{kind=link}

[ad_1]

Photo voltaic Industries India Ltd. – Explosive Inventory

Established in 1995, Photo voltaic Industries India Ltd. (SIIL) is the biggest producer of business explosives and explosive initiating programs in India and has the world’s largest manufacturing facility for packaged explosives. The corporate initially commenced buying and selling of explosives in 1983 and ventured into explosive manufacturing in 1996. It has greater than 25 years of excellence within the subject of Explosives. With a licensed explosives capability of over 300,000 MT/annum, the corporate has ~30% market share in India.

SIIL, exports to 65 nations around the globe with round 36 manufacturing services worldwide. Financial Explosives, a 100% subsidiary, manufactures detonators. Other than India, the corporate has world manufacturing presence in 7 nations specifically Nigeria, Zambia, South Africa, Turkey, Tanzania, Ghana, and Australia. The corporate additional goals to develop to 10 nations in subsequent 2-3 years.

Merchandise & Providers:

The corporate has numerous merchandise beneath its two principal segments akin to Industrial explosives and Defence explosives.

Industrial Explosives – It consists of assorted merchandise beneath Packaged explosives, Bulk explosives and Initiating programs. These merchandise are utilized in a number of industries like Development, Mining, Street, Quarries, Tunnelling, Hydro initiatives, and so on.

Defence – Army explosives like TNT, RDX, Ammunitions, and so on.; Bombs and warheads for rockets and missiles; warhead for drones and Initiating programs like Ignitors, detonators, and so on. are manufactured beneath Defence explosives.

Subsidiaries: As on 31st Mar 2022, the Firm has 6 (Six) wholly owned Subsidiaries and 18 (Eighteen) Step down subsidiaries.

Key Rationale:

- Sturdy market place – The corporate is the biggest producer of Industrial explosives and explosive initiating programs in India with a market share of ~30% in India. It additionally leads the exports share from India, which is round 70% in industrial explosives and initiating programs. Photo voltaic’s key clientele consists of Coal India ltd. (CIL) and its subsidiaries, contributing to ~17-18% of its revenues within the latest years from contributing greater than 25%, 5 years again. The corporate’s diversification course of resulted within the discount of income share although the income from CIL in absolute worth is rising YoY. Its different main prospects are the Ministry of Defence (Authorities of India), Singareni Collieries Firm Restricted (SCCL) and infrastructure gamers.

- Q3FY23 – In Q3FY23, the corporate had a income progress of large 78% YoY and 16% QoQ at Rs.1812 crs. Explosive section income was up by 71% from Rs.513 crs to Rs.876 crs. Income from initiating system was additionally up by 32% that’s from Rs.101 crs to Rs.133 crs. Within the explosives section, the home quantity within the quarter has elevated by 17% that’s 1,22,000 metric tonnes in comparison with 1,04,700 metric tonnes and the belief is up by 46% that’s Rs.71,745 tonnes versus Rs.49,000 per tonne. In respect to the client breakup, income from defence sector crossed Rs.100 crs for the second consecutive quarter at Rs.110 crs in Q3FY23, a rise of 51% YoY and it’s on the trail to attain the goal of Rs.400 crs in FY23. Exports income elevated by 93% YoY at Rs.729 crs in Q3FY23 which is round 40% of the general income.

- Aggressive Benefits – Majority of the uncooked supplies (besides ammonium nitrate) akin to detonator elements, emulsifiers, sodium nitrate and calcium nitrate are manufactured internally (backward Integration), ends in minimize down in working prices, high quality management and secure EBITDA Margin. The excessive entry boundaries of the explosives trade akin to Industrial licenses with a number of clearances, security clearance from the Authorities and regulatory our bodies acts as a aggressive benefit for the corporate.

