{kind=link}

[ad_1]

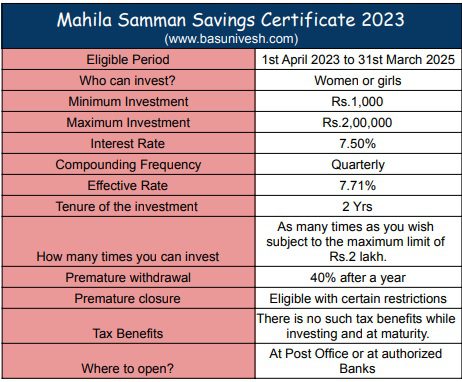

Mahila Samman Financial savings Certificates 2023 is on the market from thirty first March 2023 to thirty first March 2025. This presents an rate of interest of seven.5%. Must you make investments?

Lastly, the federal government notified Mahila Samman Financial savings Certificates 2023 scheme particulars. Allow us to see the options, eligibility, and relevant rate of interest.

As it’s possible you’ll bear in mind, throughout the Price range 2023 speech, the finance minister introduced the particular financial savings scheme for girls. On this regard, the federal government issued the gazette notification issued on March 31, 2023.

All about Mahila Samman Financial savings Certificates 2023 – Options and Eligibility

Allow us to now look into the options of Mahila Samman Financial savings Certificates 2023 options and eligibility.

# Who can open Mahila Samman Financial savings Certificates?

Mahila Samman Financial savings account will be opened by a girl or woman for herself, or by the guardian on behalf of a minor woman. Buyers should fill the Type – I, on or earlier than the thirty first of March, 2025.

Therefore, this scheme is on the market for funding from thirty first March 2023 to thirty first March 2025 (for 2 years ONLY) as of now.

An account opened underneath this Scheme shall be a single-holder kind account. Therefore, you’ll be able to’t open this in a joint account format.

# How a lot is the minimal and most funding in Mahila Samman Financial savings Certificates 2023?

You may open as many accounts as you want. There isn’t a such restrict in numbers. Nonetheless, the restrict is in regards to the minimal quantity and most quantity to be invested.

There must be at the least 3 months of hole between the prevailing account and the brand new opening date.

The minimal quantity to be invested is Rs.1,000 and any sum in multiples of Rs.100. The utmost funding restrict is Rs.2,00,000.

Therefore, one can have as many as investments with out breaching the utmost restrict set underneath this scheme.

# How a lot is the rate of interest underneath Mahila Samman Financial savings Certificates 2023?

The deposits made underneath this Scheme shall bear curiosity on the charge of seven.5% every year. Nonetheless, because the rate of interest is compounding quarterly foundation, the efficient charge will likely be 7.71%.

Nonetheless, in the event you deposited by breaking the principles and eligibility set underneath this scheme, then the curiosity payable on such deposits is the same as the speed of the Put up Workplace Saving Account charge (which is at present at 4%. You may confer with my newest put up on the put up workplace financial savings scheme rates of interest “Newest Put up Workplace Curiosity Charges April – June 2023“).

# Time period or tenure of Mahila Samman Financial savings Certificates 2023

The efficient date of the beginning of this scheme is thirty first March 2023. The tenure of the deposit is 2 years.

The deposit will mature on completion of two years from the date of the deposit and the Eligible Stability could also be paid to the account holder on an utility in Type-2 submitted to the accounts workplace on maturity.

In calculating the maturity worth, any quantity in fraction of a rupee shall be rounded off to the closest rupee and for this objective, any quantity of fifty paise or extra shall be handled as one rupee, and any quantity lower than fifty paise shall be ignored.

# Untimely withdrawal guidelines for Mahila Samman Financial savings Certificates 2023

You might be eligible to withdraw a most of as much as 40% of the Eligible Stability as soon as after the expiry of 1 12 months from the date of opening of the account however earlier than the maturity of the account by submitting an utility Type-3.

In case of an account opened on behalf of a minor woman, the guardian could apply for the withdrawal for the advantage of the minor woman by submitting the next certificates to the accounts workplace, particularly:- “Licensed that the quantity sought to be withdrawn is required for the use and welfare of Miss/ Kumari…………………………………………… who’s a minor woman and is alive on this………………. the day of…………………. (month), …………. (12 months).”.

In calculating the withdrawal from the account, any quantity in fraction of a rupee shall be rounded off to the closest rupee and for this objective, any quantity of fifty paise or extra shall be handled as one rupee, and any quantity lower than fifty paise shall be ignored.

# Untimely withdrawal guidelines for Mahila Samman Financial savings Certificates 2023

The account shall not be closed earlier than maturity besides within the following circumstances, particularly

- On the loss of life of the account holder.

- When the put up workplace or the financial institution in query determines that the operation of the account is placing the account holder by means of undue hardship because of excessive compassionate circumstances, comparable to medical assist for the account holder’s life-threatening diseases or the loss of life of the guardian, it could, after thorough documentation, by order and for causes that will likely be documented in writing, allow the account to be prematurely closed.

