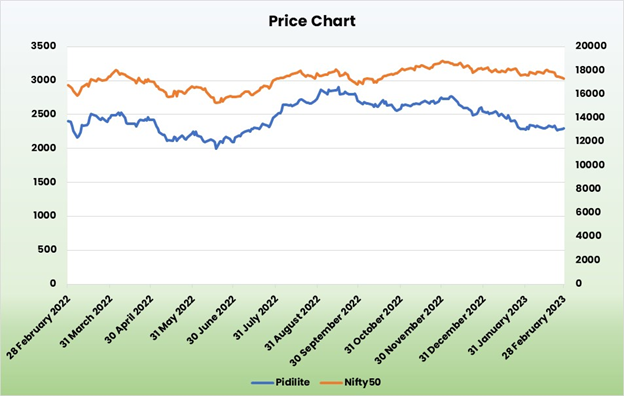

The Administration is optimistic within the development and margin restoration of Pidilite Industries regardless of the near-term challenges. Revival in the actual property enterprise will probably be a key demand driver for Client & Bazaar phase, going ahead. Therefore, we advocate a BUY score within the inventory with the goal value (TP) of Rs.2665, 65x FY25E EPS.

Dangers:

- Uncooked Materials Danger – Any enhance within the uncooked materials costs like VAM resins, and so on. that are spinoff merchandise of crude will impression the working margins of the corporate. Additionally, any delay within the passing of the uncooked materials price will impression the identical.

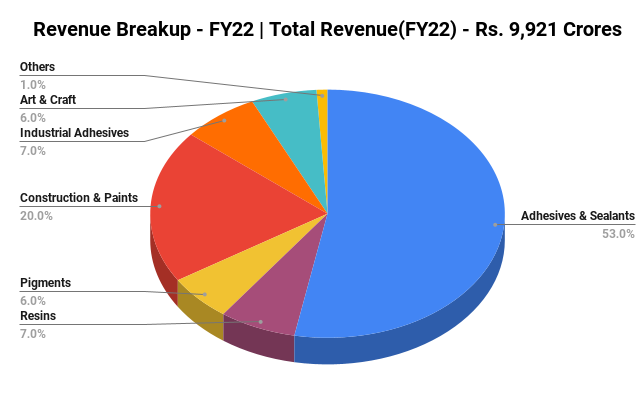

- Aggressive Danger – The economic specialty chemical compounds phase, which is a bulk commodity enterprise, contains industrial adhesives, artificial resins, natural pigments, and surfactants, and accounted for 20% of complete income for fiscal 2022. Heavy competitors within the stated phase will impression the margins.

- Financial Danger – Specialty Industrial Chemical compounds (SIC) phase development is extremely correlated with the general financial exercise within the nation. Any slowdown within the industrial spending would indicate decrease off take of firm’s merchandise.

Different articles chances are you’ll like

Submit Views:

224

[ad_2]