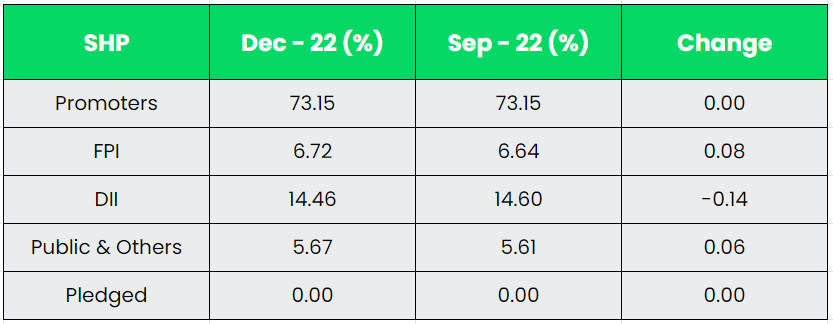

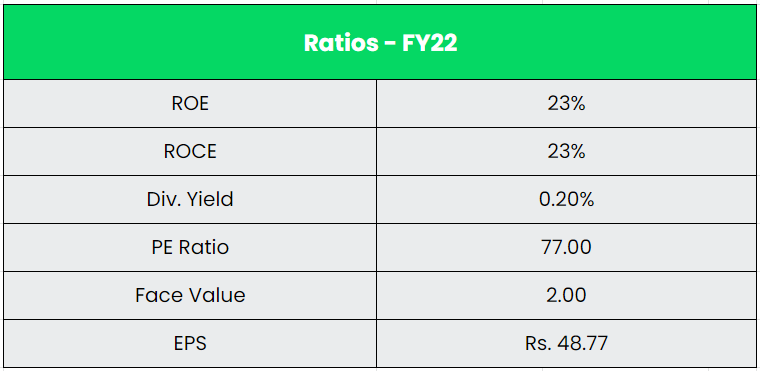

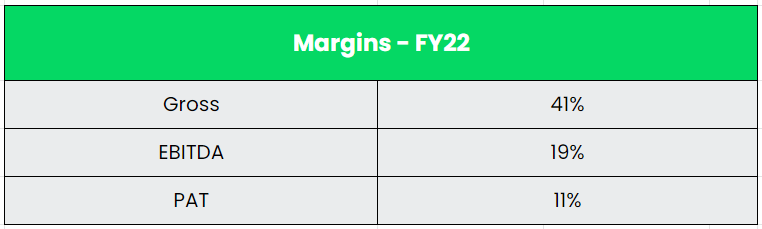

- Monetary Efficiency – The gross sales grew at a CAGR of 20% for the interval of FY17-22 and the revenue after tax grew at a CAGR of 19% for a similar interval. The five-year common worth of ROE and ROCE stand at 22% and 23% respectively. The corporate has a powerful promoter holding of greater than 70% with a much less debt to fairness ratio of 0.5x. EBITDA Margin of the corporate is maintained between 18-22% for the previous 7 years.

Business:

The Indian Defence sector, the second largest armed drive is on the cusp of revolution. The Authorities has recognized the Defence and Aerospace sector as a spotlight space for the ‘Aatmanirbhar Bharat’ or Self-Reliant India initiative, with a formidable push on the institution of indigenous manufacturing infrastructure supported by a requisite analysis and improvement ecosystem. India is positioned because the third largest navy spender on this planet, with its defence finances accounting for two.15% of the nation’s whole GDP. The imaginative and prescient of the federal government is to attain a turnover of $25 Bn together with export of $5 Bn in Aerospace and Defence items and companies by 2025. Until October 2022, a complete of 595 Industrial Licences have been issued to 366 corporations working in Defence Sector. The all-India coal manufacturing within the 12 months 2021-2022 was 778.19 MT compared to 716.08 MT within the 12 months 2020-2021. Additional, within the present monetary 12 months as much as January, 2023, the nation has produced about 698.24 MT of coal as in comparison with about 602.49 MT throughout the identical interval of final 12 months with a progress of about 16%.

Development Drivers:

- To advertise export and liberalize overseas investments, FDI in Defence Sector has been enhanced as much as 74% via the Automated Route and 100% by Authorities Route.

- Other than the Atmanirbhar increase for the sector, the federal government has additionally put a ban on import of 411 gadgets of Providers and whole 3,738 gadgets of Defence Public Sector Undertakings (DPSUs) to assist the sector.

- In FY2023-24, Ministry of Defence (MoD) has been allotted a complete Finances of Rs.5.94 lakh crore, which is 13.18% of the whole finances (Rs.45.03 lakh crore). Capital outlay pertaining to modernization and infrastructure improvement has been elevated to Rs.1.63 lakh crore.

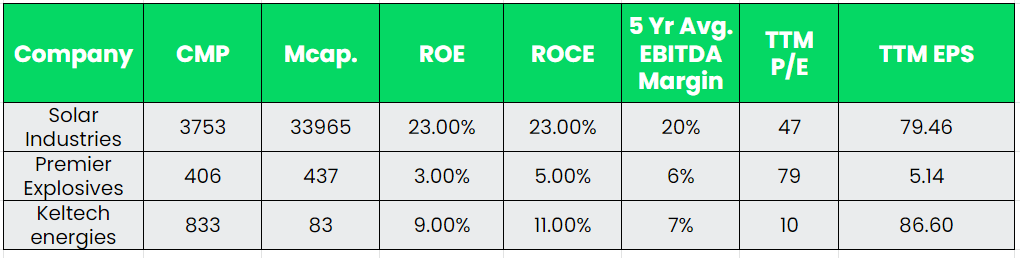

Opponents: Premier Explosives and Keltech energies.