- The place an account is prematurely closed, curiosity on the principal quantity shall be payable on the charge relevant to the Scheme for which the account has been held.

- Untimely closure of an account will likely be allowed at any time following after six months from the date of account opening for any motive aside from these listed, through which case the stability that was beforehand within the account would solely be eligible for curiosity at a charge that was 2% decrease than the speed specified on this Scheme.

# Fees underneath Mahila Samman Financial savings Certificates 2023

You need to bear the beneath expenses.

- Receipt – Bodily Mode – Rs.40

- Receipt – e mode – Rs.9

- Funds – 6.5 paise per Rs.100 turnover

# The place to open Mahila Samman Financial savings Certificates 2023?

You may make investments both by means of Put up Workplaces or with any licensed banks (the listing shouldn’t be shared within the notification).

# Taxation of Mahila Samman Financial savings Certificates 2023

As of now, the federal government has not talked about any tax advantages. Therefore, if you make investments on this scheme, then you’ll not get any particular tax advantages. Additionally, as per the present data, there isn’t a tax profit at maturity. The curiosity is taxable as per your tax slab.

I’ve tried to clarify all of the above options within the beneath desk.

Must you spend money on Mahila Samman Financial savings Certificates 2023?

# 7.5% curiosity with an efficient rate of interest of seven.71% for 2 years is somewhat bit extra engaging than another accessible protected choices.

Take for instance, the two-year Authorities Of India Bond displaying a YTM of seven.13% and in the event you have a look at the Put up Workplace Time period Deposit charge of two years is at present at 6.8% (efficient charge 6.9%). Therefore, those that are searching for the higher choice to generate the best return, in a brief interval of two years and with the best security can obliviously search for such a possibility.

Nonetheless, don’t break your current investments for the sake of investing on this scheme. As a result of we don’t know the speed of curiosity of this scheme after thirty first March 2025. Therefore, reinvestment threat is at all times there. Use the corpus which you want after two years slightly than BLIND investing to earn a better charge.

# Rs.2 lakh restrict appears to be too low. If one opts for this scheme and compares the return distinction with Put up Workplace Time period Deposits to this scheme, then one will earn Rs.2,28,874 from Put up Workplace deposit (contemplating 6.8% with compounding quarterly profit) and from Mahila Samman Financial savings Certificates 2023 it’s Rs.2,32,044. The distinction of Rs.3,170. This appears too small.

To make it engaging, the federal government ought to have elevated the utmost restrict from Rs.2 lakh to round Rs.5 lakh or Rs.10 lakh. Nonetheless, it is vitally clear that by providing this product for a shorter interval with a small quantity, the federal government doesn’t need to take an enormous and long-term dedication.

# Liquidity is a priority. Once you e-book two years of FD, then you might be eligible to withdraw at any time limit (after all with a untimely penalty of round 0.25% to the supplied charge). Nonetheless, on this scheme, untimely closure or withdrawal guidelines appear to be a bit strict than the conventional FDs. This makes individuals keep away from this scheme.

# No tax profit in investing on this scheme means yet another hindrance for traders. After all, those that are in decrease revenue teams can go for this scheme. Nonetheless, for many who are underneath the tax bracket or at a better tax bracket, this scheme in my opinion is of no use.

Therefore, aside from the scheme being meant for girls and women with a bit of a better rate of interest, I don’t assume this scheme is value it in another method to be engaging to traders.

Due to this fact, take a name primarily based in your necessities. As I discussed above, the distinction between placing cash in Put up Workplace for two years time period deposit to this scheme is a matter of Rs.3,170 with a little bit of liquidity considerations.

I’m evaluating Put up Workplace Scheme to this scheme primarily as a result of each provide a sovereign assure of the federal government. After all, you’ll be able to cross-check the charges with banks additionally because the investable quantity is simply Rs.2 lakh and banks additionally give you as much as Rs.5 lakh of insurance coverage underneath the DICGC. You may confer with the main points in my earliest put up “Financial institution FDs-Is your Financial institution have Deposit Insurance coverage and Credit score Assure (DICGC)?“. Even you’ll be able to examine the Goal Maturity Funds additionally. The taxation is identical. For instance, Bharat Bond ETF which is able to mature in April 2025 is displaying the yield to maturity as 7.59% (as of immediately). This I believe far superior to Mahila Samman Financial savings Certificates 2023 by way of liquidity and returns. However do do not forget that the YTM of debt funds modifications on day by day foundation. Therefore, it’s important to cross-check earlier than you make investments. Additionally, in the event you want to liquidate in between, then the YTM could differ for you. Investing within the bond market both immediately or by means of debt mutual funds is solely completely different than Financial institution FDs or Mahila Samman Financial savings Certificates 2023 sort of schemes. The concept of comparability is simply to provide you a touch. In the long run, examine your requirement and accordingly you’ll be able to select the most effective appropriate product.

[ad_2]