Peer Evaluation:

Photo voltaic Industries is a market chief with round 30% market share within the explosive trade adopted by the opposite listed gamers like premier and keltech with a mere ~5% market share every. SIIL can be a powerful participant when it comes to the corporate dimension and its financials. The return ratios and different basic metrics are robust sufficient for SIIL to simply outperform its friends within the comparability.

Outlook:

The corporate has a pending order e book of Rs.3389 crs as on Q3FY23. The orderbook breaks into Rs.817 crs from defence and the remainder Rs.2572 crs is from CIL and SCCL. The corporate expects the subsequent contract from Coal India by October 2023 and from Singareni Coal by April 2024. Until then, current contracts in hand shall be executed. The Administration has elevated the income steering for FY23 to an enormous 65%+ progress from the sooner steering of 45-50%. However the quantity steering stays unchanged at 15-17% for a similar interval. EBITDA Margins are anticipated to be hovering round 18-20% within the coming quarters. Capex until 9MFY23 is ~Rs.350 crs and for the present 12 months is focused at round Rs.450-500 crs and can proceed at comparable ranges for the subsequent couple of years. The corporate intends to supply its merchandise for area utility and it has began producing outcomes after the profitable launch of Vikram S and static check of PSOM-XL motors made for ISRO. Additionally they intend to develop it additional within the coming years.

Valuation:

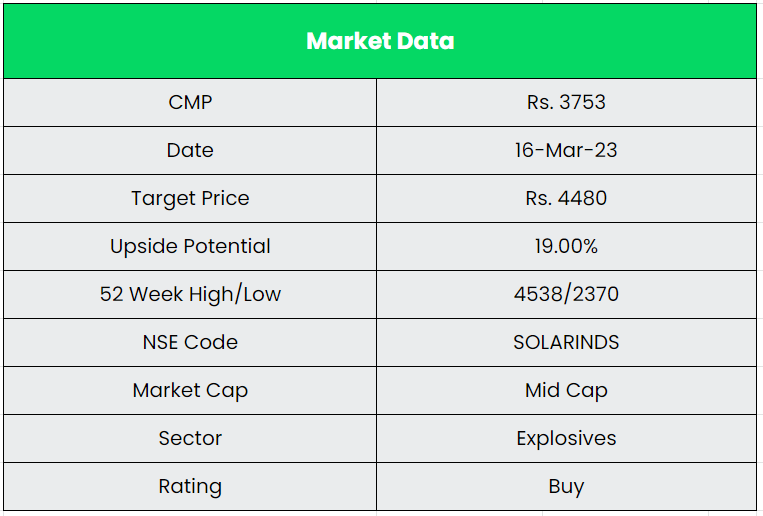

SIIL’s robust expertise in explosives trade, sturdy demand, rising alternatives from the fashionable defence wants ends in a large earnings progress. We suggest a BUY ranking within the inventory with the goal worth (TP) of Rs.4480, 35x FY25E EPS.

Dangers:

- Uncooked Materials Danger – Any extended volatility in uncooked materials (Ammonium Nitrate) costs, together with the shortcoming to fully move on larger costs resulting from stiff aggressive depth, can affect general profitability.

- Demand Associated Danger – Mining and infrastructure are the 2 key buyer segments for SIIL. Any continued slowdown in these might affect the expansion in revenues. These two buyer segments additionally face regulatory dangers when it comes to Govt.’s altering insurance policies.

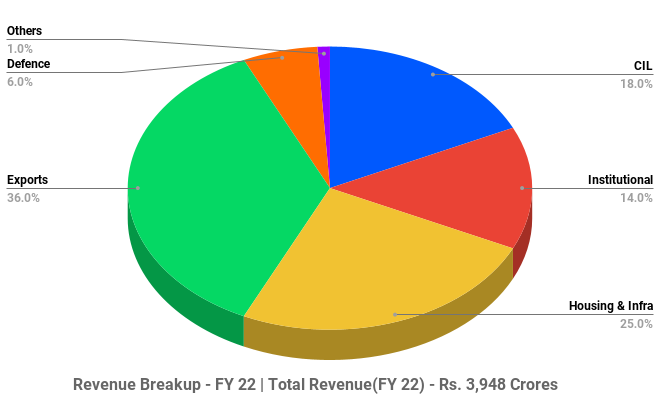

- Foreign exchange Danger – Exports and abroad section contributes the very best with 36% of the general income in FY22 from 50+ nations. So, International alternate fluctuations i.e., any volatility within the forex charges will affect the monetary place of the corporate.

Different articles you could like

Submit Views:

90

[ad_2]